Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

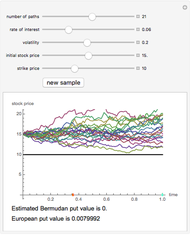

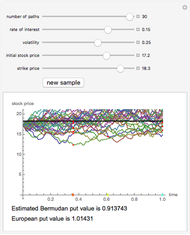

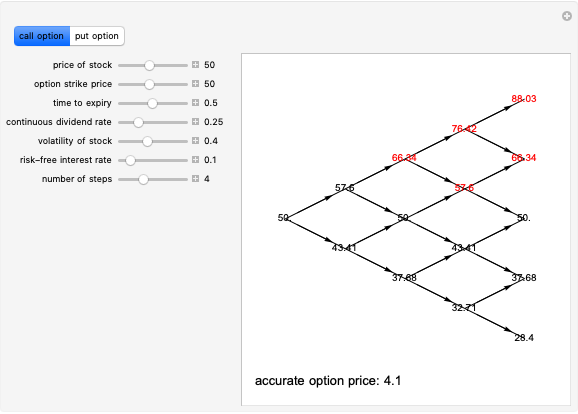

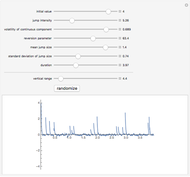

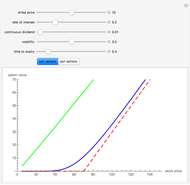

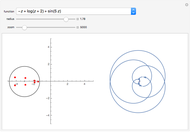

A Bermudan put option on a stock gives its holder the right to sell the stock at an agreed strike price at a certain finite number of fixed times before or at the final expiry time. Thus a Bermudan put option is more valuable than a European option (with the same parameters) but less valuable than an American put option, which can be exercised at any time before expiry. This Demonstration implements the famous method due to Longstaff and Schwartz of computing the price of a Bermudan put option on a stock by Monte Carlo simulation. Although the method can be applied to any model of stock movement, here we use it in the case of the classical Black–Scholes model. For simplicity, we also assume that the stock pays no dividend.

[more]

Contributed by: Andrzej Kozlowski (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

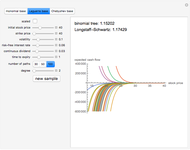

For a long time it used to be believed that the Monte Carlo method is not suitable for pricing the American type of option (one can still find this claim repeated in older texts on mathematical finance). The principle lay in efficiently estimating conditional expectations. The crucial idea, of using least-squares regression on a finite set of functions, was implemented by F. A. Longstaff and E. S. Schwartz (having been earlier proposed by J. Carrière). In this Demonstration we implement the Longstaff and Schwartz algorithm for the standard Bermudan put and call options in the Black–Scholes model. An American option can be treated as a limit of Bermudan options, so by computing the value of a Bermudan option with a large number of exercise times one can obtain a good approximation to the value of the American option.

The number of sample paths used in this Demonstration is too small to expect an accurate value. As a rough measure of accuracy obtained from a particular sample, the value of the corresponding European option, computed by means of the Black–Scholes formula, is displayed below the estimated value of the Bermudan option.

Note that if we place all the exercise times at the expiry time, the Bermudan option will turn into a standard European one, whose value is given by the Black–Scholes formula. This suggests the following method of pricing Bermudan options, which ought to produce reasonably accurate answers even with a small number of sample paths. First place all the exercise points at the expiry time and generate successive samples until the estimate is close to the value given by the Black–Scholes formula. Once that happens, move the exercise times to desired locations.

J. Carrière, "Valuation of Early-Exercise Price of Options Using Simulations and Nonparametric Regression," Insurance: Math. Econ., 19, pp. 19–30 1988.

F. A. Longstaff and E. S. Schwartz, "Valuing American Options by Simulation: A Simple Least-Squares Approach," Review of Financial Studies, 14(1), pp. 113–147 2001.

Robustness of the Longstaff-Schwartz LSM Method of Pricing American Derivatives

Robustness of the Longstaff-Schwartz LSM Method of Pricing American Derivatives

Andrzej Kozlowski Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski The Price of a Call Option on Electrical Power

The Price of a Call Option on Electrical Power

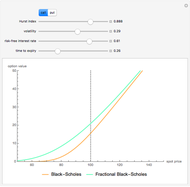

Andrzej Kozlowski Option Prices under the Fractional Black-Scholes Model

Option Prices under the Fractional Black-Scholes Model

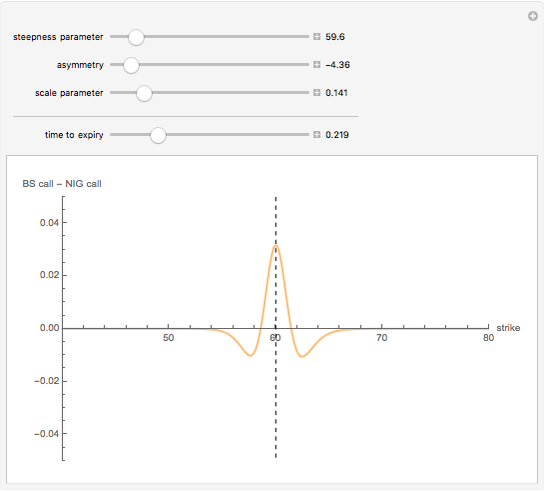

Andrzej Kozlowski The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

Andrzej Kozlowski Hedging the European Put Option

Hedging the European Put Option

Andrzej Kozlowski American Call and Put Option

American Call and Put Option

Andrzej Kozlowski The Russian Option: Reduced Regret

The Russian Option: Reduced Regret

Andrzej Kozlowski Hedging the Black-Scholes Call Option

Hedging the Black-Scholes Call Option

Andrzej Kozlowski The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski

-

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski -

Newton Polygon and Branching of Algebraic Curves

Newton Polygon and Branching of Algebraic Curves

Andrzej Kozlowski -

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Andrzej Kozlowski -

The Space of Inner Products

The Space of Inner Products

Andrzej Kozlowski