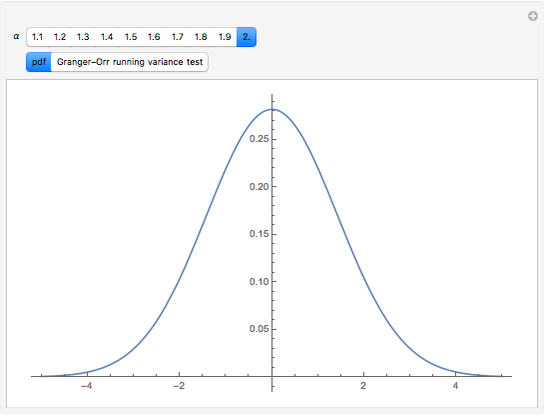

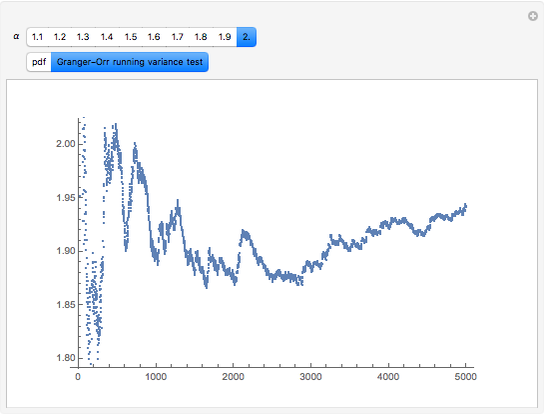

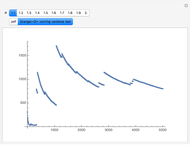

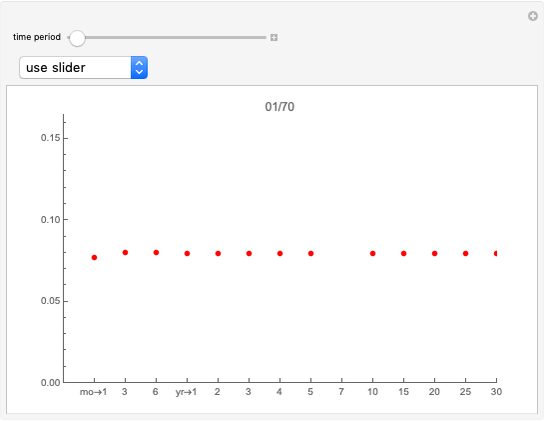

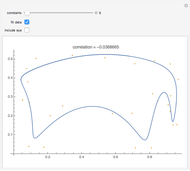

Granger-Orr Running Variance Test

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

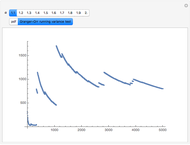

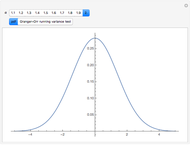

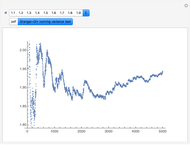

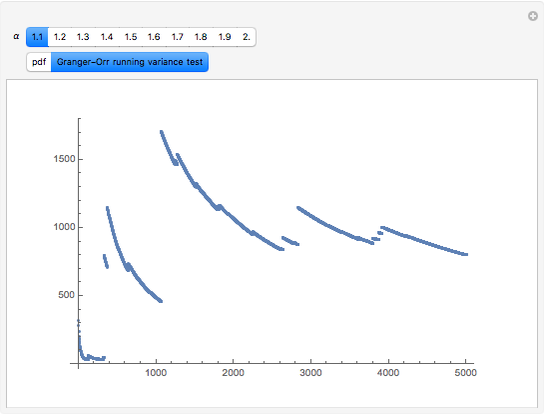

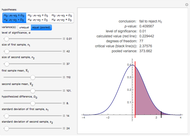

There is no test to prove a distribution is non-normal stable. However there are tests that indicate stability. One of these is a test for infinite variance. For the normal (a special case of stable) distribution the variance converges to a finite real number as  grows without bounds. When tails are heavy (stable

grows without bounds. When tails are heavy (stable  ) variance does not exist or is infinite. Granger and Orr (1972) devised a running variance test for infinite variance that is displayed here.

) variance does not exist or is infinite. Granger and Orr (1972) devised a running variance test for infinite variance that is displayed here.

Contributed by: Roger J. Brown (May 2009)

Reproduced by permission of Academic Press from Private Real Estate Investment ©2005

Open content licensed under CC BY-NC-SA

Snapshots

Details

The method of generating random variables used here is Chambers et al. Other approaches, based on their work, have been developed.

More information is available in chapter six of [3] and at mathestate.com.

References

[1] J. M. Chambers, C. L. Mallows, and B. W. Stuck, "A Method for Simulating Stable Random Variables," Journal of the American Statistical Association 71, 1976 pp. 1340–1344.

[2] C. W. J. Granger and D. Orr, "Infinite Variance and Research Strategy in Time Series Analysis," Journal of the American Statistical Association, 67(338), 1972 pp. 275-285.

[3] R. J. Brown, Private Real Estate Investment: Data Analysis and Decision Making, Burlington, MA: Elsevier Academic Press, 2005.

Permanent Citation

Predictive Scores and Ultimate Test Passage

Predictive Scores and Ultimate Test Passage

Seth J. Chandler Variance-Gamma Distribution

Variance-Gamma Distribution

Peter Falloon Variance-Bias Tradeoff

Variance-Bias Tradeoff

Ian McLeod Comparing Two Means Using Independent Samples of Unknown Variance

Comparing Two Means Using Independent Samples of Unknown Variance

Shailesh S. Kulkarni and Hakan Tarakci Power Curve of a Mean Test

Power Curve of a Mean Test

Sijia Liang and Bruce Atwood One-Sample t-Test and Confidence Interval with Dot Chart in Small Samples

One-Sample t-Test and Confidence Interval with Dot Chart in Small Samples

Douglas Woolford and Ian McLeod Generalized Central Limit Theorem

Generalized Central Limit Theorem

Roger J. Brown and Bob Rimmer Analysis of Diagnostic Accuracy Measures

Analysis of Diagnostic Accuracy Measures

Theodora Chatzimichail Binomial Probability Distribution

Binomial Probability Distribution

Paul Savory (University of Nebraska ? Lincoln) Intuitive Parameterization of the Bivariate Normal Distribution

Intuitive Parameterization of the Bivariate Normal Distribution

Robert L. Brown

-

Dissolving Partnerships

Dissolving Partnerships

Roger J. Brown -

Forming the Efficient Frontier When Returns Are Non-Normal

Forming the Efficient Frontier When Returns Are Non-Normal

Roger J. Brown -

Spectral Measures

Spectral Measures

Roger J. Brown -

Granger-Orr Running Variance Test

Granger-Orr Running Variance Test

Roger J. Brown -

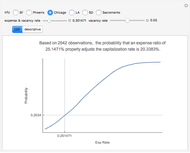

Capitalization Rate Probability

Capitalization Rate Probability

Roger J. Brown -

Net Lease Economics

Net Lease Economics

Roger J. Brown -

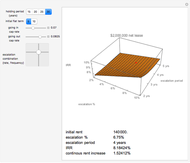

The Refinance Decision

The Refinance Decision

Roger J. Brown -

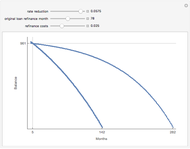

True Cost of Variable Rate Mortgage Funds

True Cost of Variable Rate Mortgage Funds

Roger J. Brown -

Term Structure of Interest Rates

Term Structure of Interest Rates

Roger J. Brown -

Generalized Central Limit Theorem

Roger J. Brown -

Inflation-Adjusted Yield

Inflation-Adjusted Yield

Roger J. Brown -

Simulating the IRR

Simulating the IRR

Roger J. Brown -

Real Options

Real Options

Roger J. Brown -

The Price-Terms Tradeoff

The Price-Terms Tradeoff

Roger J. Brown -

Fitting an Elephant

Fitting an Elephant

Roger J. Brown -

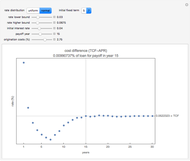

Solving the Subprime Loan Problem

Solving the Subprime Loan Problem

Roger J. Brown -

Why Location Matters: The Bid Rent Curve

Why Location Matters: The Bid Rent Curve

Roger J. Brown -

Explaining Real Estate Price Bubbles

Explaining Real Estate Price Bubbles

Roger J. Brown -

Value Added Growth Model

Value Added Growth Model

Roger J. Brown -

Connecting the CDF and the PDF

Connecting the CDF and the PDF

Roger J. Brown