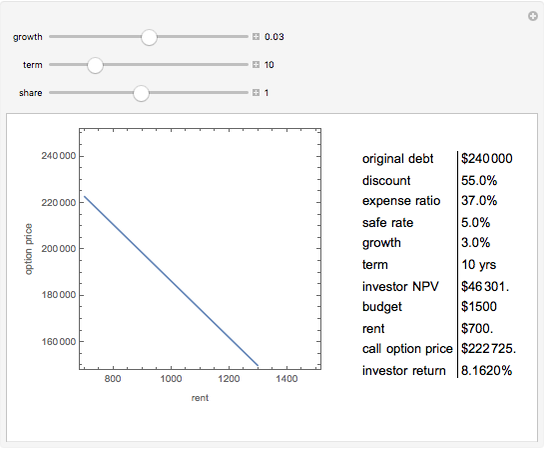

The Price-Terms Tradeoff

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

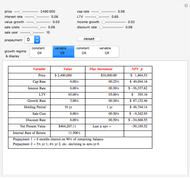

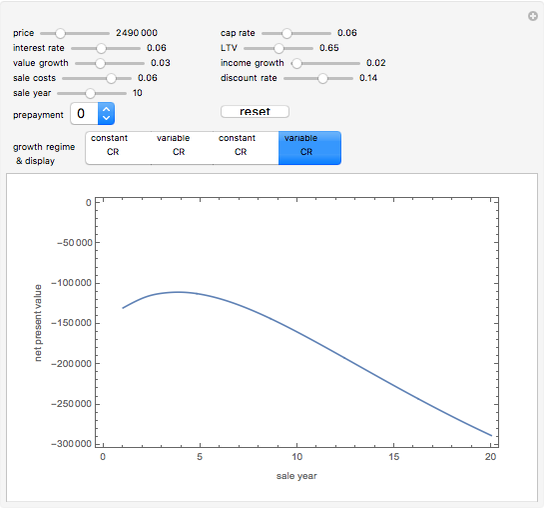

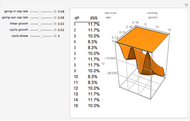

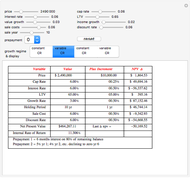

It is widely accepted that commodities have two prices: a cash price and a different price if payment is deferred to some later time. Delayed payment for a real estate investment acquisition can involve many individual terms, such as loan-to-value ratio (LTV), interest rate, and term. Woven into this are assumptions the investor must make about the future, such as growth rate and discount rate. This Demonstration shows the most common variables and produces a net present value for each set. The third column provides an increment of positive change in that variable. The last output (right column) in the grid is the net present value (NPV) of the change in that variable after an up increment. Thus, the user desiring to know how much price difference a particular relaxation of terms may be worth can make that change and see the net present value difference, all else remaining constant. In the lower-right cell the change from the last NPV is shown.

[more]

Contributed by: Roger J. Brown (March 2011)

Reproduced by permission of Academic Press from Private Real Estate Investment ©2005

Open content licensed under CC BY-NC-SA

Snapshots

Details

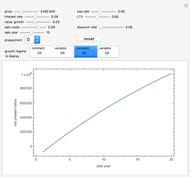

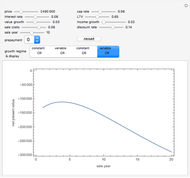

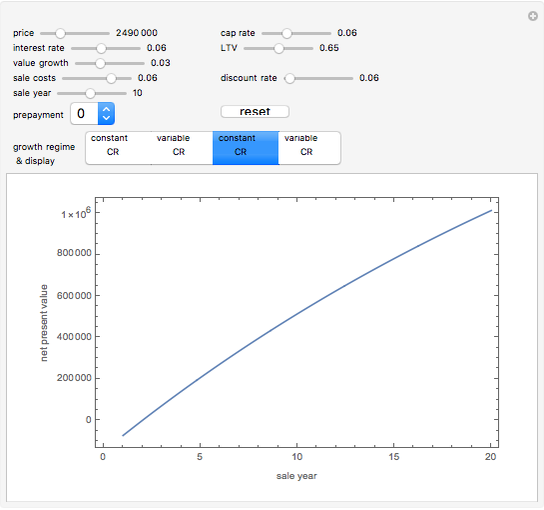

Notice what appears to be an anomaly: when price increases, NPV also increases. This, however counterintuitive, is the result of an assumption that capitalization rate is constant over the holding period (the "Constant CR" option). For this to be possible, growth must occur on both income and value at the same rate. The alternate assumption, that different growth rates apply to value and income, produces capitalization rates that vary over time ("Variable CR" option) and results in NPV change depending on the relative direction and magnitudes of the different growth rates.

This Demonstration shows the value, in terms of NPV, of incremental changes in negotiated variables. Following that purpose, one can use the sliders to learn about scale and direction. For instance, the default values show that a 5% change in LTV produces a trivial difference in NPV, while a change of one-tenth of that amount on the projected growth rate has a very substantial effect. Not surprisingly, the direction of NPV change is the opposite for interest rate and cap rate. It may be more helpful to know that, at the default values, a change of capitalization rate of roughly half the change in interest rate is nearly offsetting.

There are some comforting results to be found. Here are three examples: First, when the computed internal rate of return is less than the pre-specified discount rate, the net present value is, as expected, negative. Second, setting the income growth lower than the value growth over time and a high initial capitalization rate (which is the point value of the ratio of income to value at the time of purchase) produces, as expected, high net present values. This is the mathematical representation of the investment strategy that always works: buy low and sell high. Third, one can model the opposite, choose either graphic view and move the initial discount rate to the right to show the disastrous results arising from owning during a time when rates are moving in the wrong direction.

There is also a comment to be made about linearity. While some forms of NPV may be linear, in general NPV is not linear in each variable. Thus, note that moving the slider for capitalization rate reflects a constant NPV change for each increment of capitalization rate change. Also note that three other variables—interest rate, LTV, and sale cost—have constant change values at all levels of capitalization rate within the range of this Demonstration.

More information is available in Chapter Four of Private Real Estate Investment and at mathestate.com.

R. J. Brown, Private Real Estate Investment: Data Analysis and Decision Making, Burlington, MA: Elsevier Academic Press, 2005.

Permanent Citation

"The Price-Terms Tradeoff"

http://demonstrations.wolfram.com/ThePriceTermsTradeoff/

Wolfram Demonstrations Project

Published: March 7 2011

Explaining Real Estate Price Bubbles

Explaining Real Estate Price Bubbles

Roger J. Brown Term Structure of Interest Rates

Term Structure of Interest Rates

Roger J. Brown Stock Price Envelopes

Stock Price Envelopes

Seth J. Chandler Simulating the IRR

Simulating the IRR

Roger J. Brown Capitalization Rate Probability

Capitalization Rate Probability

Roger J. Brown Net Lease Economics

Net Lease Economics

Roger J. Brown The Effect of Holding Period on Real Estate Investment Return

The Effect of Holding Period on Real Estate Investment Return

Roger J. Brown Value Added Growth Model

Value Added Growth Model

Roger J. Brown Real Options

Real Options

Roger J. Brown Solving the Subprime Loan Problem

Solving the Subprime Loan Problem

Roger J. Brown

-

Dissolving Partnerships

Dissolving Partnerships

Roger J. Brown -

Forming the Efficient Frontier When Returns Are Non-Normal

Forming the Efficient Frontier When Returns Are Non-Normal

Roger J. Brown -

Spectral Measures

Spectral Measures

Roger J. Brown -

Granger-Orr Running Variance Test

Granger-Orr Running Variance Test

Roger J. Brown -

Capitalization Rate Probability

Roger J. Brown -

Net Lease Economics

Roger J. Brown -

The Refinance Decision

The Refinance Decision

Roger J. Brown -

True Cost of Variable Rate Mortgage Funds

True Cost of Variable Rate Mortgage Funds

Roger J. Brown -

Term Structure of Interest Rates

Roger J. Brown -

Generalized Central Limit Theorem

Generalized Central Limit Theorem

Roger J. Brown -

Inflation-Adjusted Yield

Inflation-Adjusted Yield

Roger J. Brown -

Simulating the IRR

Roger J. Brown -

Real Options

Roger J. Brown -

The Price-Terms Tradeoff

The Price-Terms Tradeoff

Roger J. Brown -

Fitting an Elephant

Fitting an Elephant

Roger J. Brown -

Solving the Subprime Loan Problem

Roger J. Brown -

Why Location Matters: The Bid Rent Curve

Why Location Matters: The Bid Rent Curve

Roger J. Brown -

Explaining Real Estate Price Bubbles

Roger J. Brown -

Value Added Growth Model

Roger J. Brown -

Connecting the CDF and the PDF

Connecting the CDF and the PDF

Roger J. Brown