Generalized Hyperbolic Distribution

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

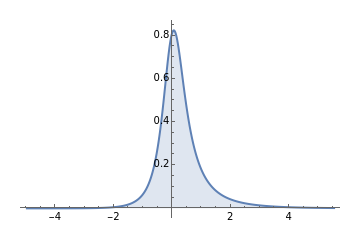

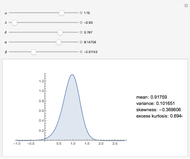

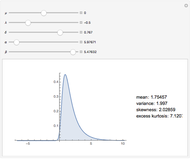

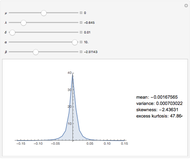

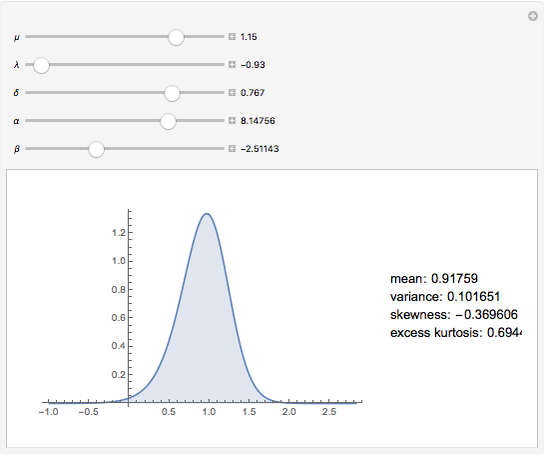

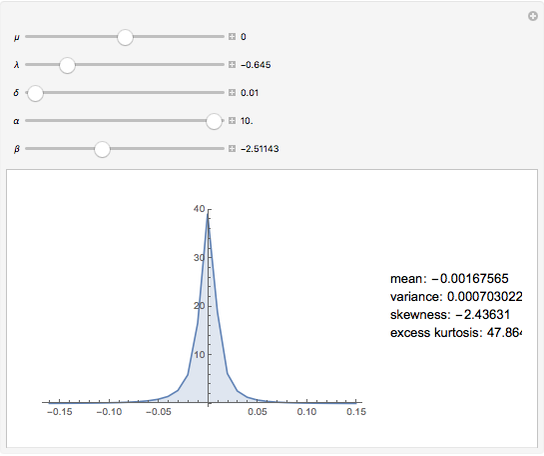

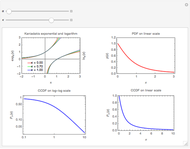

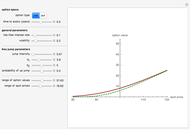

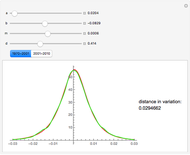

This Demonstration shows the probability density function of the generalized hyperbolic distribution, which generalizes a large number of distributions with numerous applications in finance and other areas. There are a number of parametrizations of this distribution. We use the most common one with five parameters, of which  and

and  describe the location and the scale, while

describe the location and the scale, while  and

and  determine the shape of the distribution. Special values of the parameter

determine the shape of the distribution. Special values of the parameter  often correspond to well-known special cases: for example,

often correspond to well-known special cases: for example,  gives the hyperbolic distribution and

gives the hyperbolic distribution and  gives the normal inverse Gaussian (NIG) distribution. On the other hand, the case

gives the normal inverse Gaussian (NIG) distribution. On the other hand, the case  gives the variance gamma distribution. Many other distributions are obtained as limiting cases.

gives the variance gamma distribution. Many other distributions are obtained as limiting cases.

Contributed by: Andrzej Kozlowski (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

Generalized hyperbolic distributions were introduced by Barndorff–Nielsen [1]. They generalize many previously known distributions in addition to being a source of many new ones. As they are infinitely divisible, Lévy and other stochastic processes can be based on them.

Such processes were first applied in finance by Eberlein and Keller [2]. Being normal variance-mean mixtures, GH distributions possess semi-heavy tails and allow for a natural definition of volatility models by replacing the mixing generalized the inverse Gaussian (GIG) distribution by appropriate volatility processes.

[1] O. E. Barndorff-Nielsen, "Exponentially Decreasing Distributions for the Logarithm of Particle Size," Proceedings of the Royal Society London A, 353(1674), 1977 pp. 401–419.

[2] E. Eberlein and U. Keller, "Hyperbolic Distributions in Finance," Bernoulli 1(3), 1995 pp. 281–299.

Permanent Citation

The Return Distribution of the Variance Gamma Process

The Return Distribution of the Variance Gamma Process

Andrzej Kozlowski Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski The Poisson Process

The Poisson Process

Andrzej Kozlowski Merton's Jump Diffusion Model

Merton's Jump Diffusion Model

Andrzej Kozlowski Brownian Bridge

Brownian Bridge

Andrzej Kozlowski Correlated Wiener Processes

Correlated Wiener Processes

Andrzej Kozlowski Correlated Gamma Variance Processes with Common Subordinator

Correlated Gamma Variance Processes with Common Subordinator

Andrzej Kozlowski The Kappa Distribution

The Kappa Distribution

Fabio Clementi Autoregressive Moving-Average Generator

Autoregressive Moving-Average Generator

Matus Baniar Stable Distribution Function

Stable Distribution Function

Bob Rimmer

-

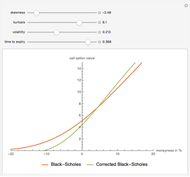

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski -

Newton Polygon and Branching of Algebraic Curves

Newton Polygon and Branching of Algebraic Curves

Andrzej Kozlowski -

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Andrzej Kozlowski -

The Space of Inner Products

The Space of Inner Products

Andrzej Kozlowski