The Method of Common Random Numbers: An Example

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

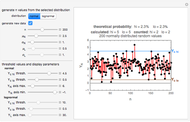

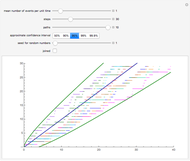

Variance reduction is of great interest to the creators of Monte Carlo experiments. For example, investment banks use very complicated Monte Carlo simulations to price esoteric mortgage-backed securities. These simulations often run overnight because many Monte Carlo trials are necessary to obtain (by the central limit theorem) a point estimate of some true population parameter, bounded by a relatively small confidence interval. One way to reduce the number of required Monte Carlo trials is to use a variance reduction technique.

[more]

Contributed by: Jeff Hamrick (March 2011)

Open content licensed under CC BY-NC-SA

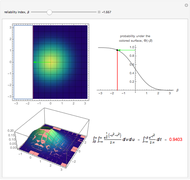

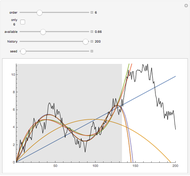

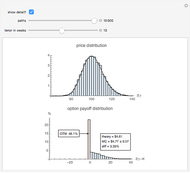

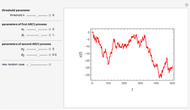

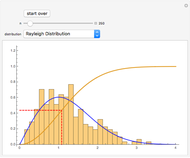

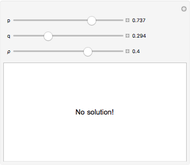

Snapshots

Details

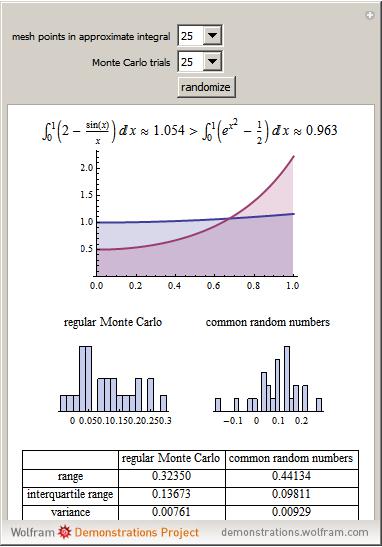

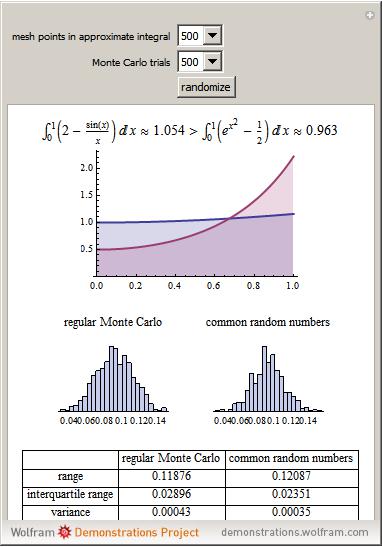

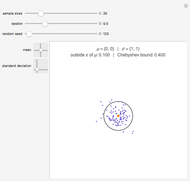

This method of common numbers produces good, but not overwhelming, variance reduction. The method of common random numbers (also known as the method of correlated sampling, the method of matched pairs, or the method of matched sampling) does not always work. It can backfire if the the engineer of the Monte Carlo simulation creates a negative, rather than positive, correlation between the two random variables  and

and  . Often, it is useful to choose

. Often, it is useful to choose  , which we do in this example.

, which we do in this example.

Why does this method work?

Recall that, for example,  is a sequence of independent, identically distributed random variables. The variance of the first Monte Carlo method, when is independent of , is

is a sequence of independent, identically distributed random variables. The variance of the first Monte Carlo method, when is independent of , is

.

.

Now consider the second Monte Carlo method, the method of common random numbers. The variance of this Monte Carlo method, when is positively correlated to , is

and therefore

.

.

If we make the additional assumption that  and

and  are either: (a) both monotonically nondecreasing; or (b) both monotonically nonincreasing, then

are either: (a) both monotonically nondecreasing; or (b) both monotonically nonincreasing, then

,

,

and we see that  .

.

Notice that in both cases, and have the identical marginals—the method of common numbers only permits us to manipulate the joint distribution of and . Also, notice that in our example, both  and

and  are strictly monotonically increasing.

are strictly monotonically increasing.

In this particular example, the variance reduction is always successful. However, notice that other measures of dispersion—like the range or the interquartile range—are not always reduced by the technique.

There are more powerful variance reduction techniques available, including antithetic variates, control variates, importance sampling, and stratified sampling. For more information on the method of common random numbers, see Sheldon Ross's textbook Stochastic Processes or Paul Glasserman's book on Monte Carlo methods.

Permanent Citation

Mean-Reverting Random Walks

Mean-Reverting Random Walks

Jason Cawley Failure Probabilities from Quality Control Charts

Failure Probabilities from Quality Control Charts

Mark D. Normand and Micha Peleg Reliability Analysis and Failure Probability Using First-Order Reliability Method

Reliability Analysis and Failure Probability Using First-Order Reliability Method

Diego M. Oviedo Salcedo Polynomial Fits of Random Walks

Polynomial Fits of Random Walks

Michael Schreiber Monte Carlo Valuation of an Option

Monte Carlo Valuation of an Option

N. T. Gladd Simulating the Poisson Process

Simulating the Poisson Process

Heikki Ruskeepää Two-Regime Threshold Autoregressive Model Simulation

Two-Regime Threshold Autoregressive Model Simulation

Jozef Barunik The Method of Inverse Transforms

The Method of Inverse Transforms

Ryan Carroll, Adam Joplin, Jeff Hamrick, and Eric Stradley Linear Dependence between Two Bernoulli Random Variables

Linear Dependence between Two Bernoulli Random Variables

Jeff Hamrick Chebyshev's Inequality and the Weak Law of Large Numbers for iid Two-Vectors

Chebyshev's Inequality and the Weak Law of Large Numbers for iid Two-Vectors

Jeff Bryant and Chris Boucher

-

Expected Returns of the Dow Industrials, Beta Model

Expected Returns of the Dow Industrials, Beta Model

Jeff Hamrick -

Exploring Measures of Association

Exploring Measures of Association

Jeff Hamrick -

Bootstrapping Credit Default Swap Data

Bootstrapping Credit Default Swap Data

Jeff Hamrick -

Linear Dependence between Two Bernoulli Random Variables

Jeff Hamrick -

Estimating the Local Mean Function

Estimating the Local Mean Function

Jeff Hamrick -

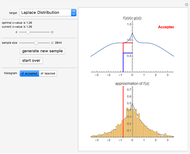

Acceptance/Rejection Sampling

Acceptance/Rejection Sampling

Jeff Hamrick -

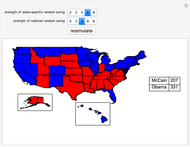

Simulating the 2008 U.S. Presidential Election

Simulating the 2008 U.S. Presidential Election

Jeff Hamrick -

The Method of Inverse Transforms

Jeff Hamrick -

The Perturbed Rat

The Perturbed Rat

Jeff Hamrick -

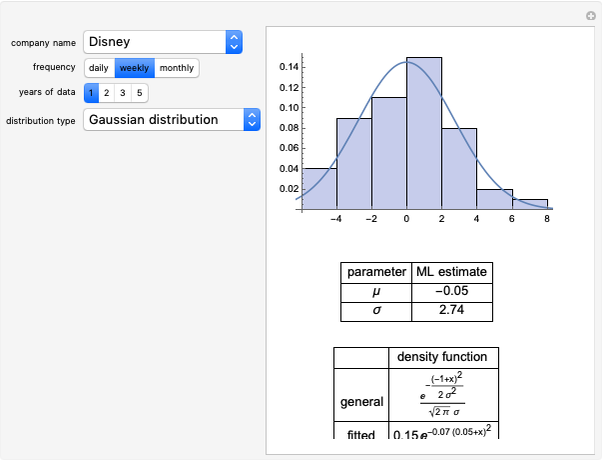

Modeling Return Distributions

Modeling Return Distributions

Jeff Hamrick -

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Jeff Hamrick -

The Method of Common Random Numbers: An Example

The Method of Common Random Numbers: An Example

Jeff Hamrick -

The Envelope Theorem: Numerical Examples

The Envelope Theorem: Numerical Examples

Jeff Hamrick -

Bootstrapping to Compute Value-at-Risk Standard Errors

Bootstrapping to Compute Value-at-Risk Standard Errors

Jeff Hamrick -

Expected Returns of the Dow Industrials, Fama-French Model

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick -

Kernel Density Estimation

Kernel Density Estimation

Jeff Hamrick -

Simulating Asset Prices with a GARCH(1,1) Model

Simulating Asset Prices with a GARCH(1,1) Model

Jeff Hamrick