Connecting the CDF and the PDF

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

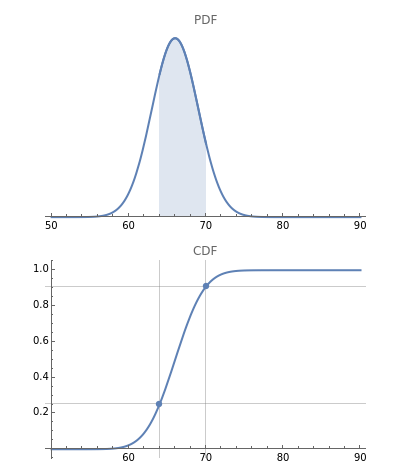

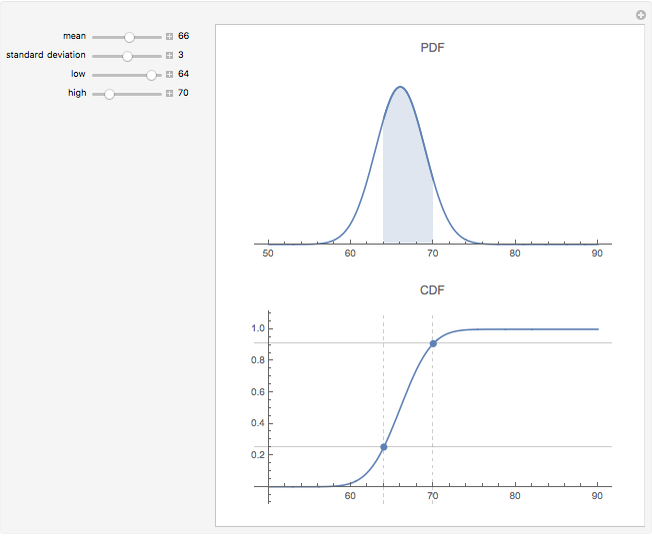

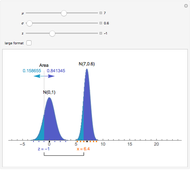

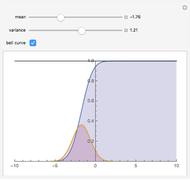

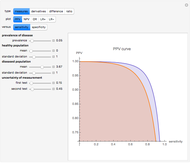

The probability density function (PDF - upper plot) is the derivative of the cumulative density function (CDF - lower plot). This elegant relationship is illustrated here. The default plot of the PDF answers the question, "How much of the distribution of a random variable is found in the filled area; that is, how much probability mass is there between observation values equal to or more than 64 and equal to or fewer than 70?"

[more]

Contributed by: Roger J. Brown (November 2007)

Reproduced by permission of Academic Press from Private Real Estate Investment ©2005

Open content licensed under CC BY-NC-SA

Details

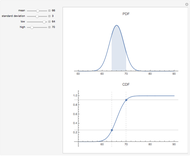

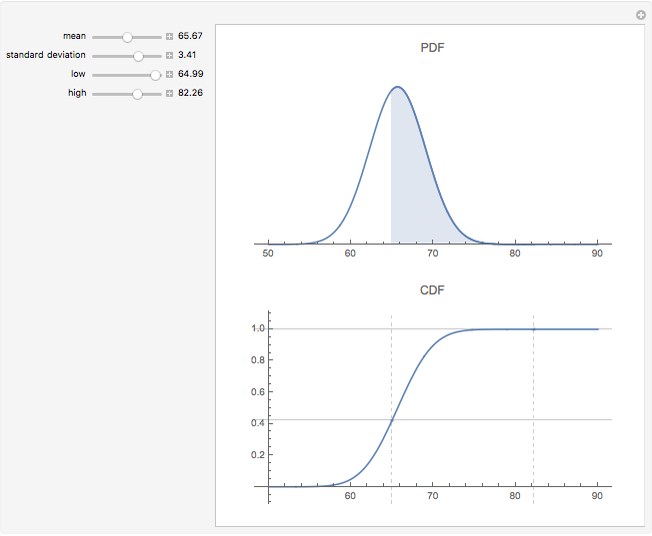

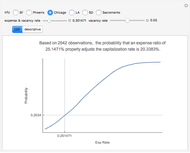

The calculations here are based on the normal distribution, which is completely determined by its mean and standard deviation. Changing these values changes the result of probability estimates. In the first snapshot you can see that the chance of seeing a value at or below 70 is approximately 81%. There is no need to subtract as in the default view because the lower bound of 50 is presumed to have a zero probability.

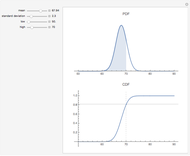

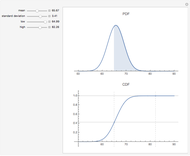

The second snapshot shows that it does not matter which side is filled. The procedure for finding the probability of particular random variables is the same. In the third snapshot the filled portion of the PDF plot is too narrow to visualize, a reminder that a single point has no probability mass for a continuous distribution. (To avoid problems in the illustration there is a tiny difference between the high and low points—65 versus 64.99—that may be ignored for purposes of the exposition.) The points in the CDF plot overlap visually, also showing that the probability of being between two values goes to zero as the values approach each other for a continuous distribution.

More information is available in Chapter Five of Private Real Estate Investment and at mathestate.com.

R. J. Brown, Private Real Estate Investment: Data Analysis and Decision Making, Burlington, MA: Elsevier Academic Press, 2005.

Snapshots

Permanent Citation

Exploring the Tails of the Normal Distribution

Exploring the Tails of the Normal Distribution

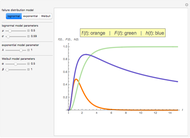

Joe O'Hara Comparing and Weighting Two Weibull Models

Comparing and Weighting Two Weibull Models

Frederick Wu Fitting Lifetime Data to a Weibull Model

Fitting Lifetime Data to a Weibull Model

Frederick Wu Normal Approximation to a Poisson Random Variable

Normal Approximation to a Poisson Random Variable

Chris Boucher Area of a Normal Distribution

Area of a Normal Distribution

Eric Schulz Logistic Sigmoid Market Model

Logistic Sigmoid Market Model

Michael Schreiber Reliability Distributions

Reliability Distributions

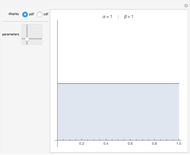

Joe O'Hara Beta Distribution

Beta Distribution

Fiona Maclachlan Uncertainty of Measurement and Diagnostic Accuracy Measures

Uncertainty of Measurement and Diagnostic Accuracy Measures

Aristides T. Hatjimihail The Exponential Distribution

The Exponential Distribution

Chris Boucher

-

Connecting the CDF and the PDF

Connecting the CDF and the PDF

Roger J. Brown -

Dissolving Partnerships

Dissolving Partnerships

Roger J. Brown -

Forming the Efficient Frontier When Returns Are Non-Normal

Forming the Efficient Frontier When Returns Are Non-Normal

Roger J. Brown -

Spectral Measures

Spectral Measures

Roger J. Brown -

Granger-Orr Running Variance Test

Granger-Orr Running Variance Test

Roger J. Brown -

Capitalization Rate Probability

Capitalization Rate Probability

Roger J. Brown -

Net Lease Economics

Net Lease Economics

Roger J. Brown -

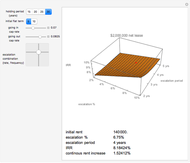

The Refinance Decision

The Refinance Decision

Roger J. Brown -

True Cost of Variable Rate Mortgage Funds

True Cost of Variable Rate Mortgage Funds

Roger J. Brown -

Term Structure of Interest Rates

Term Structure of Interest Rates

Roger J. Brown -

Generalized Central Limit Theorem

Generalized Central Limit Theorem

Roger J. Brown -

Inflation-Adjusted Yield

Inflation-Adjusted Yield

Roger J. Brown -

Simulating the IRR

Simulating the IRR

Roger J. Brown -

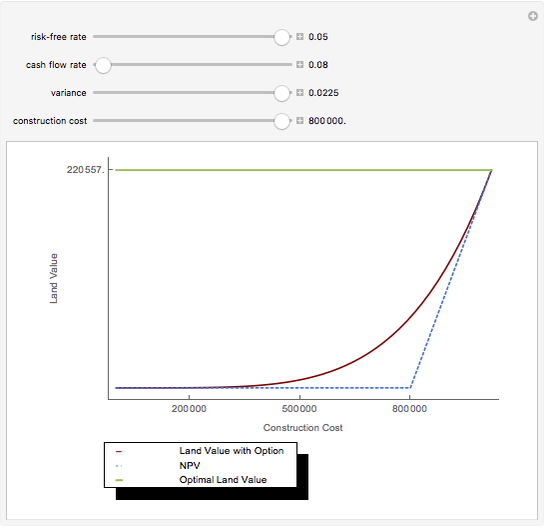

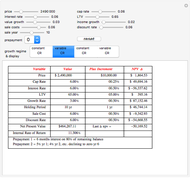

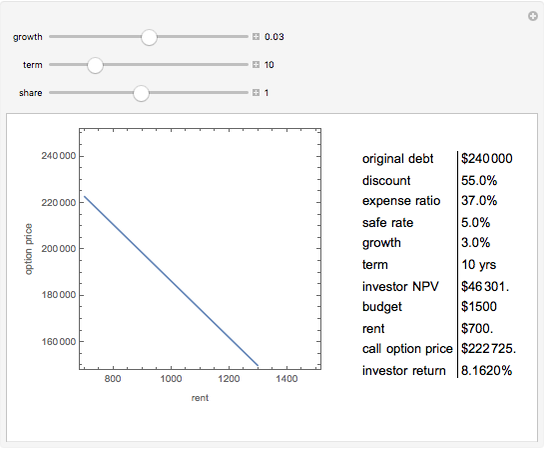

Real Options

Real Options

Roger J. Brown -

The Price-Terms Tradeoff

The Price-Terms Tradeoff

Roger J. Brown -

Fitting an Elephant

Fitting an Elephant

Roger J. Brown -

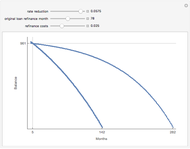

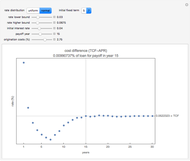

Solving the Subprime Loan Problem

Solving the Subprime Loan Problem

Roger J. Brown -

Why Location Matters: The Bid Rent Curve

Why Location Matters: The Bid Rent Curve

Roger J. Brown -

Explaining Real Estate Price Bubbles

Explaining Real Estate Price Bubbles

Roger J. Brown -

Value Added Growth Model

Value Added Growth Model

Roger J. Brown