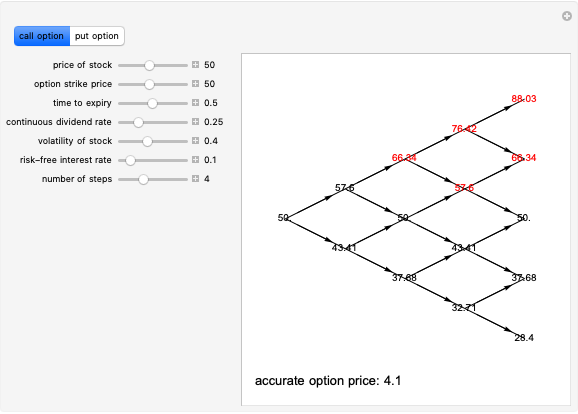

Hedging the European Put Option

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

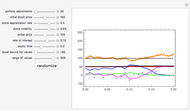

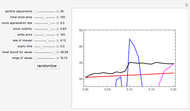

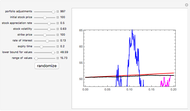

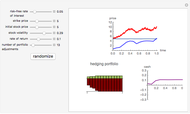

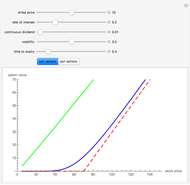

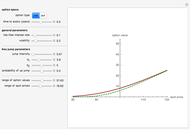

This Demonstration illustrates the so-called delta-hedging argument that is used to derive the Black–Scholes formula for the price of a European put option on stock in the Black–Scholes model. The sample path of a stock price following an exponential Brownian process is shown colored orange (mouse over a curve to display its description). The strike price is represented by the dashed black line. A portfolio is constructed consisting of one put option on the stock, an amount of stock (equal to -Δ, where Δ is the derivative of the Black–Scholes price of the option with respect to the stock price), and a money market account. The portfolio is adjusted at regular intervals (you choose the number of times) and the proceeds from the transactions (shown as points in the graph) are invested in the money market. The total value of the portfolio, which is the sum of the value of the option (green line), value of the stock held (blue line), and the money market account (magenta line) is almost deterministic. Zooming in on this brokerage account line (by using the two bottom sliders) reveals the presence of randomness, which can be eliminated by increasing the number of portfolio adjustments.

Contributed by: Andrzej Kozlowski (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

There are two basic arguments involving delta-hedging that can be used to derive the Black–Scholes formula. One of them is used in the related Demonstration "Hedging the Black-Scholes Call Option". In that argument a self-financing portfolio is constructed that matches with probability 1 the value of the payoff of the option. In practice the portfolio is only approximately self-financing; to make it really so, infinitely many portfolio adjustments are needed. Here we construct a portfolio consisting of the option itself, stock, and a money market account, which makes the portfolio self-financing. However, again, infinitely many portfolio adjustments are needed to make the portfolio truly self-financing and "riskless". Assuming that the portfolio is self-financing and riskless, the principle of absence of arbitrage implies that it has to grow at the riskless interest rate. Writing this condition in differential form and using the Itô formula leads to the Black–Scholes equation.

This argument is given in incorrect form in many well-known books on option pricing—it ignores the money market account and incorrectly applies the Itô formula. This particular corrected version of the argument can be found in S. Stojanovic, Computational Financial Mathematics Using Mathematica, Boston: Birkhäuser, 2002, which also contains a Mathematica program implementing it (somewhat different from this Demonstration and written for an earlier version of Mathematica).

Permanent Citation

"Hedging the European Put Option"

http://demonstrations.wolfram.com/HedgingTheEuropeanPutOption/

Wolfram Demonstrations Project

Published: March 7 2011

Hedging the Black-Scholes Call Option

Hedging the Black-Scholes Call Option

Andrzej Kozlowski American Call and Put Option

American Call and Put Option

Andrzej Kozlowski Standard American and European Options

Standard American and European Options

Andrzej Kozlowski The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

Andrzej Kozlowski The Russian Option: Reduced Regret

The Russian Option: Reduced Regret

Andrzej Kozlowski Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski Option Prices under the Fractional Black-Scholes Model

Option Prices under the Fractional Black-Scholes Model

Andrzej Kozlowski The Price of a Call Option on Electrical Power

The Price of a Call Option on Electrical Power

Andrzej Kozlowski Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

Andrzej Kozlowski

-

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski -

Newton Polygon and Branching of Algebraic Curves

Newton Polygon and Branching of Algebraic Curves

Andrzej Kozlowski -

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Andrzej Kozlowski -

The Space of Inner Products

The Space of Inner Products

Andrzej Kozlowski