Hedging the Black-Scholes Call Option

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

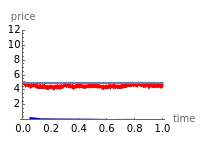

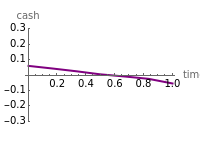

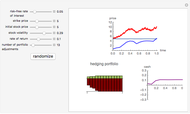

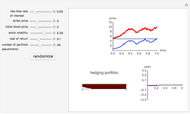

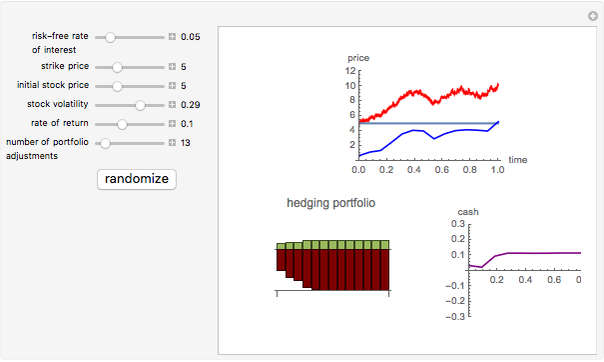

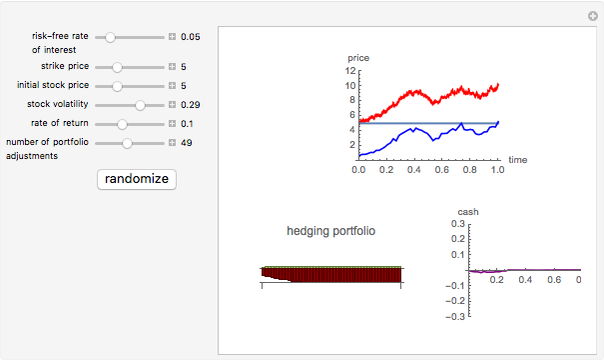

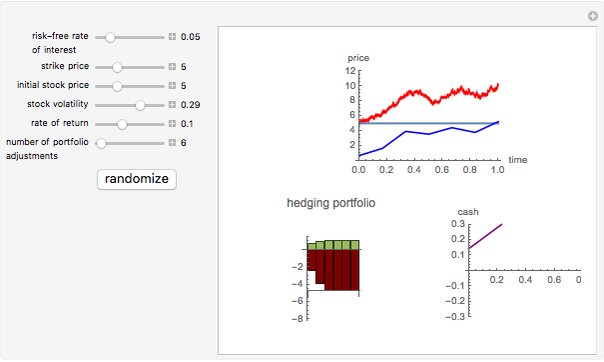

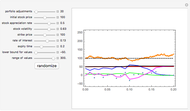

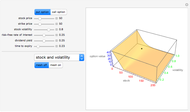

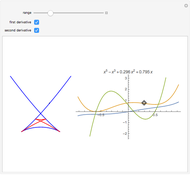

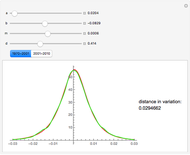

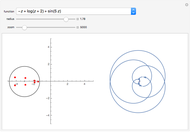

We demonstrate hedging of a vanilla European call option on stock paying no dividend in the Black–Scholes model. The top picture shows the path of an exponential Brownian motion (actually, a random walk approximation with a very small time step) representing the price of stock (colored red), the strike price of a European call option (colored dark blue), and the values of a hedging portfolio. The hedging portfolio itself, consisting of some stock (colored green) and a short position in a riskless bond (colored red) is shown below. The graph at the lower right shows the "cash flow" from the transactions performed in holding the portfolio. For a perfectly self-financing portfolio this graph ought to be perfectly flat and coincide with the horizontal axis.

[more]

Contributed by: Andrzej Kozlowski (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

Hedging is both a theoretical device that makes it possible to calculate the "fair value" of derivative instruments such as options and a practical technique of risk management. Here we illustrate it on one of the simplest examples: a so-called vanilla European call option on stock whose price is assumed to follow an exponential Brownian motion (the Black–Scholes model). We assume the stock pays no dividend and that the rate of interest is constant (neither of these are essential assumptions but they make the details simpler). Since we cannot use a genuine Brownian motion, we approximate it by a random walk consisting of a large number of independent and normally distributed jumps over equally spaced time periods ("steps"). We hold a portfolio consisting of a certain number of shares of stock and a short position in a risk-free bond, which means that the value of the bond is subtracted when computing the value of the portfolio. We purchase a starting portfolio consisting of some stock and a certain quantity of interest-paying bond, which we "short" (financial jargon for selling without owning). We then observe the movements of the stock at a certain number of points in time and adjust the portfolio we hold, by selling the old one and purchasing a new one at each of these points.

The cash flow of these transactions is shown in the picture on the rightâ€Âhand side. The portfolio is almost "self-financing", that is, the proceeds from the transactions almost exactly balance the costs of purchasing new portfolios. To obtain a genuinely self-financing portfolio we would need to adjust the portfolio at every moment in time, which in the case of a genuine continuous exponential Brownian motion is, of course, impossible. However, we can see that increasing the number of portfolio adjustments will tend to make the portfolio closer to a "self-financing" one (the cash flow curve on the lower right will lie closer to the horizontal axis). In practice, one needs a certain amount of cash to finance hedging operations, which, in the real world, also includes transaction costs.

Note that the final payoff from the option, which is equal to the greater of (a) the stock price at expiration minus the strike price and (b) zero, is almost equal to the final value of the hedging portfolio—as it should be. Thus the portfolio really "hedges" the European call option, in the sense that it always produces a payoff (almost) equal to that of the option. It follows that the initial value of the hedging portfolio must be (approximately) equal to the "fair value" of the option.

The entire argument can be viewed as a visual proof of the Black–Scholes formula, which is actually the main tool used in constructing the hedging portfolio.

Permanent Citation

"Hedging the Black-Scholes Call Option"

http://demonstrations.wolfram.com/HedgingTheBlackScholesCallOption/

Wolfram Demonstrations Project

Published: March 7 2011

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski Option Prices under the Fractional Black-Scholes Model

Option Prices under the Fractional Black-Scholes Model

Andrzej Kozlowski Hedging the European Put Option

Hedging the European Put Option

Andrzej Kozlowski The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

Andrzej Kozlowski Exploring the Black-Scholes Formula

Exploring the Black-Scholes Formula

Andrzej Kozlowski American Call and Put Option

American Call and Put Option

Andrzej Kozlowski The Price of a Call Option on Electrical Power

The Price of a Call Option on Electrical Power

Andrzej Kozlowski The Russian Option: Reduced Regret

The Russian Option: Reduced Regret

Andrzej Kozlowski Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

Andrzej Kozlowski

-

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski -

Newton Polygon and Branching of Algebraic Curves

Newton Polygon and Branching of Algebraic Curves

Andrzej Kozlowski -

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Andrzej Kozlowski -

The Space of Inner Products

The Space of Inner Products

Andrzej Kozlowski