Option Prices in the Kou Jump Diffusion Model

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

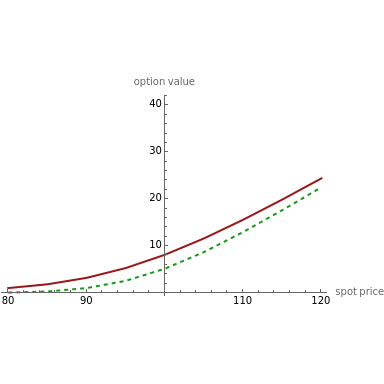

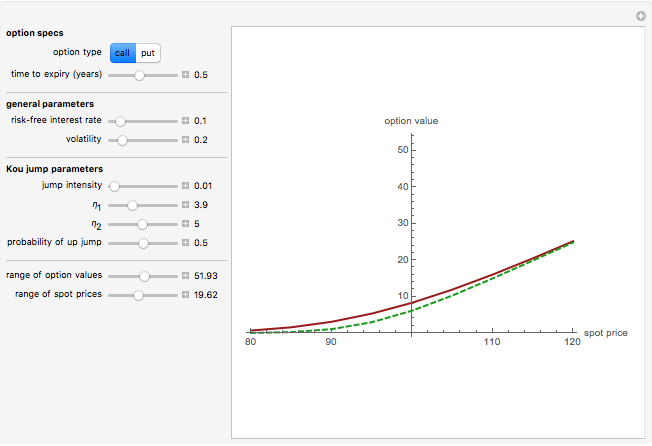

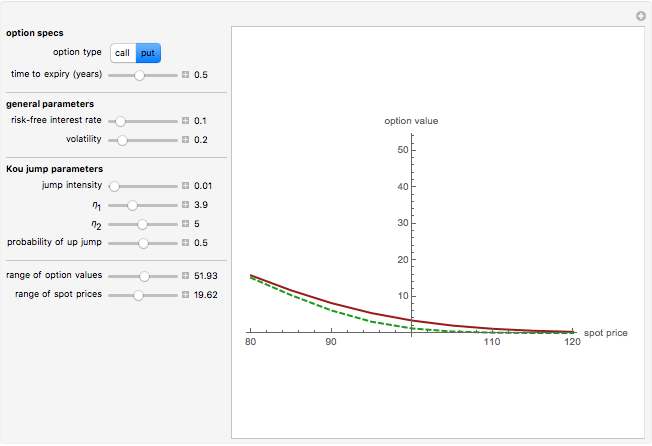

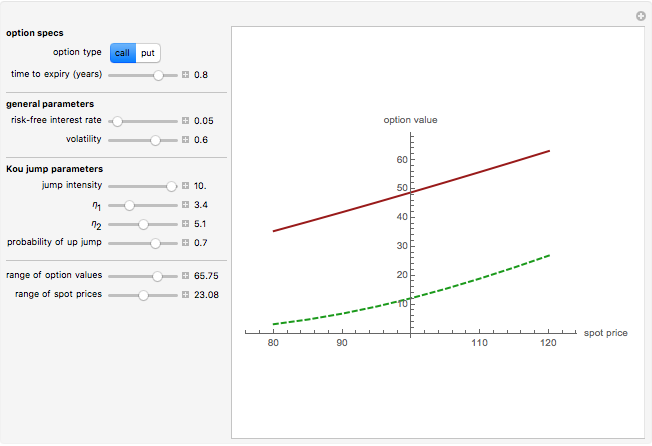

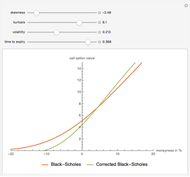

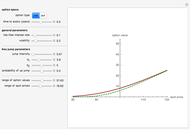

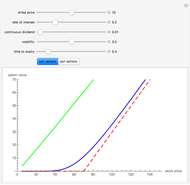

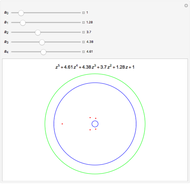

The well-known weaknesses of diffusion-based models of option prices have led to a variety of models involving (in addition to a "diffusive component" driven by an (exponential) Brownian motion) randomly occurring discontinuous jumps. These models are known as "jump diffusions" and form a subset of the set of models driven by an (exponential) Lévy process. The first such model was due to Robert Merton. In Merton's model the jump sizes are normally distributed. Kou introduced a similar model, in which the distribution of jump sizes is an asymmetric exponential. Both models possess certain features that they share with observed market prices and which are not present in the popular Black–Scholes model, such as the leptokurtic feature, but Kou's model has several advantages over Merton's. One of these is the fact that, thanks to the "memoryless property" of the exponential distribution, it is possible to obtain "explicit formulas" for many important types of options. This Demonstration uses such a formula for the price of a European call and put option, shown on the graph by a solid brown curve, which is compared with that of the corresponding option in the Black–Scholes model shown by a dashed green curve. Note than increasing the jump intensity (average jump frequency) parameter will make the jump diffusion price of options increasingly higher than the Black–Scholes one, reflecting the increased jump risk.

Contributed by: Andrzej Kozlowski (September 2010)

Open content licensed under CC BY-NC-SA

Snapshots

Details

In the Kou jump-diffusion model the dynamics of the stock price are given by the stochastic differential eequation (SDE):

,

,

where  is a standard Brownian motion,

is a standard Brownian motion,  is a Poisson process with rate

is a Poisson process with rate  , and

, and  is a sequence of i.i.d. non-negative random variables such that

is a sequence of i.i.d. non-negative random variables such that  has the probability density function

has the probability density function

,

,

where  ,

,  ,

,  represent the probabilities of upward and downward jumps. All sources of randomness are assumed independent, although this assumption can be relaxed. The model has four independent parameters that make it more flexible and easier to calibrate to fit market prices than the Merton model [1], which has only three. The model was introduced by Kou in [2], with an explicit formula (in terms of

represent the probabilities of upward and downward jumps. All sources of randomness are assumed independent, although this assumption can be relaxed. The model has four independent parameters that make it more flexible and easier to calibrate to fit market prices than the Merton model [1], which has only three. The model was introduced by Kou in [2], with an explicit formula (in terms of  functions) for European call and put options. The "memoryless" property of the exponential distribution makes it possible to derive analytical formulas for the expectations of various first passage times, which are the basis for explicit formulas for a variety of options [3].

functions) for European call and put options. The "memoryless" property of the exponential distribution makes it possible to derive analytical formulas for the expectations of various first passage times, which are the basis for explicit formulas for a variety of options [3].

The Black–Scholes model used for comparison with the Kou model has approximately the same variance of daily returns (given by the formula in the footnote on page 1091 of [2]).

References

[1] R. C. Merton, "Option Pricing When Stock Returns Are Discontinuous," Journal of Financial Economics, 3, 1976 pp. 125–144.

[2] S. Kou, "A Jump-Diffusion Model for Option Pricing," Management Science, 48, 2002 pp. 1086–1101.

[3] S. Kou. and H. Wang, "Option Pricing under a Jump-Diffusion Model," Management Science, 50(9), 2004 pp. 1178–1192.

Permanent Citation

Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski Merton's Jump Diffusion Model

Merton's Jump Diffusion Model

Andrzej Kozlowski Option Prices under the Fractional Black-Scholes Model

Option Prices under the Fractional Black-Scholes Model

Andrzej Kozlowski Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

Andrzej Kozlowski The Price of a Call Option on Electrical Power

The Price of a Call Option on Electrical Power

Andrzej Kozlowski Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

Andrzej Kozlowski The Russian Option: Reduced Regret

The Russian Option: Reduced Regret

Andrzej Kozlowski Hedging the European Put Option

Hedging the European Put Option

Andrzej Kozlowski American Call and Put Option

American Call and Put Option

Andrzej Kozlowski

-

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski -

Newton Polygon and Branching of Algebraic Curves

Newton Polygon and Branching of Algebraic Curves

Andrzej Kozlowski -

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Andrzej Kozlowski -

The Space of Inner Products

The Space of Inner Products

Andrzej Kozlowski