Distribution of Returns from Merton's Jump Diffusion Model

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

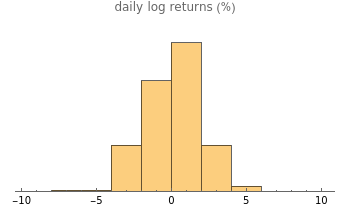

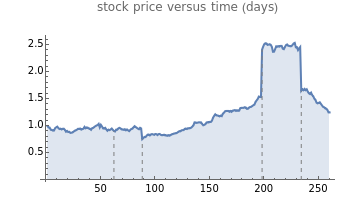

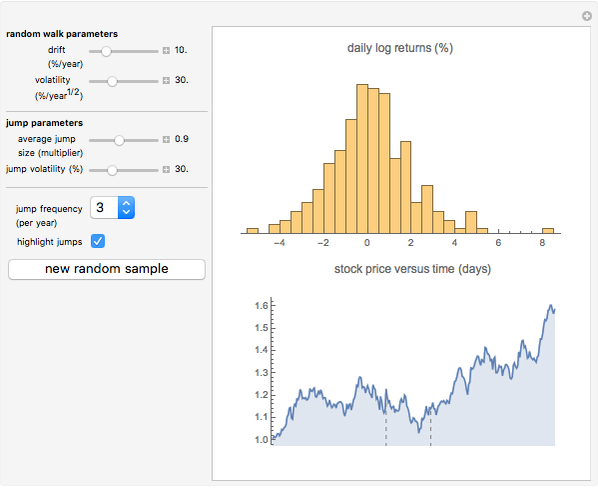

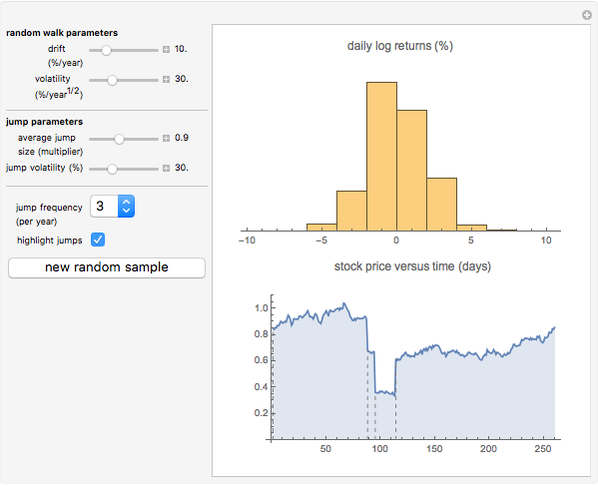

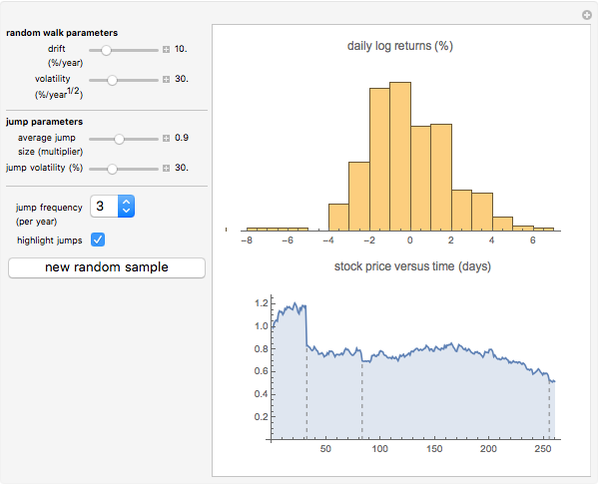

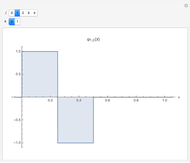

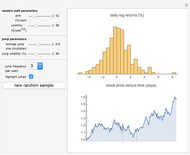

This Demonstration illustrates sample paths for an asset following Merton's jump diffusion model: the upper graph is a histogram of daily price returns, while the lower graph is the time series of price, both for a sample path of one year. The key feature of this model is that it incorporates large jumps; these show up as outliers in the histogram. The model parameters (namely, drift and volatility of the diffusive component, together with average size and volatility of the jumps) can be varied for a given sample. New random samples can be drawn, and the jump frequency (i.e., average number of jumps per sample) can be varied.

Contributed by: Peter Falloon (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

In the jump diffusion model, the stock price  follows the random process

follows the random process  . The first two terms are familiar from the Black–Scholes model: drift rate

. The first two terms are familiar from the Black–Scholes model: drift rate  , volatility

, volatility  , and random walk (Wiener process)

, and random walk (Wiener process)  . The last term represents the jumps:

. The last term represents the jumps:  is the jump size as a multiple of stock price, while

is the jump size as a multiple of stock price, while  is the number of jump events that have occurred up to time

is the number of jump events that have occurred up to time  .

.  is assumed to follow the Poisson process

is assumed to follow the Poisson process  , where

, where  is the average frequency with which jumps occur. The jump size follows a log-normal distribution

is the average frequency with which jumps occur. The jump size follows a log-normal distribution  , where

, where  is the standard normal distribution,

is the standard normal distribution,  is the average jump size, and

is the average jump size, and  is the volatility of jump size.

is the volatility of jump size.

Snapshot 1: when there are no jumps, the jump diffusion model reduces to the Black–Scholes model, in which returns follow a normal distribution

Snapshot 2: the effect of jumps can be observed clearly by "turning down" the volatility of the diffusive component to zero

Snapshot 3: one limitation of the jump diffusion model is that is the volatility in the diffusive component is constant, which results in unrealistic-looking behavior when the jumps are large: in reality, volatility tends to increase dramatically around the time that large jumps occur.

References:

R. Merton, Continuous-Time Finance, Cambridge, MA: B. Blackwell, 1998.

M. Joshi, The Concepts and Practice of Mathematical Finance, New York: Cambridge University Press, 2003.

Permanent Citation

"Distribution of Returns from Merton's Jump Diffusion Model"

http://demonstrations.wolfram.com/DistributionOfReturnsFromMertonsJumpDiffusionModel/

Wolfram Demonstrations Project

Published: March 7 2011

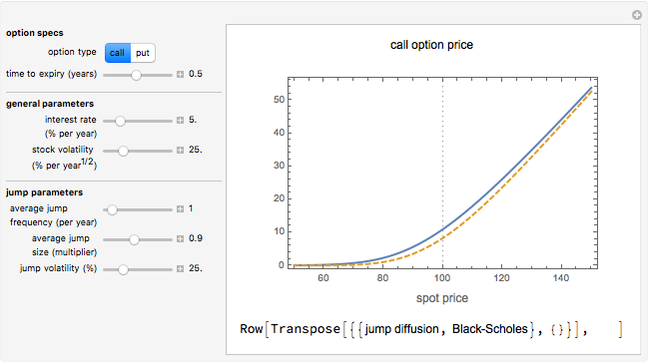

Option Prices in Merton's Jump Diffusion Model

Option Prices in Merton's Jump Diffusion Model

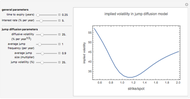

Peter Falloon Implied Volatility in Merton's Jump Diffusion Model

Implied Volatility in Merton's Jump Diffusion Model

Peter Falloon Barrier Option Pricing within the Black-Scholes Model

Barrier Option Pricing within the Black-Scholes Model

Peter Falloon Pricing Power Options in the Black-Scholes Model

Pricing Power Options in the Black-Scholes Model

Peter Falloon Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski Stock Market Returns by Party

Stock Market Returns by Party

Theodore Gray Options Board Using Black-Scholes Prices

Options Board Using Black-Scholes Prices

Peter Falloon Chooser Options

Chooser Options

Peter Falloon Basic Option Trading Strategies

Basic Option Trading Strategies

Peter Falloon Options: Time Value

Options: Time Value

Peter Falloon

-

Option Prices in Merton's Jump Diffusion Model

Peter Falloon -

Chooser Options

Peter Falloon -

Binary Options: Pricing and Greeks

Binary Options: Pricing and Greeks

Peter Falloon -

Angular Spheroidal Functions as a Function of Spheroidicity

Angular Spheroidal Functions as a Function of Spheroidicity

Peter Falloon -

Hyperbolic Distribution

Hyperbolic Distribution

Peter Falloon -

Variance-Gamma Distribution

Variance-Gamma Distribution

Peter Falloon -

Options Board Using Black-Scholes Prices

Peter Falloon -

Properties of a Simple Random Walk with Boundaries

Properties of a Simple Random Walk with Boundaries

Peter Falloon -

Visualizing Superellipses

Visualizing Superellipses

Peter Falloon -

Haar Functions

Haar Functions

Peter Falloon -

Barrier Option Pricing within the Black-Scholes Model

Peter Falloon -

Clebsch-Gordan Coefficients

Clebsch-Gordan Coefficients

Peter Falloon -

Constant Coordinate Curves for Elliptic Coordinates

Constant Coordinate Curves for Elliptic Coordinates

Peter Falloon -

Chi-Squared Distribution and the Central Limit Theorem

Chi-Squared Distribution and the Central Limit Theorem

Peter Falloon -

Multiple Slit Diffraction Pattern

Multiple Slit Diffraction Pattern

Peter Falloon -

Constant Coordinate Curves for Parabolic and Polar Coordinates

Constant Coordinate Curves for Parabolic and Polar Coordinates

Peter Falloon -

Distribution of Returns from Merton's Jump Diffusion Model

Distribution of Returns from Merton's Jump Diffusion Model

Peter Falloon -

Pricing Power Options in the Black-Scholes Model

Peter Falloon -

Implied Volatility in Merton's Jump Diffusion Model

Peter Falloon -

Game Clock

Game Clock

Peter Falloon