Illustrating the Central Limit Theorem with Sums of Bernoulli Random Variables

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

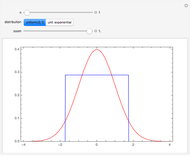

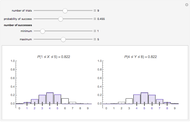

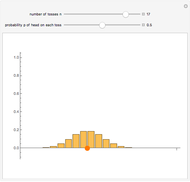

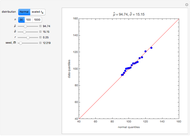

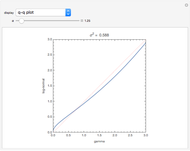

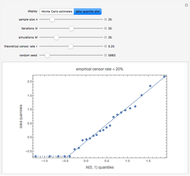

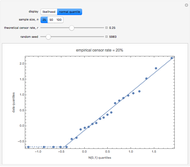

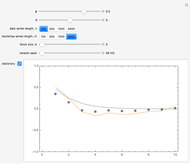

Consider the central limit theorem for independent Bernoulli random variables  , where

, where  and

and  ,

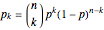

,  . Then the sum

. Then the sum  is binomial with parameters

is binomial with parameters  and

and  and

and  converges in distribution to the standard normal. The exact distribution for

converges in distribution to the standard normal. The exact distribution for  may be written

may be written  , where

, where  ,

,  ,

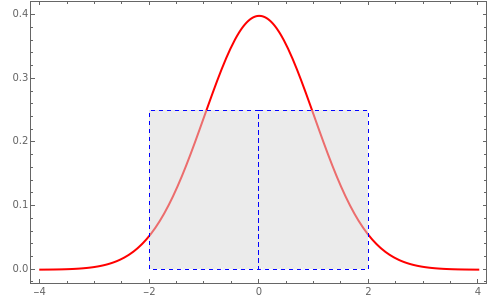

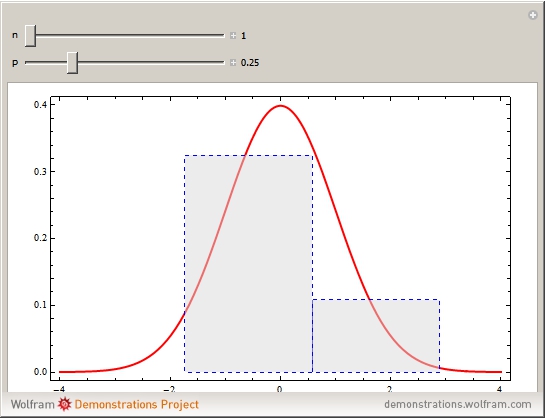

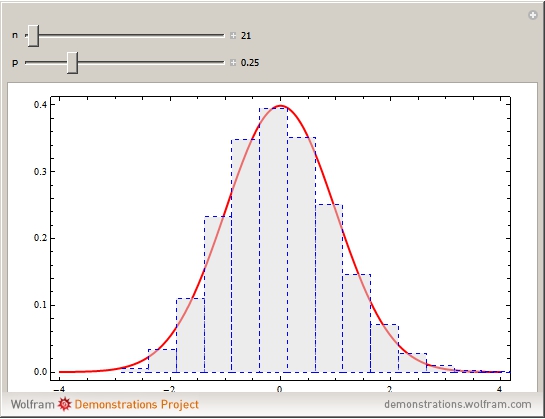

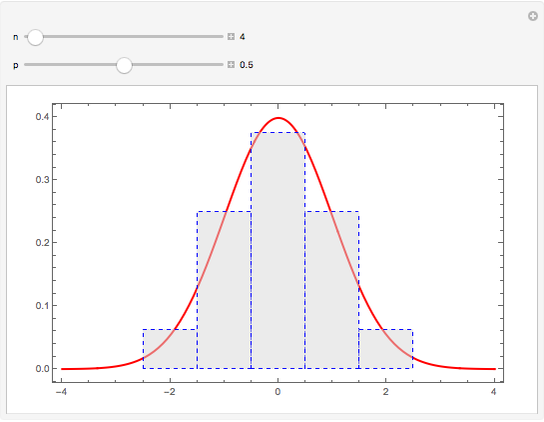

,  . The convergence may be illustrated using rectangles of width

. The convergence may be illustrated using rectangles of width  and height

and height  centered at

centered at  . As

. As  increases, the rectangles closely approach the standard normal density function. The convergence is faster in the symmetric case when

increases, the rectangles closely approach the standard normal density function. The convergence is faster in the symmetric case when  .

.

Contributed by: Ian McLeod (University of Western Ontario) (February 2010)

Open content licensed under CC BY-NC-SA

Snapshots

Details

detailSectionParagraph Binomial Approximation to a Poisson Random Variable

Binomial Approximation to a Poisson Random Variable

Chris Boucher Mathematica 7's Discrete Distributions

Mathematica 7's Discrete Distributions

Nasser M. Abbasi Illustrating the Central Limit Theorem with Sums of Uniform and Exponential Random Variables

Illustrating the Central Limit Theorem with Sums of Uniform and Exponential Random Variables

Ian McLeod Successes and Failures in a Run of Bernoulli Trials

Successes and Failures in a Run of Bernoulli Trials

Chris Boucher Illustrating the Central Limit Theorem Using the Quantile Plot for Sums of Unit Exponential Random Variables

Illustrating the Central Limit Theorem Using the Quantile Plot for Sums of Unit Exponential Random Variables

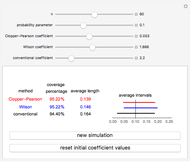

Ian McLeod Confidence Intervals, Confidence Levels, and Average Interval Length

Confidence Intervals, Confidence Levels, and Average Interval Length

Tomas Garza Confidence Intervals for the Binomial Distribution

Confidence Intervals for the Binomial Distribution

Tomas Garza Binomial Distribution

Binomial Distribution

Chris Boucher Central Limit Theorem Illustrated with Four Probability Distributions

Central Limit Theorem Illustrated with Four Probability Distributions

D. Meliga and S. Z. Lavagnino Generalized Central Limit Theorem

Generalized Central Limit Theorem

Roger J. Brown and Bob Rimmer

-

Rank Transform in Harmonic Regression Time Series

Rank Transform in Harmonic Regression Time Series

Ian McLeod -

Detecting Periodicity in Short Time Series

Detecting Periodicity in Short Time Series

Ian McLeod -

Tempered Fractionally Differenced White Noise

Tempered Fractionally Differenced White Noise

Ian McLeod -

Regression toward the Mean

Regression toward the Mean

Ian McLeod -

Spread-Location Regression Diagnostic Check

Spread-Location Regression Diagnostic Check

Ian McLeod -

Anscombe Quartet

Anscombe Quartet

Ian McLeod -

Visualizing Higher-Dimensional Data with 3D Scatterplots

Visualizing Higher-Dimensional Data with 3D Scatterplots

Ian McLeod -

Mean, Fitted-Value, Error, and Residual in Simple Linear Regression

Mean, Fitted-Value, Error, and Residual in Simple Linear Regression

Ian McLeod -

Estimating and Diagnostic Checking in Censored Normal Random Samples

Estimating and Diagnostic Checking in Censored Normal Random Samples

Ian McLeod -

Comparing Gamma and Log-Normal Distributions

Comparing Gamma and Log-Normal Distributions

Ian McLeod -

Monte Carlo Expectation-Maximization (EM) Algorithm

Monte Carlo Expectation-Maximization (EM) Algorithm

Ian McLeod -

Comparing Exact and Approximate Censored Normal Likelihoods

Comparing Exact and Approximate Censored Normal Likelihoods

Ian McLeod -

Transformation to Symmetry of Gamma Random Variables

Transformation to Symmetry of Gamma Random Variables

Ian McLeod -

Illustrating the Central Limit Theorem with Sums of Bernoulli Random Variables

Illustrating the Central Limit Theorem with Sums of Bernoulli Random Variables

Ian McLeod -

Hidden Correlation in Regression

Hidden Correlation in Regression

Ian McLeod -

Informal Power Assessment of the Normal Probability Plot

Informal Power Assessment of the Normal Probability Plot

Ian McLeod -

Time Series for Power-Law Decay

Time Series for Power-Law Decay

Ian McLeod -

Block Bootstrap for Time Series

Block Bootstrap for Time Series

Ian McLeod -

Fractional Gaussian Noise

Fractional Gaussian Noise

Ian McLeod -

Plotting a Long Time Series

Plotting a Long Time Series

Ian McLeod