Estimating Conditional Expectations with Monte Carlo Simulation and Least Squares Regression

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

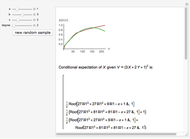

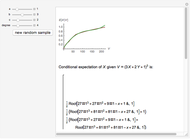

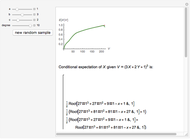

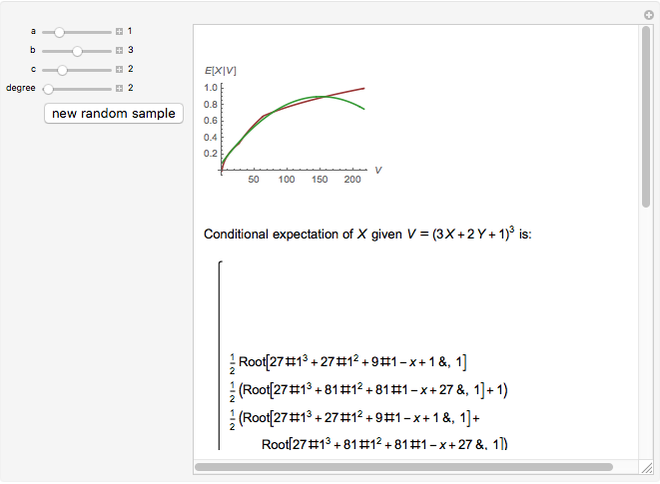

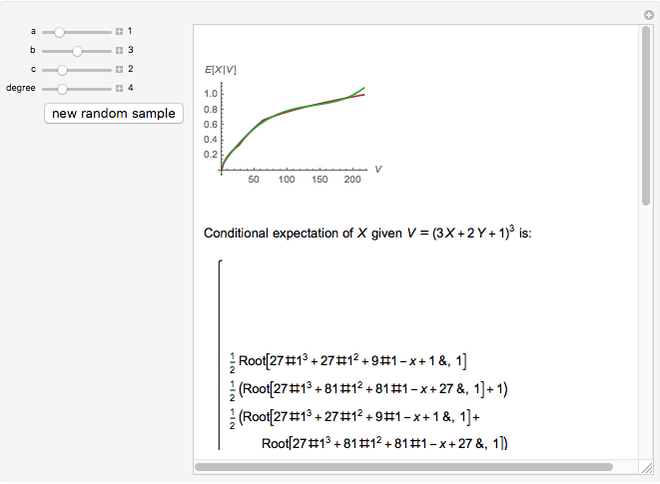

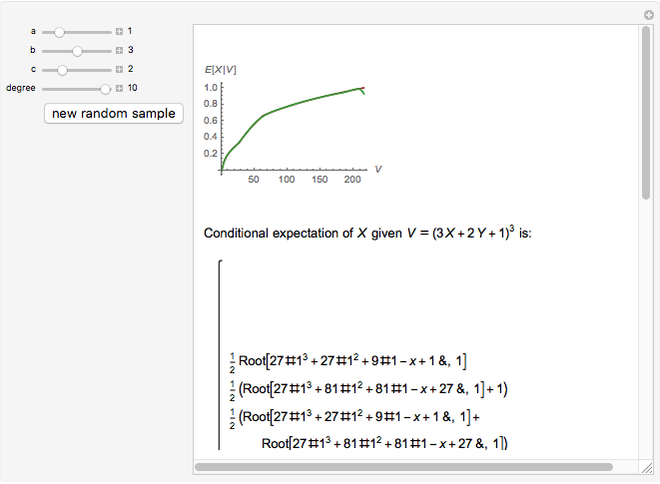

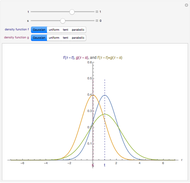

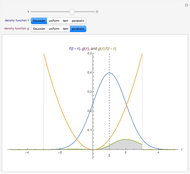

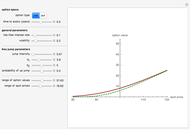

In this Demonstration we consider three random variables,  and

and  , which are uniformly distributed on the interval [0,1] and

, which are uniformly distributed on the interval [0,1] and  , where

, where  ,

,  , and

, and  are (user-specified) non-negative integers. The purpose is to compute the conditional expectation

are (user-specified) non-negative integers. The purpose is to compute the conditional expectation  symbolically and by polynomial regression on data obtained from randomly generated sequences (

symbolically and by polynomial regression on data obtained from randomly generated sequences ( ,

,  ). The display shows the graphs of the conditional expectation function (red) and an estimate (green), explicit formulas giving the exact value of the conditional expectation and its polynomial estimate, and the

). The display shows the graphs of the conditional expectation function (red) and an estimate (green), explicit formulas giving the exact value of the conditional expectation and its polynomial estimate, and the  (square-integrable) error of the estimate, obtained by integrating the square of the difference between the true conditional expectation and the estimated one.

(square-integrable) error of the estimate, obtained by integrating the square of the difference between the true conditional expectation and the estimated one.

Contributed by: Andrzej Kozlowski (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

Many problems in science, economics, finance, and so on require us to compute conditional expectations. If  and are random variables with nice density, then the conditional expectation

and are random variables with nice density, then the conditional expectation  can be defined as the orthogonal projection of on the linear subspace space of all functions of in Hilbert space of all (square-integrable) random variables. Thus the conditional expectation can be though of as a function of with the minimum distance from . This justifies the well‐known Monte Carlo method of approximating

can be defined as the orthogonal projection of on the linear subspace space of all functions of in Hilbert space of all (square-integrable) random variables. Thus the conditional expectation can be though of as a function of with the minimum distance from . This justifies the well‐known Monte Carlo method of approximating  by generating a sample of (, ) pairs and regressing on by solving a least-squares problem for a polynomial of some chosen degree. In this Demonstration we start with two independent random variables and with uniform distribution on [0,1]. As we take a random variable

by generating a sample of (, ) pairs and regressing on by solving a least-squares problem for a polynomial of some chosen degree. In this Demonstration we start with two independent random variables and with uniform distribution on [0,1]. As we take a random variable  for some positive integers , , and . In this case Mathematica is able to compute the exact formula for

for some positive integers , , and . In this case Mathematica is able to compute the exact formula for  , so that we can assess the accuracy of the estimate by computing the norm using numerical integration.

, so that we can assess the accuracy of the estimate by computing the norm using numerical integration.

The idea of this Demonstration is based on an example in chapter 11.6 of

K. L. Judd, Numerical Methods in Economics, Cambridge, MA: The MIT Press, 1998.

Permanent Citation

The Bivariate Normal and Conditional Distributions

The Bivariate Normal and Conditional Distributions

Chris Boucher The Itô Integral and Itô's Lemma

The Itô Integral and Itô's Lemma

Andrzej Kozlowski Least Squares Estimate Using a Monte Carlo Method

Least Squares Estimate Using a Monte Carlo Method

Richard Simson Convolutions of Shifted Densities

Convolutions of Shifted Densities

Xiangjun Shao Convolution of Two Densities

Convolution of Two Densities

Chris Boucher Common Methods of Estimating the Area under a Curve

Common Methods of Estimating the Area under a Curve

Scott Liao (The Harker School) Using Sampled Data to Estimate Derivatives, Integrals, and Interpolated Values

Using Sampled Data to Estimate Derivatives, Integrals, and Interpolated Values

Robert L. Brown Monte Carlo Simulation of Markov Prisoner

Monte Carlo Simulation of Markov Prisoner

Paul Savory (University of Nebraska-Lincoln) Monte Carlo Expectation-Maximization (EM) Algorithm

Monte Carlo Expectation-Maximization (EM) Algorithm

Ian McLeod and Nagham Muslim Mohammad Monte Carlo Simulation of Line-of-Sight Distance Measurements

Monte Carlo Simulation of Line-of-Sight Distance Measurements

Daniel G. Martinez

-

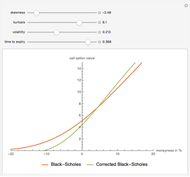

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski -

Newton Polygon and Branching of Algebraic Curves

Newton Polygon and Branching of Algebraic Curves

Andrzej Kozlowski -

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Andrzej Kozlowski -

The Space of Inner Products

The Space of Inner Products

Andrzej Kozlowski