The Poisson Process

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

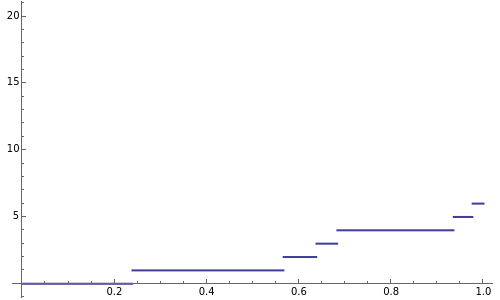

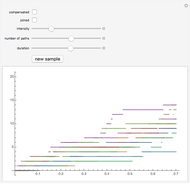

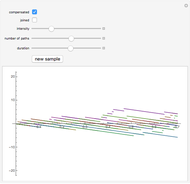

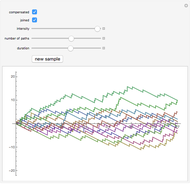

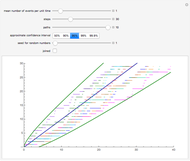

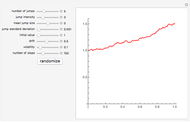

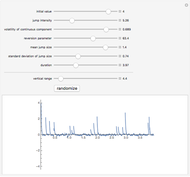

This Demonstration shows sample trajectories of a Poisson process—a fundamental example of a stochastic process with discontinuous trajectories, which is used as a building block for constructing jump processes that play an important role in modern financial modeling. You can vary the intensity of the jumps, the duration, whether the trajectories should be connected, and whether an ordinary Poisson process or a "compensated" one should be displayed.

Contributed by: Andrzej Kozlowski (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

The Poisson process is one of the two most fundamental stochastic processes in continuous time financial modelling, the other being Brownian motion, with which it shares a number of common properties (both are examples of a Levy process). In this Demonstration two kinds of Poisson processes are shown: an ordinary one and one that is "compensated". The compensated Poisson process is a martingale with expected value 0. As the intensity of jumps increases, the compensated Poisson process approximates a Brownian motion (this follows from the Donsker invariance principle). Making the plot joined and choosing a high value for the intensity makes the trajectories resemble those in standard simulations of Brownian motion.

R. Cont, P. Tankov, Financial Modelling with Jump Processes, Boca Raton, London, New York, Washington, D.C: Chapman & Hall, 2004.

Permanent Citation

"The Poisson Process"

http://demonstrations.wolfram.com/ThePoissonProcess/

Wolfram Demonstrations Project

Published: March 7 2011

The Return Distribution of the Variance Gamma Process

The Return Distribution of the Variance Gamma Process

Andrzej Kozlowski Correlated Wiener Processes

Correlated Wiener Processes

Andrzej Kozlowski Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski Simulating the Poisson Process

Simulating the Poisson Process

Heikki Ruskeepää Merton's Jump Diffusion Model

Merton's Jump Diffusion Model

Andrzej Kozlowski Brownian Bridge

Brownian Bridge

Andrzej Kozlowski Correlated Gamma Variance Processes with Common Subordinator

Correlated Gamma Variance Processes with Common Subordinator

Andrzej Kozlowski Generalized Hyperbolic Distribution

Generalized Hyperbolic Distribution

Andrzej Kozlowski Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski The Normal Inverse Gaussian Lévy Process

The Normal Inverse Gaussian Lévy Process

Piotr Teklinski, Piotr Wroblewski, and Andrzej Kozlowski

-

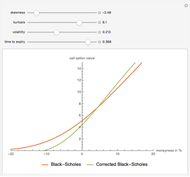

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

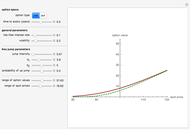

Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

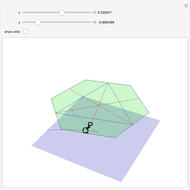

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

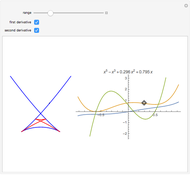

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski -

Newton Polygon and Branching of Algebraic Curves

Newton Polygon and Branching of Algebraic Curves

Andrzej Kozlowski -

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Andrzej Kozlowski -

The Space of Inner Products

The Space of Inner Products

Andrzej Kozlowski