The Variance Gamma Process

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

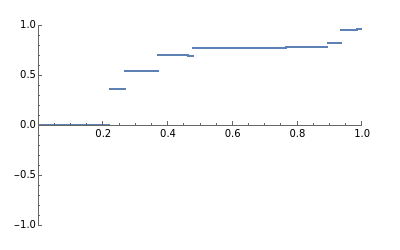

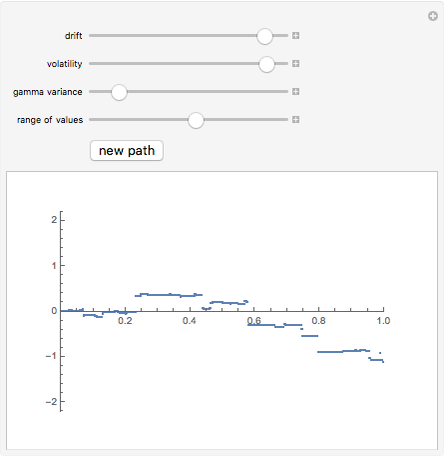

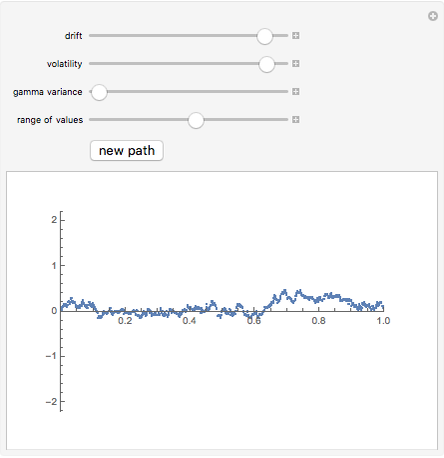

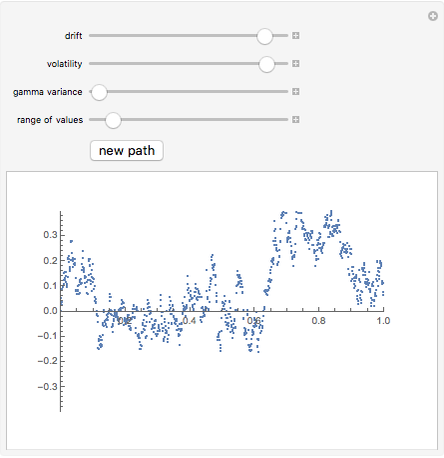

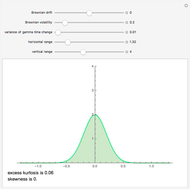

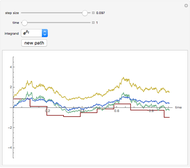

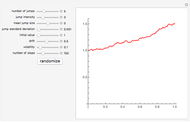

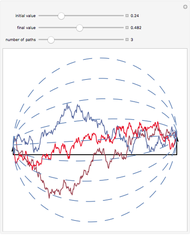

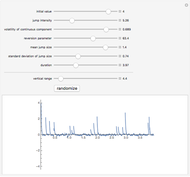

This Demonstration shows the path of a variance gamma process, a pure jump process of finite variation, but with infinitely many jumps. This process has been used in option pricing in place of Brownian motion, generally producing answers that agree better with empirical evidence. The process is constructed by means of "Brownian subordination", that is, by evaluating Brownian motion with drift at random times given by a gamma process. There are three basic controls: the volatility and drift of the Brownian motion and the variance of the gamma process. These parameters allow you to control the skewness and kurtosis of the return distribution in addition to mean and variance, as is the case with models based on Brownian motion.

[more]

Contributed by: Andrzej Kozlowski (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

The variance gamma stochastic process is a three-parameter generalization of the Brownian motion process. It is an example of the finite variation Lévy process. It has infinitely many jumps in any time interval, but only finitely many jumps larger than any given size. Like all finite variation processes, it can be written as the difference of two increasing processes, in this case gamma processes.

The variance gamma process was introduced into option pricing by Madan and Seneta [1] and generalized by Madan, Carr, and Chang [2]. Explicit formulas for European style options can be given, generalizing the Black–Scholes formulas. The model has been shown to perform better than the Black–Scholes model under the "historical approach" [3].

[1] D. B. Madan and E. Seneta, "The Variance Gamma Process (V.G.) Model for Share Market Returns," Journal of Business 63(4) pp. 511-524.

[2] D. B. Madan, P. P. Carr, and E. C. Chang, "The Variance Gamma Process and Option Pricing," European Finance Review 2(1), 1998 pp. 79-105.

[3] K. Lam, E. Chang, and M. C. Lee, "An Empirical Test of the Variance Gamma Option Pricing Model," Pacific Basin Finance Journal 10(3), 2002 pp. 267-285.

Permanent Citation

"The Variance Gamma Process"

http://demonstrations.wolfram.com/TheVarianceGammaProcess/

Wolfram Demonstrations Project

Published: March 7 2011

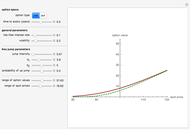

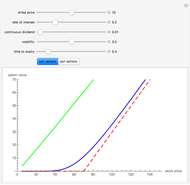

Option Prices in the Variance Gamma Model

Option Prices in the Variance Gamma Model

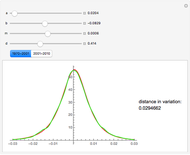

Andrzej Kozlowski The Return Distribution of the Variance Gamma Process

The Return Distribution of the Variance Gamma Process

Andrzej Kozlowski Correlated Wiener Processes

Correlated Wiener Processes

Andrzej Kozlowski Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski Correlated Gamma Variance Processes with Common Subordinator

Correlated Gamma Variance Processes with Common Subordinator

Andrzej Kozlowski The Itô Integral and Itô's Lemma

The Itô Integral and Itô's Lemma

Andrzej Kozlowski Merton's Jump Diffusion Model

Merton's Jump Diffusion Model

Andrzej Kozlowski Brownian Bridge

Brownian Bridge

Andrzej Kozlowski A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski Variance-Gamma Distribution

Variance-Gamma Distribution

Peter Falloon

-

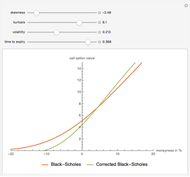

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

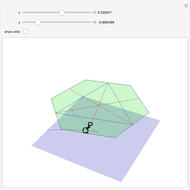

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

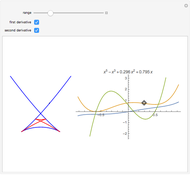

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski -

Newton Polygon and Branching of Algebraic Curves

Newton Polygon and Branching of Algebraic Curves

Andrzej Kozlowski -

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Andrzej Kozlowski -

The Space of Inner Products

The Space of Inner Products

Andrzej Kozlowski