Simulating Asset Prices with a GARCH(1,1) Model

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

Independent, identically distributed, properly scaled Gaussian random numbers are the foundation upon which Brownian motion, geometric Brownian motion, and a wide variety of other diffusions are simulated. The GARCH model is different: the variance of today's return depends conditionally on (a) the variance of yesterday's return, and (b) the square of yesterday's return.

Contributed by: Jeff Hamrick (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

We aim to simulate an asset price trajectory over 251 days in a way that captures stylized observations about asset returns like volatility clustering, heavy tails, and serial correlation. A GARCH model is one way to capture these stylized observations. The GARCH model is an extension of the autoregressive conditional heteroskedasticity (ARCH) model developed by Engle in 1982. The acronym "GARCH" means "generalized autoregressive condition heteroskedasticity" model.

We model the log-return time series by  , where

, where  is an independent, identically distributed sequence of properly scaled Gaussian random numbers. The variance is dynamic and is governed by the equation

is an independent, identically distributed sequence of properly scaled Gaussian random numbers. The variance is dynamic and is governed by the equation  . We refer to

. We refer to  as the "state memory factor" and

as the "state memory factor" and  as the "variance memory factor". If

as the "variance memory factor". If  and

and  , then the variance does not change and we obtain a discrete white noise. Note that you also have control over the initial variance

, then the variance does not change and we obtain a discrete white noise. Note that you also have control over the initial variance  .

.

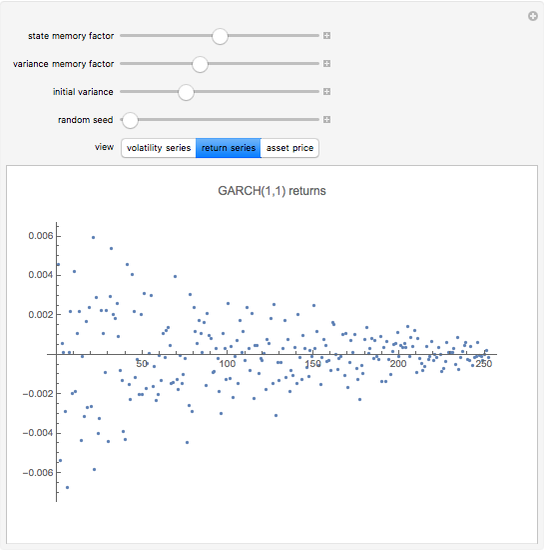

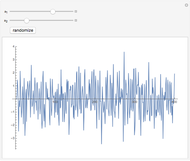

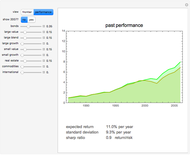

We make three views available to the user. The first view features the volatility series  . The most important feature of a GARCH model is the non-constant volatility series. Notice, e.g. the first snapshot, that making the variance memory factor too small causes the volatility series to tend to zero—which produces an unrealistic model of a real asset's returns.

. The most important feature of a GARCH model is the non-constant volatility series. Notice, e.g. the first snapshot, that making the variance memory factor too small causes the volatility series to tend to zero—which produces an unrealistic model of a real asset's returns.

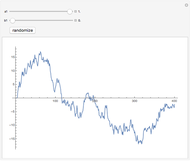

The second view features the log-return series. This series is used to construct the asset price in the third view. Again, notice that a poor choice of parameters—making the state memory or variance memory factor too large—generally causes the variance to explode.

Examples of state memory and variance memory factors that produce realistic-looking asset returns include (2.72, 0.99), (8.1, 0.97), and (16.3, 0.94). The GARCH models are generally quite sensitive to parameter choices. This sensitivity is problematic when estimating GARCH parameters from real data.

Instead of having the variance of today's return depend on yesterday's variance and yesterday's squared return, we could have allowed today's return to depend on the variance and squared returns from multiple prior days. In general, if the process depends on the past  days' squared returns and the past

days' squared returns and the past  days' variances, the process is called a GARCH

days' variances, the process is called a GARCH process. For sake of simplicity, we simulate only the log-returns and associated asset price of a GARCH

process. For sake of simplicity, we simulate only the log-returns and associated asset price of a GARCH process.

process.

Wolfram Research's Time Series package makes it trivial to simulate GARCH processes, but you can still simulate these processes with a few lines of your own code.

Permanent Citation

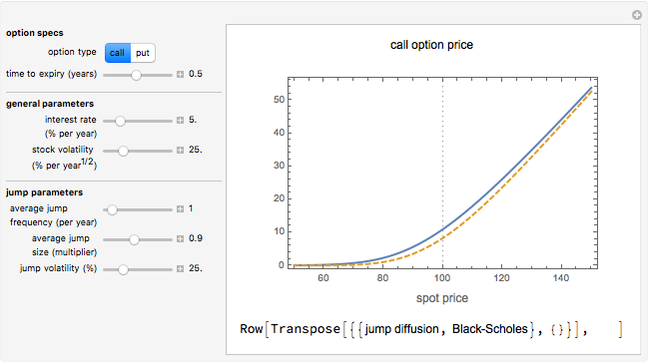

Merton's Jump Diffusion Model

Merton's Jump Diffusion Model

Andrzej Kozlowski Markov Volatility Random Walks

Markov Volatility Random Walks

Jason Cawley Mean-Reverting Random Walks

Mean-Reverting Random Walks

Jason Cawley Minimal Model of Simulating Prices of Financial Securities Using an Iterated Finite Automaton

Minimal Model of Simulating Prices of Financial Securities Using an Iterated Finite Automaton

Philip Maymin Option Prices in Merton's Jump Diffusion Model

Option Prices in Merton's Jump Diffusion Model

Peter Falloon Auto-Regressive Simulation (Second-Order)

Auto-Regressive Simulation (Second-Order)

David von Seggern (University of Nevada) Autoregressive Moving-Average Simulation (First Order)

Autoregressive Moving-Average Simulation (First Order)

David von Seggern (University of Nevada) Asset Allocation

Asset Allocation

Jason Cawley Exploring Minimal Models of the Complexity of Security Prices

Exploring Minimal Models of the Complexity of Security Prices

Philip Maymin Two-Asset Markowitz Feasible Set

Two-Asset Markowitz Feasible Set

Jim R Larkin

-

Expected Returns of the Dow Industrials, Beta Model

Expected Returns of the Dow Industrials, Beta Model

Jeff Hamrick -

Exploring Measures of Association

Exploring Measures of Association

Jeff Hamrick -

Bootstrapping Credit Default Swap Data

Bootstrapping Credit Default Swap Data

Jeff Hamrick -

Linear Dependence between Two Bernoulli Random Variables

Linear Dependence between Two Bernoulli Random Variables

Jeff Hamrick -

Estimating the Local Mean Function

Estimating the Local Mean Function

Jeff Hamrick -

Acceptance/Rejection Sampling

Acceptance/Rejection Sampling

Jeff Hamrick -

Simulating the 2008 U.S. Presidential Election

Simulating the 2008 U.S. Presidential Election

Jeff Hamrick -

The Method of Inverse Transforms

The Method of Inverse Transforms

Jeff Hamrick -

The Perturbed Rat

The Perturbed Rat

Jeff Hamrick -

Modeling Return Distributions

Modeling Return Distributions

Jeff Hamrick -

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Jeff Hamrick -

The Method of Common Random Numbers: An Example

The Method of Common Random Numbers: An Example

Jeff Hamrick -

The Envelope Theorem: Numerical Examples

The Envelope Theorem: Numerical Examples

Jeff Hamrick -

Bootstrapping to Compute Value-at-Risk Standard Errors

Bootstrapping to Compute Value-at-Risk Standard Errors

Jeff Hamrick -

Expected Returns of the Dow Industrials, Fama-French Model

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick -

Kernel Density Estimation

Kernel Density Estimation

Jeff Hamrick -

Simulating Asset Prices with a GARCH(1,1) Model

Simulating Asset Prices with a GARCH(1,1) Model

Jeff Hamrick