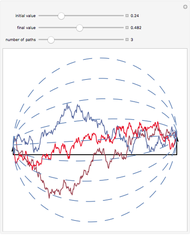

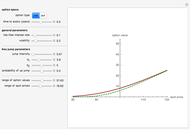

Two Jump Diffusion Processes

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

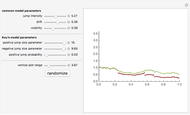

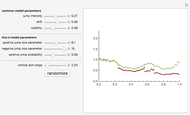

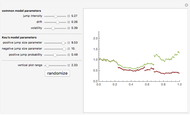

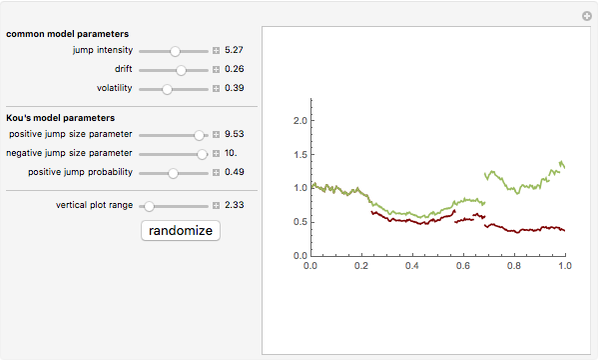

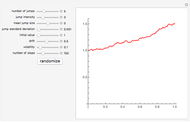

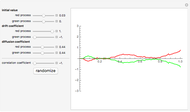

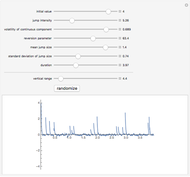

Jump diffusion processes are the simplest generalizations of the classical Black–Scholes model of stock price movements that include discontinuous jumps in price. This Demonstration compares the two most popular diffusion processes: the Merton model and the Kou model. One path from each model is shown. The models share the same continuous component and initial value but differ in their jump distributions, hence their trajectories coincide until the first jump of either process occurs. Kou's model, having 6 independent parameters versus Merton's model's five, is more flexible, hence we expressed the parameter's of Merton's models in terms of those of Kou's one. Thus the two paths shown have the same drift, diffusion as well as mean jump size and the standard deviation of jump sizes.

Contributed by: Andrzej Kozlowski (June 2010)

Open content licensed under CC BY-NC-SA

Snapshots

Details

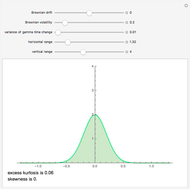

The classical Black–Scholes model of stock price movements is known to suffer from a number of shortcomings. One of them is that the (log) returns distribution of empirical stock returns consistently show asymmetric leptocuritc features not present in the Black–Scholes model. In other words, the empirical return distribution is skewed to the left, and has a higher peak and two heavier tails than those of the normal distribution. Another feature is the so-called volatility smile. Yet another is the clear statistical evidence for the presence of discontinuous jumps in empirical prices, while the Black–Scholes model assumes that price trajectories are continuous.

One approach that successfully overcomes most of these difficulties while still retaining most of the tractability of the Black–Scholes model is to replace the exponential Brownian motion on which the Black–Scholes model is based by an exponential Lévy process. One group of such models are the so called "jump diffusion models". In these models the log stock price has two independent components: the "normal" evolution of prices is given by a diffusion process, punctuated by jumps at random intervals, that represent rare events, crashes, and large drawbacks. Two of the most popular models are Merton's jump diffusion model, in which the jumps in the log-price have a Gaussian distribution, and the Kou model in which they have asymmetric exponential distribution. More precisely, the distribution of jumps is  where

where  and

and  are exponential random variables with means

are exponential random variables with means  and

and  (

( and

and  are called the positive and negative jump size parameter in this Demonstration). The Kou model has a number of advantages over the better known Merton model. First of all, the model can produce more realistic heavier tails in the return distribution compared to the Merton model. Secondly, thanks to the memoryless property of the exponential distribution, explicit formulas can be obtained for many types of options. Thirdly, the presence of six parameters makes calibrating the model to fit empirical data easier.

are called the positive and negative jump size parameter in this Demonstration). The Kou model has a number of advantages over the better known Merton model. First of all, the model can produce more realistic heavier tails in the return distribution compared to the Merton model. Secondly, thanks to the memoryless property of the exponential distribution, explicit formulas can be obtained for many types of options. Thirdly, the presence of six parameters makes calibrating the model to fit empirical data easier.

S. G. Kou, "A Jump Diffusion Model for Option Pricing," Management Science, 48, 2002 pp.1086–1101.

S. G. Kou and H. Wang, "Option Pricing under a Double Exponential Jump Diffusion Model," Management Science, 50, pp. 1178–1192.

Permanent Citation

"Two Jump Diffusion Processes"

http://demonstrations.wolfram.com/TwoJumpDiffusionProcesses/

Wolfram Demonstrations Project

Published: June 16 2010

Merton's Jump Diffusion Model

Merton's Jump Diffusion Model

Andrzej Kozlowski Correlated Wiener Processes

Correlated Wiener Processes

Andrzej Kozlowski The Return Distribution of the Variance Gamma Process

The Return Distribution of the Variance Gamma Process

Andrzej Kozlowski The Poisson Process

The Poisson Process

Andrzej Kozlowski Brownian Bridge

Brownian Bridge

Andrzej Kozlowski Simulating the Poisson Process

Simulating the Poisson Process

Heikki Ruskeepää Correlated Gamma Variance Processes with Common Subordinator

Correlated Gamma Variance Processes with Common Subordinator

Andrzej Kozlowski Polynomial Fits of Random Walks

Polynomial Fits of Random Walks

Michael Schreiber Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski

-

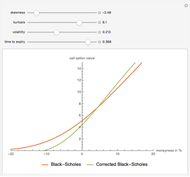

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski -

Newton Polygon and Branching of Algebraic Curves

Newton Polygon and Branching of Algebraic Curves

Andrzej Kozlowski -

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Andrzej Kozlowski -

The Space of Inner Products

The Space of Inner Products

Andrzej Kozlowski