The Price of a Call Option on Electrical Power

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

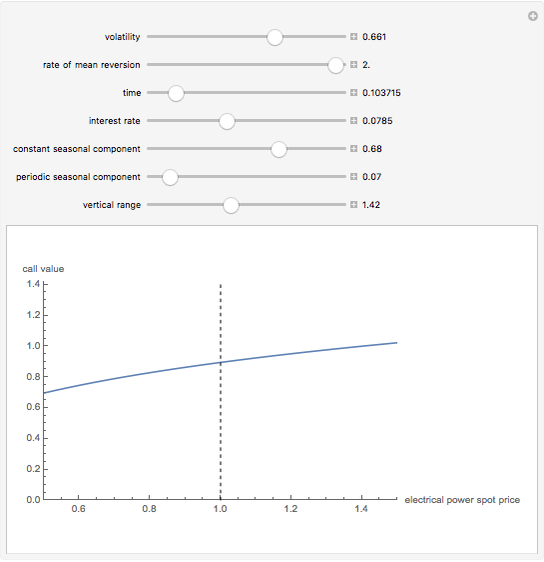

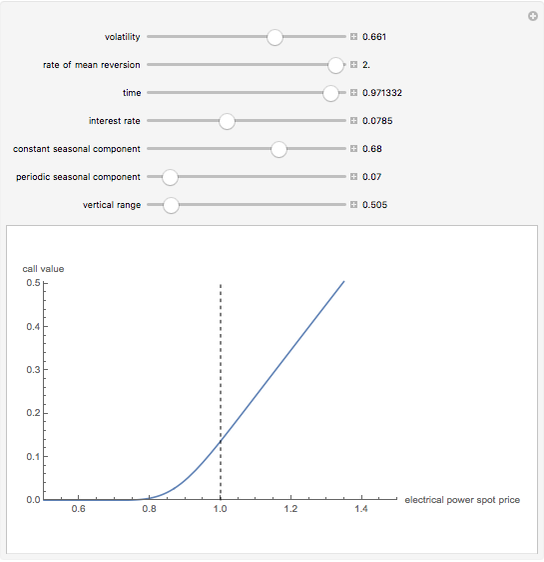

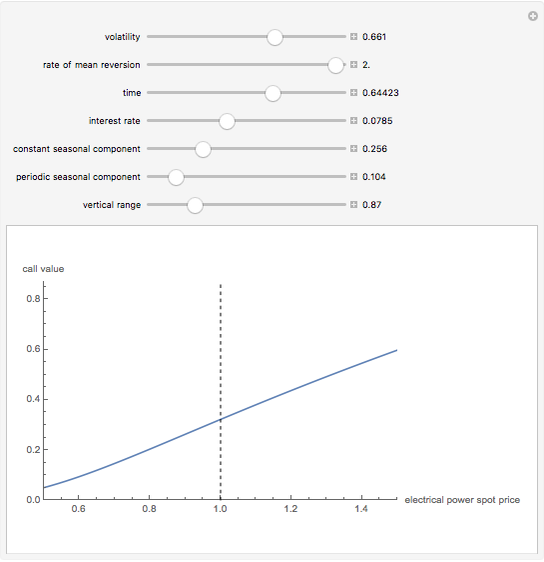

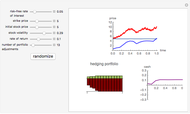

We demonstrate the formula for the value of a call option on electrical power obtained by Tino Kluge, which is analogous to the classical Black–Scholes formula. The model of spot price movements is described under a risk-neutral measure by  , where

, where  is a mean-reverting process satisfying

is a mean-reverting process satisfying  , and

, and  is Brownian motion. The deterministic seasonality function

is Brownian motion. The deterministic seasonality function  is supposed to capture all relevant components of the market that vary predictably with time. Here we use an oversimplified model,

is supposed to capture all relevant components of the market that vary predictably with time. Here we use an oversimplified model,  , where the trigonometric component reflects weekly periodicity (time

, where the trigonometric component reflects weekly periodicity (time  is measured in years, with 365 days per year and 7 days per week).

is measured in years, with 365 days per year and 7 days per week).

Contributed by: Andrzej Kozlowski (March 2011)

Open content licensed under CC BY-NC-SA

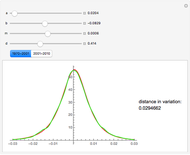

Snapshots

Details

In many markets in various parts of the world deregulation of electric power has led to more competitive prices, but at the same time to higher uncertainty about future development. This in turn led to the introduction of derivative contracts such as options, intended to protect energy users from unexpected price spikes due to various seasonal and random factors. Models borrowed from financial markets, such as the Black–Scholes model, are not suitable for valuing options on electrical energy, as they lack the most important property such a model should have: mean reversion. The price of electrical energy (and other commodities) reflects the marginal cost of production and departs from this value due to various random and seasonal factors. When the influence of these temporary factors ceases, the price tends to revert to the mean. There is one additional important aspect of electricity prices: discontinuous random spikes in price due to unpredictable changes in weather or supply conditions. We ignore this aspect in this Demonstration for the sake of simplicity and particularly because we can then use a closed-form solution analogous to the one for Black–Scholes, given in [1] (where a much more sophisticated model, including spikes, is studied). The model used in here is a simplified version of Model 2 of [2], with the deterministic seasonal component reflecting only weekly seasonality and the difference between holidays and "peak" days disregarded.

[1] T. Kluge, Pricing Swing Options And Other Electricity Derivatives, Univ. Of Oxford D. Phil. thesis, 2006.

[2] J. Lucia and E. Schwartz, "Electricity Prices and Power Derivatives: Evidence from the Nordic Power Exchange," Review of Derivatives Research, 5(1), 2002 pp. 5–50.

Permanent Citation

"The Price of a Call Option on Electrical Power"

http://demonstrations.wolfram.com/ThePriceOfACallOptionOnElectricalPower/

Wolfram Demonstrations Project

Published: March 7 2011

American Call and Put Option

American Call and Put Option

Andrzej Kozlowski Hedging the Black-Scholes Call Option

Hedging the Black-Scholes Call Option

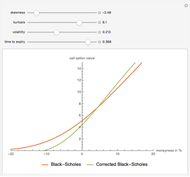

Andrzej Kozlowski The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

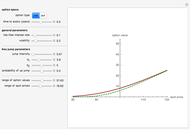

Andrzej Kozlowski Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

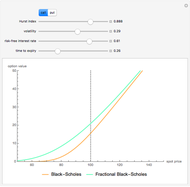

Andrzej Kozlowski Option Prices under the Fractional Black-Scholes Model

Option Prices under the Fractional Black-Scholes Model

Andrzej Kozlowski Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

Andrzej Kozlowski The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

Andrzej Kozlowski Hedging the European Put Option

Hedging the European Put Option

Andrzej Kozlowski The Russian Option: Reduced Regret

The Russian Option: Reduced Regret

Andrzej Kozlowski Standard American and European Options

Standard American and European Options

Andrzej Kozlowski

-

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski -

Newton Polygon and Branching of Algebraic Curves

Newton Polygon and Branching of Algebraic Curves

Andrzej Kozlowski -

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Andrzej Kozlowski -

The Space of Inner Products

The Space of Inner Products

Andrzej Kozlowski