Maximum Likelihood Estimators with Normally Distributed Error

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

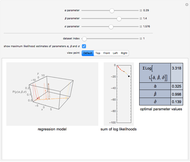

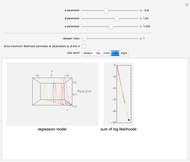

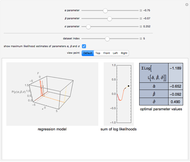

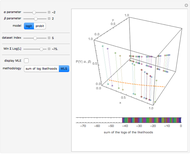

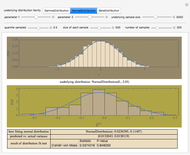

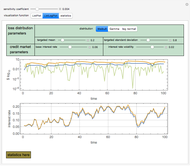

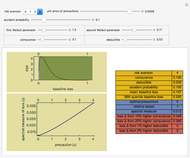

In statistics, there is a frequent desire to develop a model that has, of all models in that class, the maximum likelihood of producing the data observed. This Demonstration shows how to derive the maximum likelihood estimates of the coefficients in a linear model of data ( ) that is believed to have normally distributed error with a standard deviation of a user-set value

) that is believed to have normally distributed error with a standard deviation of a user-set value  . The top panel shows the data, the current regression model (as an orange line) and the probability (likelihood) that each

. The top panel shows the data, the current regression model (as an orange line) and the probability (likelihood) that each  value would occur for a given

value would occur for a given  value, given

value, given  and

and  . The bottom panel shows the sum of the logs of each of these likelihoods. Selection of maximum likelihood estimates of and will make this sum as large as possible and the displayed rectangle as small as possible. Curious users can request a computation of the maximum likelihood estimate for each dataset.

. The bottom panel shows the sum of the logs of each of these likelihoods. Selection of maximum likelihood estimates of and will make this sum as large as possible and the displayed rectangle as small as possible. Curious users can request a computation of the maximum likelihood estimate for each dataset.

Contributed by: Seth J. Chandler (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

For pedagogical purposes, this Demonstration finds maximum likelihood estimators using a general approach. In specific cases, more efficient and swifter computational methods may exist. In particular, optimal parameter values in the case of normally distributed error can be obtained via linear least-squares optimization; the maximum likelihood estimate of the standard deviation can be obtained as the square root of the mean of the squared residuals. The code underlying this Demonstration permits this swifter but less general methodology to be used.

This Demonstration will be more responsive to movements of the parameter sliders if no computation of the maximum likelihood estimate is requested.

A useful experiment is to set the parameter sliders so that they correspond to the optimal parameter values determined by the computer. Then determine the effect on the sum of the log likelihoods as the σ parameter increases. Then see what happens if you set the α and β parameter sliders to suboptimal levels. Does increasing increase or decrease the sum of the log likelihoods?

Permanent Citation

Maximum Likelihood Estimators for Binary Outcomes

Maximum Likelihood Estimators for Binary Outcomes

Seth J. Chandler The Sampling Distribution of a Sampling Quantile

The Sampling Distribution of a Sampling Quantile

Seth J. Chandler Maximum Likelihood Estimation

Maximum Likelihood Estimation

Marc Brodie (Wheeling Jesuit University) Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler Maximum Likelihood Estimation of Ordinary and Finite Mixture Distributions

Maximum Likelihood Estimation of Ordinary and Finite Mixture Distributions

Heikki Ruskeepää and M. A. Ghorbani Maximum Likelihood Estimation for Coin Tosses

Maximum Likelihood Estimation for Coin Tosses

Tad Hogg Intuitive Parameterization of the Bivariate Normal Distribution

Intuitive Parameterization of the Bivariate Normal Distribution

Robert L. Brown Rotational Symmetry of Multivariate Uncorrelated Standard Normal Distribution

Rotational Symmetry of Multivariate Uncorrelated Standard Normal Distribution

Diego M. Oviedo-Salcedo Marginal Normality Does Not Imply Bivariate Normality

Marginal Normality Does Not Imply Bivariate Normality

Ehsan Azhdari Joint Density of Trivariate Gaussian Random Variables

Joint Density of Trivariate Gaussian Random Variables

John M. Shea

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

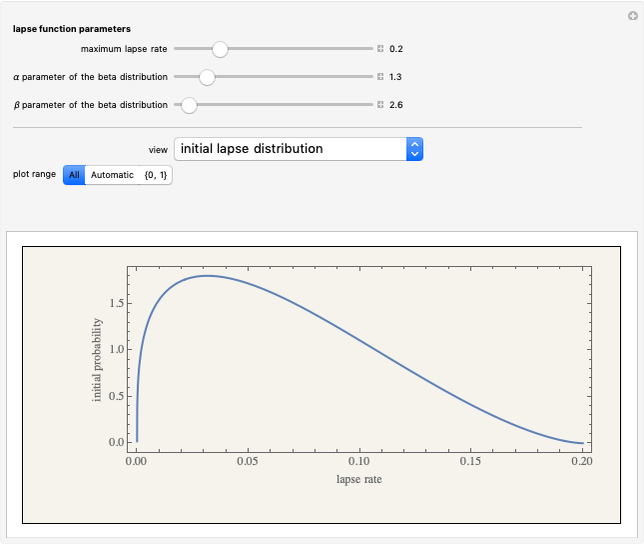

A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

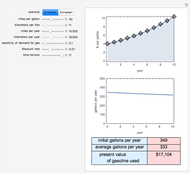

The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler