Karhunen-Loeve Directions and Regression

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

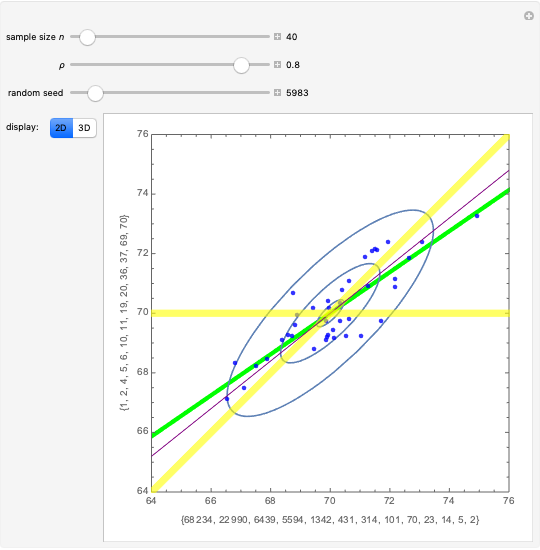

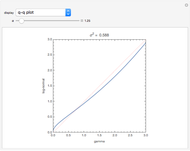

Students sometimes ask about the difference between the regression line and the Karhunen–Loeve direction. The obvious answer a professor might give is that they are different animals! The object of this Demonstration is to give a more interesting answer.

[more]

Contributed by: Ian McLeod (March 2011)

Open content licensed under CC BY-NC-SA

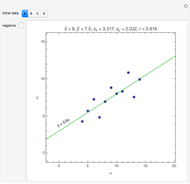

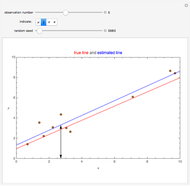

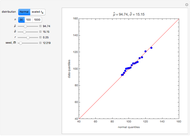

Snapshots

Details

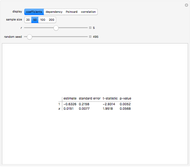

Consider the multivariate random variable  with mean

with mean  and covariance matrix

and covariance matrix  . Then the Karhunen–Loeve directions are determined by columns of

. Then the Karhunen–Loeve directions are determined by columns of  in the eigendecomposition

in the eigendecomposition  , while the regression of

, while the regression of  on

on  is

is

,

,

where  is the matrix

is the matrix  with the first row and column removed. In the present example, this simplifies to

with the first row and column removed. In the present example, this simplifies to  and similarly for the regression of

and similarly for the regression of  on .

on .

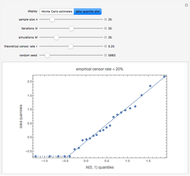

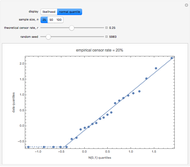

The related question based on data may be asked. In this case we just replace expectations by their sample estimates.

Permanent Citation

Regression toward the Mean

Regression toward the Mean

Ian McLeod Karhunen-Loeve Directions

Karhunen-Loeve Directions

Ian McLeod Hidden Correlation in Regression

Hidden Correlation in Regression

Ian McLeod and Yun Shi Fitting Primes to a Linear Model

Fitting Primes to a Linear Model

Darren Glosemeyer Comparing Some Residuals for Generalized Linear Models

Comparing Some Residuals for Generalized Linear Models

Darren Glosemeyer Comparing Models for Two-Way Contingency Tables

Comparing Models for Two-Way Contingency Tables

Darren Glosemeyer Exploring Measures of Association

Exploring Measures of Association

Jeff Hamrick The r-Distribution

The r-Distribution

Chris Boucher Kernel Density Estimation

Kernel Density Estimation

Jeff Hamrick Maximum Likelihood Estimators for Binary Outcomes

Maximum Likelihood Estimators for Binary Outcomes

Seth J. Chandler

-

Rank Transform in Harmonic Regression Time Series

Rank Transform in Harmonic Regression Time Series

Ian McLeod -

Detecting Periodicity in Short Time Series

Detecting Periodicity in Short Time Series

Ian McLeod -

Tempered Fractionally Differenced White Noise

Tempered Fractionally Differenced White Noise

Ian McLeod -

Regression toward the Mean

Ian McLeod -

Spread-Location Regression Diagnostic Check

Spread-Location Regression Diagnostic Check

Ian McLeod -

Anscombe Quartet

Anscombe Quartet

Ian McLeod -

Visualizing Higher-Dimensional Data with 3D Scatterplots

Visualizing Higher-Dimensional Data with 3D Scatterplots

Ian McLeod -

Mean, Fitted-Value, Error, and Residual in Simple Linear Regression

Mean, Fitted-Value, Error, and Residual in Simple Linear Regression

Ian McLeod -

Estimating and Diagnostic Checking in Censored Normal Random Samples

Estimating and Diagnostic Checking in Censored Normal Random Samples

Ian McLeod -

Comparing Gamma and Log-Normal Distributions

Comparing Gamma and Log-Normal Distributions

Ian McLeod -

Monte Carlo Expectation-Maximization (EM) Algorithm

Monte Carlo Expectation-Maximization (EM) Algorithm

Ian McLeod -

Comparing Exact and Approximate Censored Normal Likelihoods

Comparing Exact and Approximate Censored Normal Likelihoods

Ian McLeod -

Transformation to Symmetry of Gamma Random Variables

Transformation to Symmetry of Gamma Random Variables

Ian McLeod -

Illustrating the Central Limit Theorem with Sums of Bernoulli Random Variables

Illustrating the Central Limit Theorem with Sums of Bernoulli Random Variables

Ian McLeod -

Hidden Correlation in Regression

Ian McLeod -

Informal Power Assessment of the Normal Probability Plot

Informal Power Assessment of the Normal Probability Plot

Ian McLeod -

Time Series for Power-Law Decay

Time Series for Power-Law Decay

Ian McLeod -

Block Bootstrap for Time Series

Block Bootstrap for Time Series

Ian McLeod -

Fractional Gaussian Noise

Fractional Gaussian Noise

Ian McLeod -

Plotting a Long Time Series

Plotting a Long Time Series

Ian McLeod