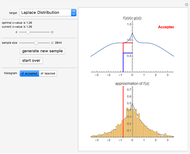

Acceptance/Rejection Sampling

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

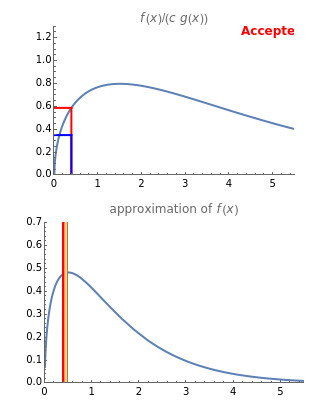

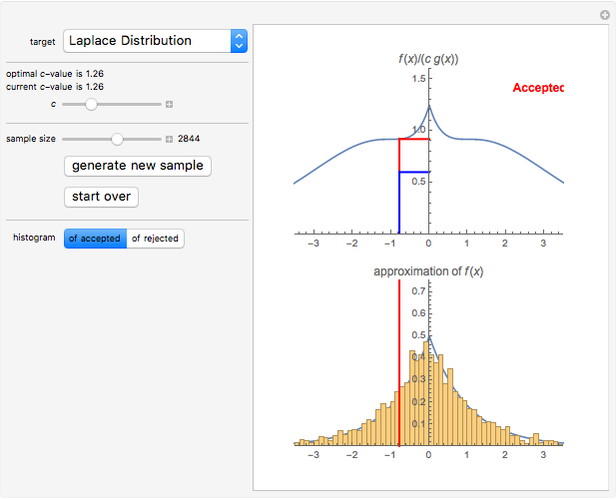

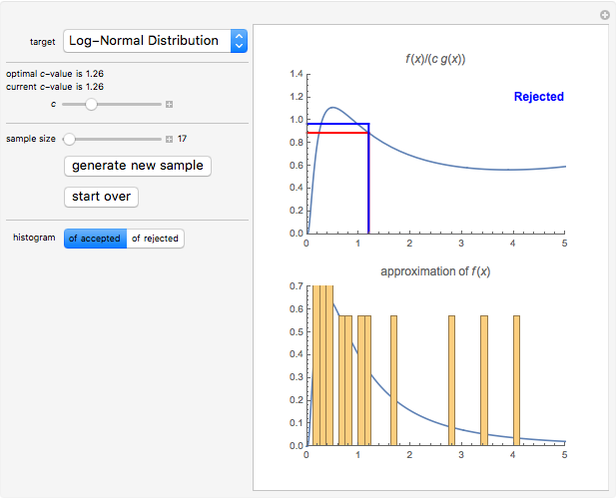

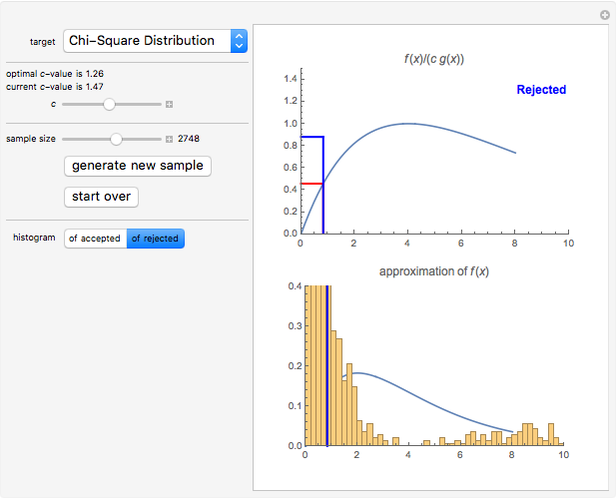

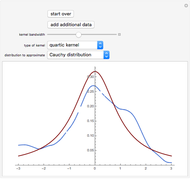

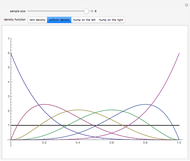

With this Demonstration, you can visualize the rejection sampling technique, which is also known as the acceptance-rejection algorithm. Select a target distribution (the distribution from which you would like to generate random samples) and then choose a "threshold value"  that influences the likelihood that a candidate sample from a nontarget distribution will be "accepted" as if it were, in fact, from the target distribution. You can change the number of random variates generated and view histograms of both the accepted and the rejected samples.

that influences the likelihood that a candidate sample from a nontarget distribution will be "accepted" as if it were, in fact, from the target distribution. You can change the number of random variates generated and view histograms of both the accepted and the rejected samples.

Contributed by: Ryan Carroll and Jeff Hamrick (September 2011)

Open content licensed under CC BY-NC-SA

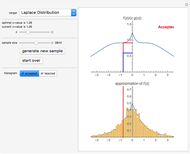

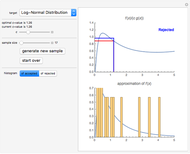

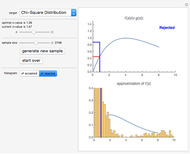

Snapshots

Details

Suppose that you want to generate pseudorandom numbers from a random variable  with probability distribution

with probability distribution  , but that other methods (like the method of inverse transforms) do not work well (perhaps because the cumulative distribution function associated with does not have an explicit inverse). Instead, choose a companion random variable

, but that other methods (like the method of inverse transforms) do not work well (perhaps because the cumulative distribution function associated with does not have an explicit inverse). Instead, choose a companion random variable  with probability density function

with probability density function  , making sure that and have the same support (i.e. both vanish and fail to vanish over the same sets of real numbers).

, making sure that and have the same support (i.e. both vanish and fail to vanish over the same sets of real numbers).

Ideally, the random variable has been chosen in such a way that the cumulative distribution function associated with has an explicit inverse and is easy to simulate using a technique like the method of inverse transforms.

The acceptance-rejection algorithm is then as follows: (1) independently simulate a random number  with a uniform distribution over the unit interval and a realization * of the random variable ; and then (2) using a fixed, strictly positive number , accept * as a realization of if

with a uniform distribution over the unit interval and a realization * of the random variable ; and then (2) using a fixed, strictly positive number , accept * as a realization of if  , where

, where  and

and  are the probability densities of the random variables and , respectively. If

are the probability densities of the random variables and , respectively. If  is not accepted, it is rejected. This process is continued repeatedly until a target number of realizations of is generated.

is not accepted, it is rejected. This process is continued repeatedly until a target number of realizations of is generated.

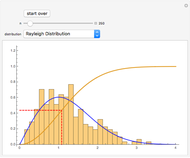

Heuristically, the acceptance-rejection method works particularly efficiently when certain conditions are satisfied. First, the target random variable and the companion random variable should have density functions that "look" as similar as possible. In this Demonstration, we use the exponential random variable as a companion random variable for the probability distributions with support on the positive part of the real line (the gamma distribution, chi-square distribution, half-normal distribution, and log-normal distribution). We use the Cauchy distribution as the companion distribution for the probability distributions with support over the whole real line (the normal distribution, the Student t distribution, the Gumbel distribution, and the Laplace distribution).

Second, the strictly positive constant influences the tendency of the algorithm to "accept" instead of "reject". If is particularly large, will be less than  with small probability, and the algorithm will throw away many fine proxies for . On the other hand, if is particularly close to zero and

with small probability, and the algorithm will throw away many fine proxies for . On the other hand, if is particularly close to zero and  is not substantially smaller than

is not substantially smaller than  , then will probably be accepted. It can be shown that the acceptance-rejection algorithm produces an empirical distribution of pseudorandom numbers that converges the most rapidly to the target distribution if is chosen to be the maximum possible value of

, then will probably be accepted. It can be shown that the acceptance-rejection algorithm produces an empirical distribution of pseudorandom numbers that converges the most rapidly to the target distribution if is chosen to be the maximum possible value of  over the (common) support of and .

over the (common) support of and .

The acceptance-rejection method can be generalized to the Metropolis–Hastings algorithm and is a type of Markov chain Monte Carlo simulation. For further information about the acceptance-rejection algorithm, see [1] or [2].

References

[1] S. M. Ross, Simulation, 4th ed., Boston: Elsevier, 2006.

[2] S. Ghahramani, Fundamentals of Probability, with Stochastic Processes, 3rd ed., New York: Prentice Hall, 2004.

Permanent Citation

Sampling Theorem

Sampling Theorem

Carsten Roppel Kernel Density Estimation

Kernel Density Estimation

Jeff Hamrick Closed-Form Full Life Cycle Distribution

Closed-Form Full Life Cycle Distribution

Kelly S. Lowder Estimating a Distribution Function Subject to a Stochastic Order Restriction

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Michail Bozoudis and Vasileios Papachatzis Bootstrap Percentile Confidence Intervals

Bootstrap Percentile Confidence Intervals

Sijia Liang and Bruce Atwood Records in Sequences of Random Variables

Records in Sequences of Random Variables

Heikki Ruskeepää Distributions of Order Statistics

Distributions of Order Statistics

Chris Boucher Polynomial Fits of Random Walks

Polynomial Fits of Random Walks

Michael Schreiber Comparing Binomial Generalized Linear Models

Comparing Binomial Generalized Linear Models

Darren Glosemeyer Comparing Some Residuals for Generalized Linear Models

Comparing Some Residuals for Generalized Linear Models

Darren Glosemeyer

-

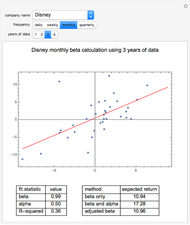

Expected Returns of the Dow Industrials, Beta Model

Expected Returns of the Dow Industrials, Beta Model

Jeff Hamrick -

Exploring Measures of Association

Exploring Measures of Association

Jeff Hamrick -

Bootstrapping Credit Default Swap Data

Bootstrapping Credit Default Swap Data

Jeff Hamrick -

Linear Dependence between Two Bernoulli Random Variables

Linear Dependence between Two Bernoulli Random Variables

Jeff Hamrick -

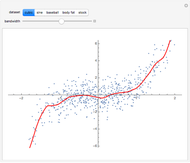

Estimating the Local Mean Function

Estimating the Local Mean Function

Jeff Hamrick -

Acceptance/Rejection Sampling

Acceptance/Rejection Sampling

Jeff Hamrick -

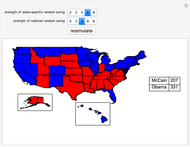

Simulating the 2008 U.S. Presidential Election

Simulating the 2008 U.S. Presidential Election

Jeff Hamrick -

The Method of Inverse Transforms

The Method of Inverse Transforms

Jeff Hamrick -

The Perturbed Rat

The Perturbed Rat

Jeff Hamrick -

Modeling Return Distributions

Modeling Return Distributions

Jeff Hamrick -

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Jeff Hamrick -

The Method of Common Random Numbers: An Example

The Method of Common Random Numbers: An Example

Jeff Hamrick -

The Envelope Theorem: Numerical Examples

The Envelope Theorem: Numerical Examples

Jeff Hamrick -

Bootstrapping to Compute Value-at-Risk Standard Errors

Bootstrapping to Compute Value-at-Risk Standard Errors

Jeff Hamrick -

Expected Returns of the Dow Industrials, Fama-French Model

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick -

Kernel Density Estimation

Jeff Hamrick -

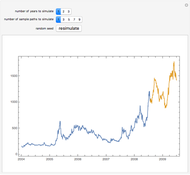

Simulating Asset Prices with a GARCH(1,1) Model

Simulating Asset Prices with a GARCH(1,1) Model

Jeff Hamrick