Bootstrapping Credit Default Swap Data

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

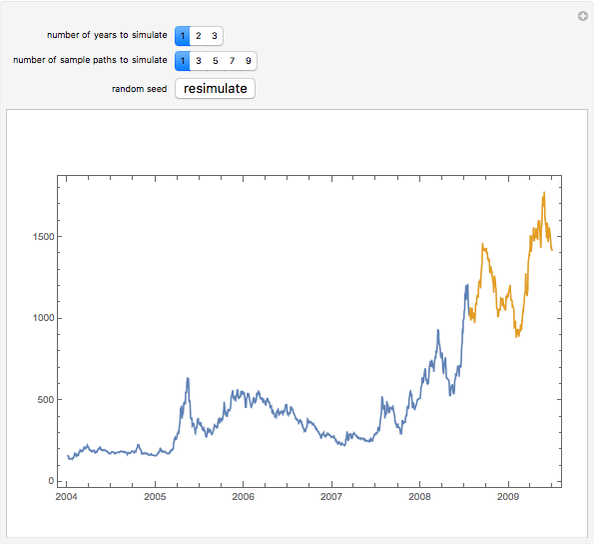

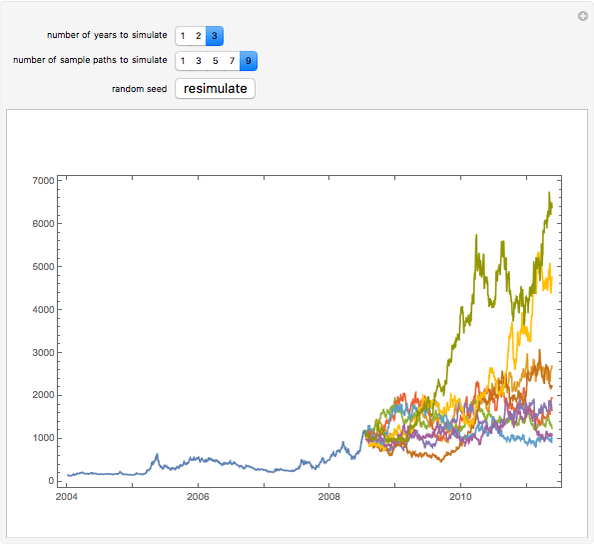

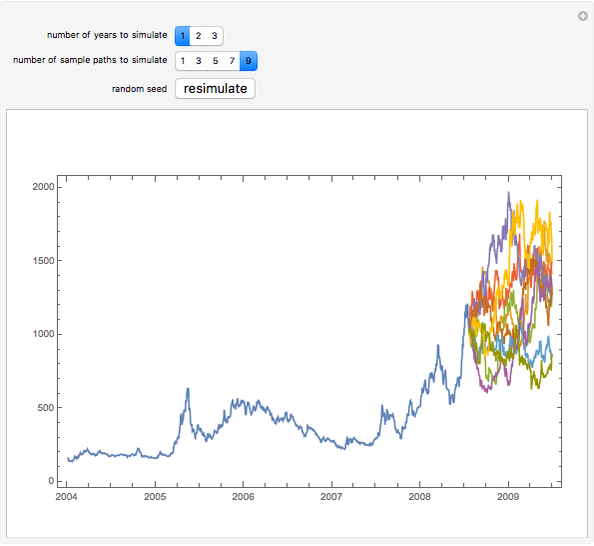

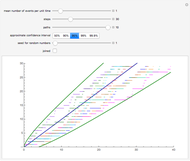

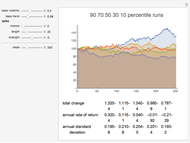

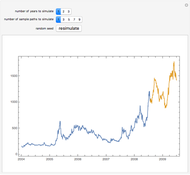

Bootstrapping is a resampling method that has a wide variety of applications. It can be used to simulate the trajectories of sample paths, to determine if an estimator generated from real-world data has an approximate distribution, or to derive standard errors of a complicated estimator.

[more]

Contributed by: Jeff Hamrick (August 2008)

Open content licensed under CC BY-NC-SA

Snapshots

Details

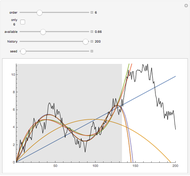

We assume that the log-returns of the credit default swap (CDS) index are independent and identically distributed. After computing the set of log-returns in the automobile and automobile parts CDS index for the period from January 1, 2004 through July 21, 2008, we resample from the empirical distribution to obtain projected log-returns for the index for a length of time specified by the user. We then reconstitute the future projected index using the latest observed value of the index.

A credit default swap (CDS) is a bilateral contract, typically possessing counter-party risk, under which two parties agree to isolate and trade the credit risk of at least one third-party reference entity. The buyer of the swap receives credit protection and pays a premium periodically to the seller of the swap. If a "credit event'' occurs (typically failure to make a coupon or principal payment, but also possibly failing to maintain certain financial ratios), then the seller of the swap is obligated to purchase the bond from the swap buyer at par value. Credit default swaps can also be settled in the cash market; after a credit event occurs, the seller can simply pay the buyer the difference between the new (typically much lower) price of the bond and the par value of the bond.

Datastream, a popular data service owned by Thomson Financial, produces a family of credit default swap indices. Some of these indices are organized by U.S. economic sectors. Moreover, they are effectively market-weighted (by the market weights of the underlying bond instruments) averages of relatively liquid credit default swaps. The sector-based credit default swap indices produced by Datastream include automobile and related parts, banks, basic resources, chemicals, construction and materials, financial services, food and beverages, health care, industrial goods and services, insurance, media, oil and gas, personal and household goods, real estate, retail, technology, telecommunications, travel and leisure, and utilities. Various credit default swap indices for various economic sectors are available for the United States, Japan, the United Kingdom, and Europe. We study the automobile and related parts CDS index.

We note that the technique of bootstrapping future trajectories of economic variables (like asset prices or credit default swap data) is not immune to criticism. It is potentially problematic to rely on the assumption that some aspects of the time series (in our case, the log-returns) are independent and identically distributed. In particular, one can argue that in the current credit crisis, credit default swap premiums are extraordinarily high, and that they will "revert to the mean" in the near-term. Most of the projections we make result in a credit default swap index that remains rather high for the foreseeable future.

Permanent Citation

"Bootstrapping Credit Default Swap Data"

http://demonstrations.wolfram.com/BootstrappingCreditDefaultSwapData/

Wolfram Demonstrations Project

Published: August 27 2008

Bootstrapping to Compute Value-at-Risk Standard Errors

Bootstrapping to Compute Value-at-Risk Standard Errors

Jeff Hamrick World Bank Data Series Overview

World Bank Data Series Overview

Michael Schreiber Polynomial Fits of Random Walks

Polynomial Fits of Random Walks

Michael Schreiber Expected Returns of the Dow Industrials, Fama-French Model

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick and Jason Cawley Analysis of Minimum Credit Card Payments

Analysis of Minimum Credit Card Payments

Andreas Lauschke Stock Forecasting

Stock Forecasting

Andrew Tao Simulating the Poisson Process

Simulating the Poisson Process

Heikki Ruskeepää Markov Volatility Random Walks

Markov Volatility Random Walks

Jason Cawley Holistic Theorem

Holistic Theorem

Phil Kongtcheu Expected Returns of the Dow Industrials, Beta Model

Expected Returns of the Dow Industrials, Beta Model

Jeff Hamrick and Jason Cawley

-

Expected Returns of the Dow Industrials, Beta Model

Jeff Hamrick -

Exploring Measures of Association

Exploring Measures of Association

Jeff Hamrick -

Bootstrapping Credit Default Swap Data

Bootstrapping Credit Default Swap Data

Jeff Hamrick -

Linear Dependence between Two Bernoulli Random Variables

Linear Dependence between Two Bernoulli Random Variables

Jeff Hamrick -

Estimating the Local Mean Function

Estimating the Local Mean Function

Jeff Hamrick -

Acceptance/Rejection Sampling

Acceptance/Rejection Sampling

Jeff Hamrick -

Simulating the 2008 U.S. Presidential Election

Simulating the 2008 U.S. Presidential Election

Jeff Hamrick -

The Method of Inverse Transforms

The Method of Inverse Transforms

Jeff Hamrick -

The Perturbed Rat

The Perturbed Rat

Jeff Hamrick -

Modeling Return Distributions

Modeling Return Distributions

Jeff Hamrick -

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Jeff Hamrick -

The Method of Common Random Numbers: An Example

The Method of Common Random Numbers: An Example

Jeff Hamrick -

The Envelope Theorem: Numerical Examples

The Envelope Theorem: Numerical Examples

Jeff Hamrick -

Bootstrapping to Compute Value-at-Risk Standard Errors

Jeff Hamrick -

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick -

Kernel Density Estimation

Kernel Density Estimation

Jeff Hamrick -

Simulating Asset Prices with a GARCH(1,1) Model

Simulating Asset Prices with a GARCH(1,1) Model

Jeff Hamrick