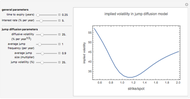

Implied Volatility in Merton's Jump Diffusion Model

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

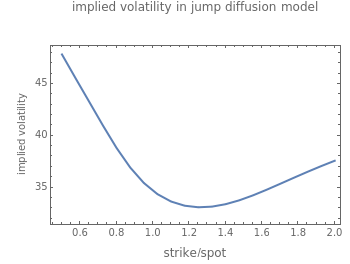

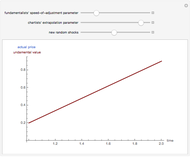

The "implied volatility" corresponding to an option price is the value of the volatility parameter for which the Black-Scholes model gives the same price. A well-known phenomenon in market option prices is the "volatility smile", in which the implied volatility increases for strike values away from the spot price. The jump diffusion model is a generalization of Black–Scholes in which the stock price has randomly occurring jumps in addition to the random walk behavior. One of the interesting properties of this model is that it displays the volatility smile effect. In this Demonstration, we explore the Black–Scholes implied volatility of option prices (equal for both put and call options) in the jump diffusion model. The implied volatility is modeled as a function of the ratio of option strike price to spot price.

Contributed by: Peter Falloon (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

In the jump diffusion model, the stock price  follows the random process

follows the random process  , which comprises, in order, drift, diffusive, and jump components. The jumps occur according to a Poisson distribution and their size follows a log-normal distribution. The model is characterized by the diffusive volatility

, which comprises, in order, drift, diffusive, and jump components. The jumps occur according to a Poisson distribution and their size follows a log-normal distribution. The model is characterized by the diffusive volatility  , the average jump size

, the average jump size  (expressed as a fraction of ), the frequency of jumps

(expressed as a fraction of ), the frequency of jumps  , and the volatility of jump size

, and the volatility of jump size  .

.

In this Demonstration, you can vary the model parameters, along with the time to option expiry and the (constant) interest rate.

Note that, in addition to varying with the model parameters and strike/spot price ratio, the implied volatility is generally larger than the model diffusive volatility ; this is essentially the extra volatility introduced by the jumps.

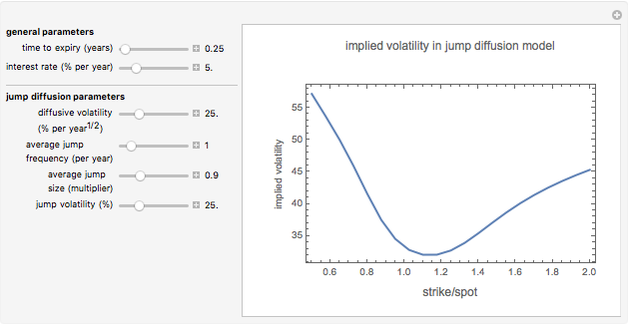

Snapshot 1: volatility smile in a jump diffusion model with downward jumps ( )

)

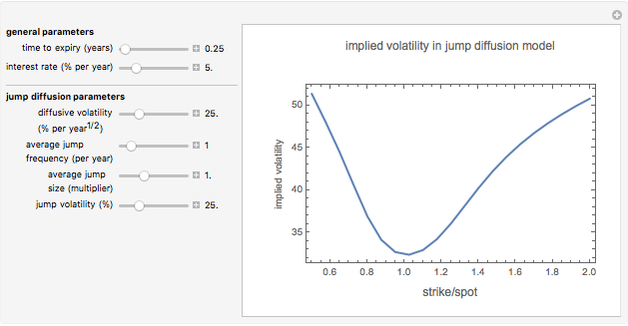

Snapshot 2: volatility smile with symmetric jumps ( )

)

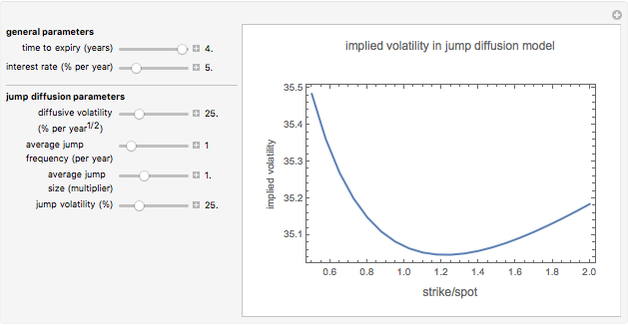

Snapshot 3: for long-dated options (here, time to expiry is four years) the smile is less pronounced

References:

R. Merton, Continuous‐Time Finance, Oxford: Blackwell, 1998.

M. Joshi, The Concepts and Practice of Mathematical Finance, Cambridge: Cambridge University Press, 2003.

Permanent Citation

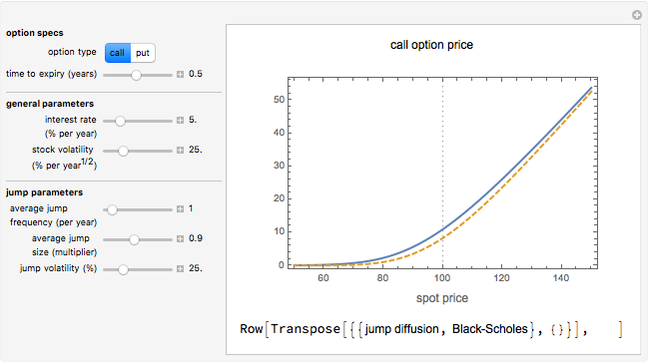

Option Prices in Merton's Jump Diffusion Model

Option Prices in Merton's Jump Diffusion Model

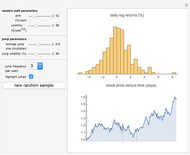

Peter Falloon Distribution of Returns from Merton's Jump Diffusion Model

Distribution of Returns from Merton's Jump Diffusion Model

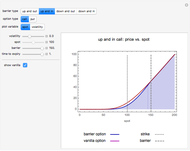

Peter Falloon Barrier Option Pricing within the Black-Scholes Model

Barrier Option Pricing within the Black-Scholes Model

Peter Falloon Pricing Power Options in the Black-Scholes Model

Pricing Power Options in the Black-Scholes Model

Peter Falloon Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski Markov Volatility Random Walks

Markov Volatility Random Walks

Jason Cawley Options Board Using Black-Scholes Prices

Options Board Using Black-Scholes Prices

Peter Falloon Bubbles in a Simple Behavioral Finance Model

Bubbles in a Simple Behavioral Finance Model

Kevin W. Capehart Chooser Options

Chooser Options

Peter Falloon Basic Option Trading Strategies

Basic Option Trading Strategies

Peter Falloon

-

Option Prices in Merton's Jump Diffusion Model

Peter Falloon -

Chooser Options

Peter Falloon -

Binary Options: Pricing and Greeks

Binary Options: Pricing and Greeks

Peter Falloon -

Angular Spheroidal Functions as a Function of Spheroidicity

Angular Spheroidal Functions as a Function of Spheroidicity

Peter Falloon -

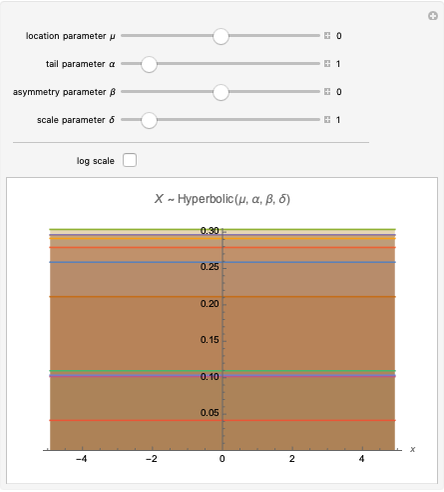

Hyperbolic Distribution

Hyperbolic Distribution

Peter Falloon -

Variance-Gamma Distribution

Variance-Gamma Distribution

Peter Falloon -

Options Board Using Black-Scholes Prices

Peter Falloon -

Properties of a Simple Random Walk with Boundaries

Properties of a Simple Random Walk with Boundaries

Peter Falloon -

Visualizing Superellipses

Visualizing Superellipses

Peter Falloon -

Haar Functions

Haar Functions

Peter Falloon -

Barrier Option Pricing within the Black-Scholes Model

Peter Falloon -

Clebsch-Gordan Coefficients

Clebsch-Gordan Coefficients

Peter Falloon -

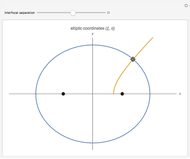

Constant Coordinate Curves for Elliptic Coordinates

Constant Coordinate Curves for Elliptic Coordinates

Peter Falloon -

Chi-Squared Distribution and the Central Limit Theorem

Chi-Squared Distribution and the Central Limit Theorem

Peter Falloon -

Multiple Slit Diffraction Pattern

Multiple Slit Diffraction Pattern

Peter Falloon -

Constant Coordinate Curves for Parabolic and Polar Coordinates

Constant Coordinate Curves for Parabolic and Polar Coordinates

Peter Falloon -

Distribution of Returns from Merton's Jump Diffusion Model

Peter Falloon -

Pricing Power Options in the Black-Scholes Model

Peter Falloon -

Implied Volatility in Merton's Jump Diffusion Model

Implied Volatility in Merton's Jump Diffusion Model

Peter Falloon -

Game Clock

Game Clock

Peter Falloon