Adaptive Monte Carlo Integration

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

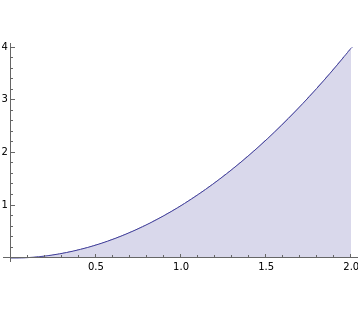

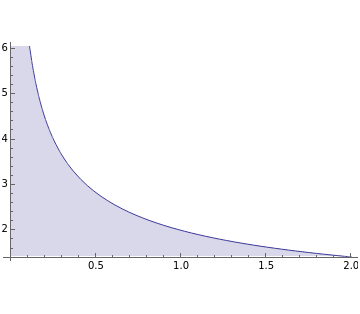

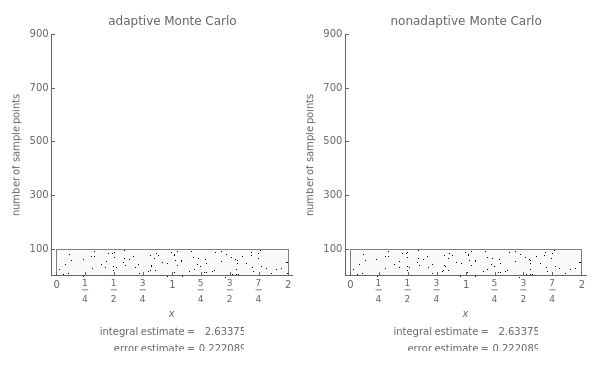

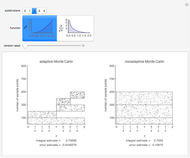

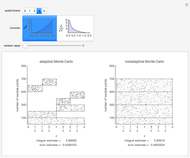

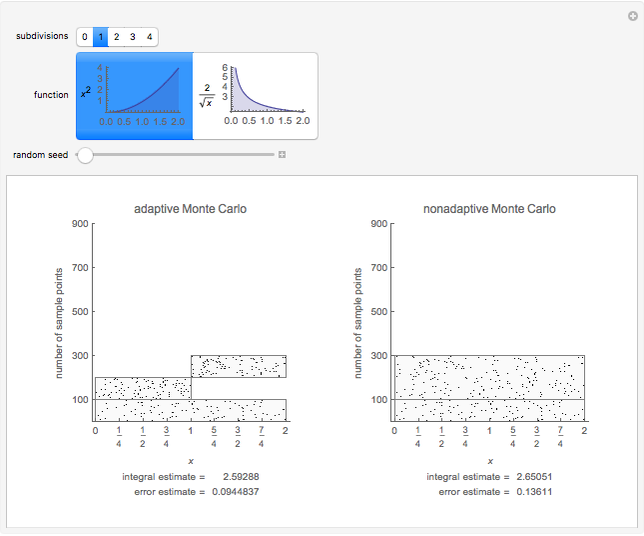

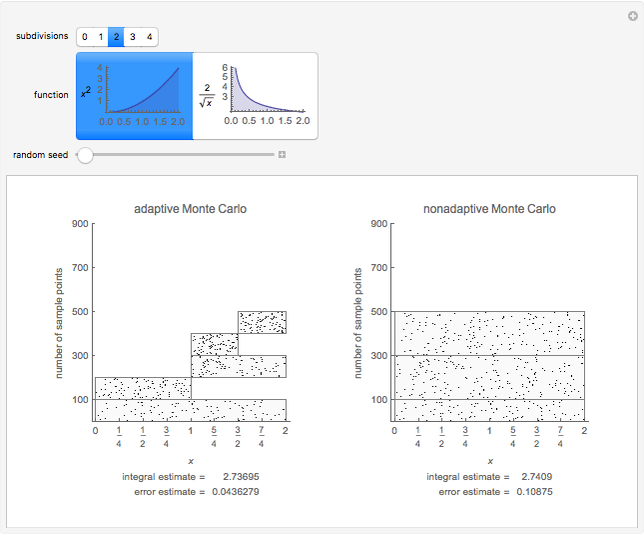

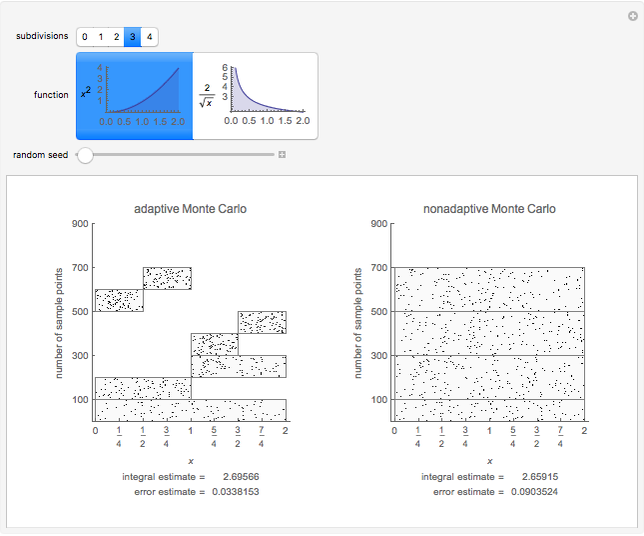

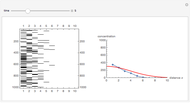

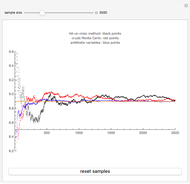

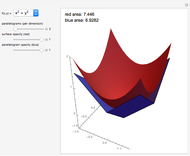

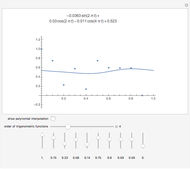

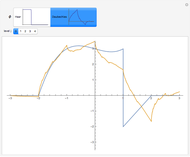

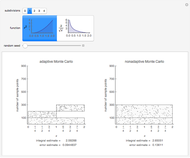

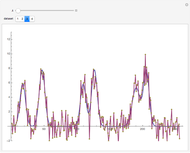

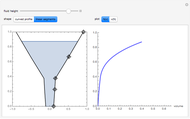

This Demonstration compares adaptive and nonadaptive Monte Carlo integration for two different functions,  and

and  . The plot shows the places on the interval

. The plot shows the places on the interval  where sample points are added as the number of sample points is increased. The actual values of the integrals to six significant figures are 2.66667 and 5.65685. The adaptive technique generally gets better estimates with the same number of sample points by subdividing the subinterval with the highest error estimate. Normally this process would be repeated until some error criterion is satisfied, but in this Demonstration only four subdivisions are shown.

where sample points are added as the number of sample points is increased. The actual values of the integrals to six significant figures are 2.66667 and 5.65685. The adaptive technique generally gets better estimates with the same number of sample points by subdividing the subinterval with the highest error estimate. Normally this process would be repeated until some error criterion is satisfied, but in this Demonstration only four subdivisions are shown.

Contributed by: Sijia Liang and Bruce Atwood (January 2013)

(Beloit College)

Open content licensed under CC BY-NC-SA

Snapshots

Details

In one dimension, if  is integrable on the interval

is integrable on the interval  , then the average value of is

, then the average value of is  . From this, the nonadaptive (basic) Monte Carlo method estimates the integral by

. From this, the nonadaptive (basic) Monte Carlo method estimates the integral by  , where

, where  is the mean of the function evaluated at

is the mean of the function evaluated at  randomly sampled points. The corresponding error estimate is

randomly sampled points. The corresponding error estimate is  , where

, where  is the variance of the function evaluations. Thus the error can be reduced by increasing the number of sample points or reducing the variance. The key idea of adaptive Monte Carlo is to reduce the variance by recursive subdivision. Parts of this Demonstration are modifications of examples from the Wolfram Mathematica Documentation Center tutorial "Advanced Numerical Integration in Mathematica" (see link below). Students should try to explain why Monte Carlo integration has more difficulty for the function with the singularity at 0. (Hint: look at the formulas for the integral estimate and error estimate.)

is the variance of the function evaluations. Thus the error can be reduced by increasing the number of sample points or reducing the variance. The key idea of adaptive Monte Carlo is to reduce the variance by recursive subdivision. Parts of this Demonstration are modifications of examples from the Wolfram Mathematica Documentation Center tutorial "Advanced Numerical Integration in Mathematica" (see link below). Students should try to explain why Monte Carlo integration has more difficulty for the function with the singularity at 0. (Hint: look at the formulas for the integral estimate and error estimate.)

Permanent Citation

Monte Carlo Estimation of Area

Monte Carlo Estimation of Area

Mark D. Normand and Micha Peleg Area Bisectors via Monte Carlo

Area Bisectors via Monte Carlo

Ed Pegg Jr Approximating Pi by the Monte Carlo Method

Approximating Pi by the Monte Carlo Method

Zubeyir Cinkir Numerical Integration using Rectangles, the Trapezoidal Rule, or Simpson's Rule

Numerical Integration using Rectangles, the Trapezoidal Rule, or Simpson's Rule

Bartosz Naskrecki Simulation of 1D Diffusion Using the Monte Carlo Method

Simulation of 1D Diffusion Using the Monte Carlo Method

Quang-Dao Trinh Monte Carlo Methods to Estimate Area

Monte Carlo Methods to Estimate Area

Tomas Garza Two-Dimensional Integrals Using the Monte Carlo Method

Two-Dimensional Integrals Using the Monte Carlo Method

Housam Binous, Brian G. Higgins, and Ahmed Bellagi Integration by Riemann Sums

Integration by Riemann Sums

Jiwon Hwang Simulation of 3D Diffusion Using the Monte Carlo Method

Simulation of 3D Diffusion Using the Monte Carlo Method

Quang-Dao Trinh Finding the Area of a 3D Surface with Parallelograms

Finding the Area of a 3D Surface with Parallelograms

Mark Peterson

-

Trigonometric Fitting and Interpolation

Trigonometric Fitting and Interpolation

Bruce Atwood -

Balancing a Can on Its Edge

Balancing a Can on Its Edge

Bruce Atwood -

Spinning Out Sine and Cosine

Spinning Out Sine and Cosine

Bruce Atwood -

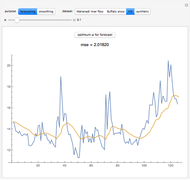

Forecasting with Exponential Moving Averages

Forecasting with Exponential Moving Averages

Bruce Atwood -

Convolution Sum

Convolution Sum

Bruce Atwood -

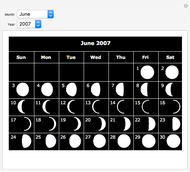

Lunar Calendar Maker

Lunar Calendar Maker

Bruce Atwood -

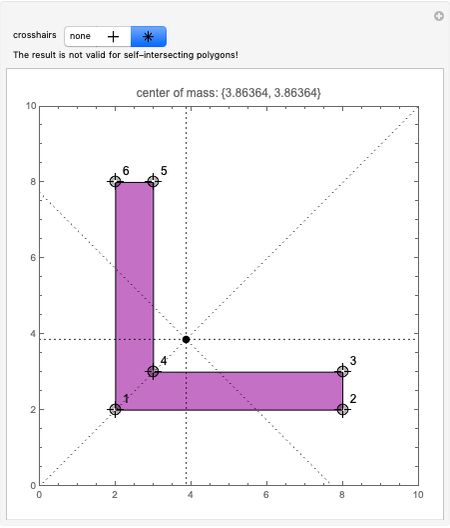

Center of Mass of a Polygon

Center of Mass of a Polygon

Bruce Atwood -

Projection into Spaces Generated by Haar and Daubechies Scaling Functions

Projection into Spaces Generated by Haar and Daubechies Scaling Functions

Bruce Atwood -

Adaptive Monte Carlo Integration

Adaptive Monte Carlo Integration

Bruce Atwood -

The Polar Planimeter

The Polar Planimeter

Bruce Atwood -

Reconstructing a Sampled Signal Using Interpolation

Reconstructing a Sampled Signal Using Interpolation

Bruce Atwood -

Bootstrap Percentile Confidence Intervals

Bootstrap Percentile Confidence Intervals

Bruce Atwood -

Power Curve of a Mean Test

Power Curve of a Mean Test

Bruce Atwood -

Approximating Continuous Functions with Haar Approximations

Approximating Continuous Functions with Haar Approximations

Bruce Atwood -

Sliding to the Fermat Point

Sliding to the Fermat Point

Bruce Atwood -

Wavelet Shrinkage Denoising

Wavelet Shrinkage Denoising

Bruce Atwood -

Filling a Container Defined by a Curve

Filling a Container Defined by a Curve

Bruce Atwood -

Squeeze Theorem

Squeeze Theorem

Bruce Atwood -

Signed Area of a Polygon

Signed Area of a Polygon

Bruce Atwood -

Bézier Curve by de Casteljau's Algorithm

Bézier Curve by de Casteljau's Algorithm

Bruce Atwood