Spectral Measures

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

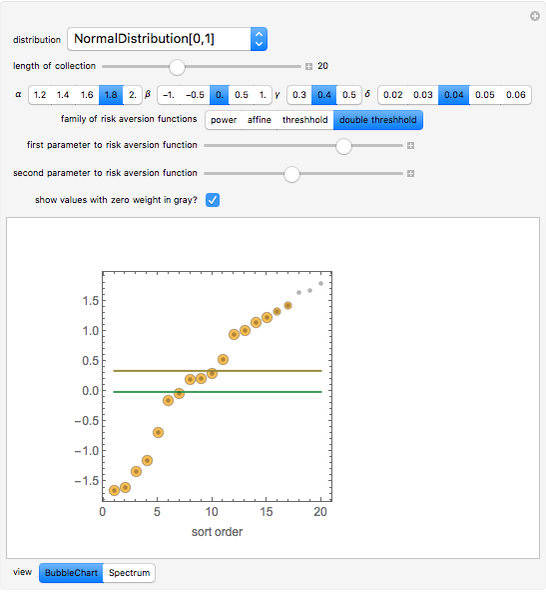

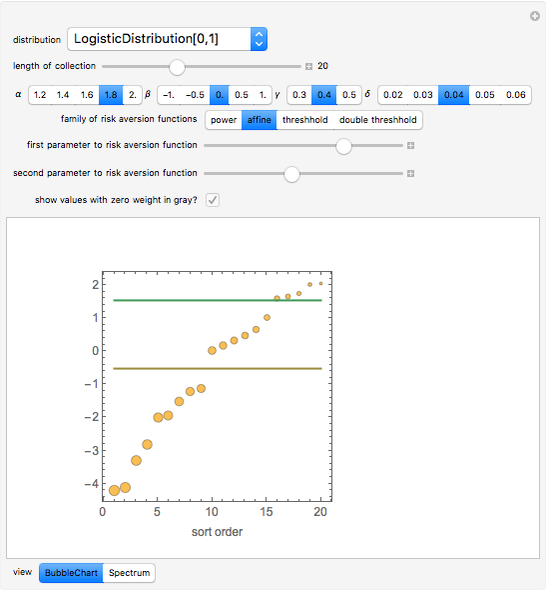

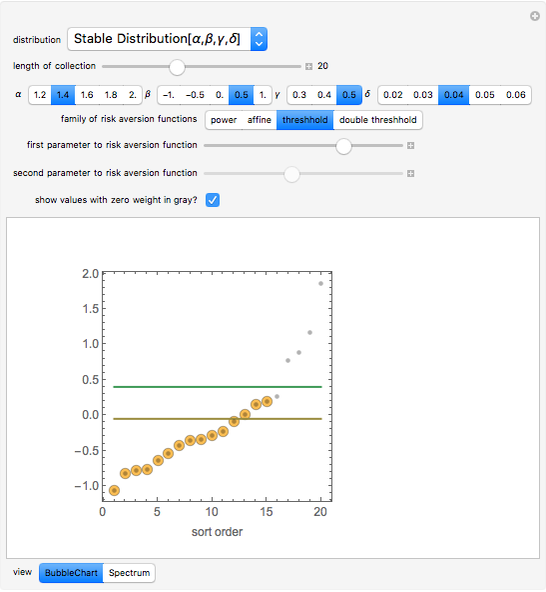

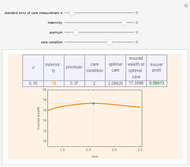

Analyses of investments, insurance, and economic policies often depend on an ability to collapse a large set of probability-weighted outcomes to just a few numbers. Examples of this process are computations of "expected utility", (or its cousin, "certainty equivalent wealth"), means and standard deviations of the outcomes, and "value at risk". Each of these measures has strengths as well as deficiencies, the latter including frequent difficulty in coping with negative outcomes in expected utility theory, the theoretical nonexistence of standard deviations for outcomes drawn from certain distributions, and the lack of sensitivity of value at risk to the magnitude of the worst outcomes.

[more]

Contributed by: Seth J. Chandler and Roger J. Brown (October 2010)

Open content licensed under CC BY-NC-SA

Snapshots

Details

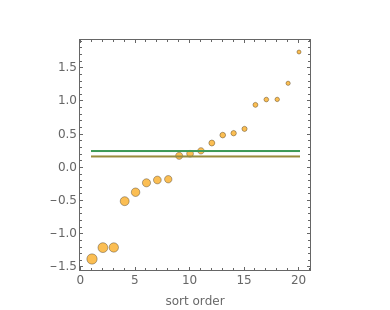

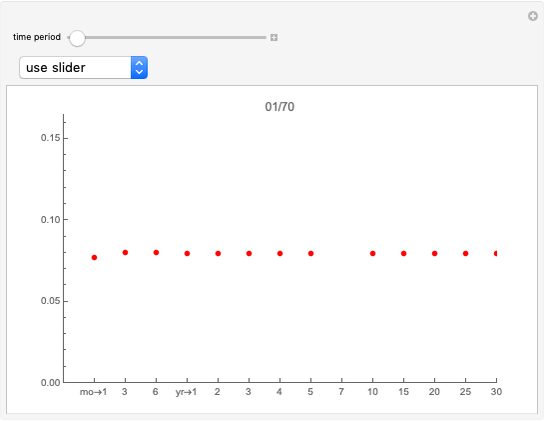

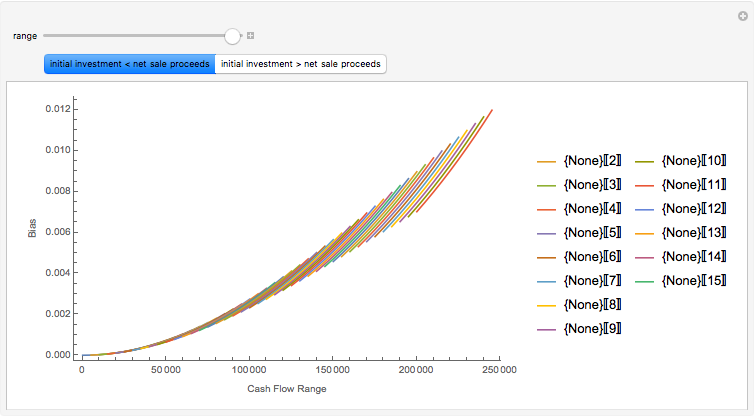

The "threshold" family of spectra has only two values: a constant value up to some position in the spectrum and zero thereafter. The risk measure "expected shortfall", which is growing in popularity and is also known as "conditional value at risk (cvar)", can be generated using a member from this family.

Pioneering work by Carlo Acerbi has been done in the field. A brief discussion of spectral measures may be found at Spectral risk measure.

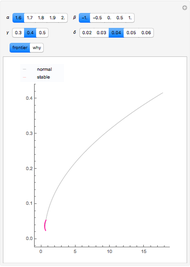

The set of permissible spectral weights is the set of nonincreasing probability density functions (sometimes also known as probability mass functions for discrete distributions).

Permanent Citation

Estimating Insurance Premiums Using Exceedance Data and the Method of Moments

Estimating Insurance Premiums Using Exceedance Data and the Method of Moments

Seth J. Chandler Estimating Loss Functions Using Exceedance Data and the Method of Moments

Estimating Loss Functions Using Exceedance Data and the Method of Moments

Seth J. Chandler Sensitivity, Specificity, and Incidence

Sensitivity, Specificity, and Incidence

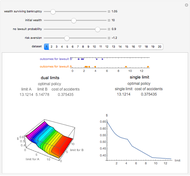

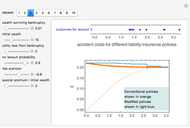

Seth J. Chandler The Efficient Dual-Limit Liability Insurance Contract

The Efficient Dual-Limit Liability Insurance Contract

Seth J. Chandler Property Coinsurance

Property Coinsurance

Seth J. Chandler Efficient Single Limit Liability Insurance

Efficient Single Limit Liability Insurance

Seth J. Chandler Insurance Disclosures

Insurance Disclosures

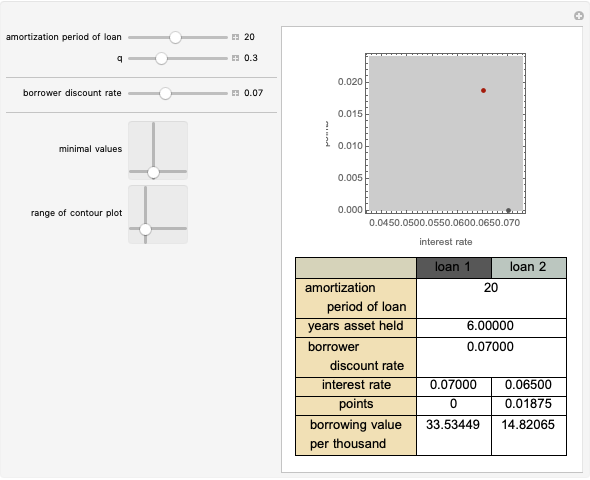

Seth J. Chandler Pay the Points?

Pay the Points?

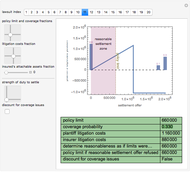

Seth J. Chandler The Duty to Settle

The Duty to Settle

Seth J. Chandler Moral Hazard

Moral Hazard

Seth J. Chandler

-

Dissolving Partnerships

Dissolving Partnerships

Roger J. Brown -

Forming the Efficient Frontier When Returns Are Non-Normal

Forming the Efficient Frontier When Returns Are Non-Normal

Roger J. Brown -

Spectral Measures

Spectral Measures

Roger J. Brown -

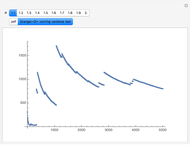

Granger-Orr Running Variance Test

Granger-Orr Running Variance Test

Roger J. Brown -

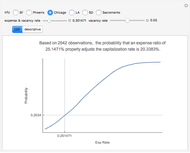

Capitalization Rate Probability

Capitalization Rate Probability

Roger J. Brown -

Net Lease Economics

Net Lease Economics

Roger J. Brown -

The Refinance Decision

The Refinance Decision

Roger J. Brown -

True Cost of Variable Rate Mortgage Funds

True Cost of Variable Rate Mortgage Funds

Roger J. Brown -

Term Structure of Interest Rates

Term Structure of Interest Rates

Roger J. Brown -

Generalized Central Limit Theorem

Generalized Central Limit Theorem

Roger J. Brown -

Inflation-Adjusted Yield

Inflation-Adjusted Yield

Roger J. Brown -

Simulating the IRR

Simulating the IRR

Roger J. Brown -

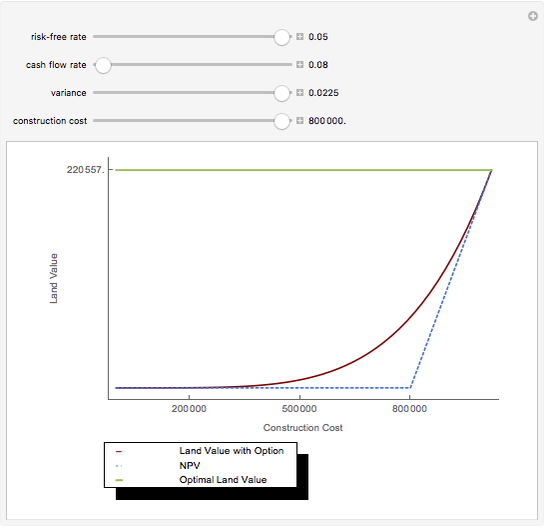

Real Options

Real Options

Roger J. Brown -

The Price-Terms Tradeoff

The Price-Terms Tradeoff

Roger J. Brown -

Fitting an Elephant

Fitting an Elephant

Roger J. Brown -

Solving the Subprime Loan Problem

Solving the Subprime Loan Problem

Roger J. Brown -

Why Location Matters: The Bid Rent Curve

Why Location Matters: The Bid Rent Curve

Roger J. Brown -

Explaining Real Estate Price Bubbles

Explaining Real Estate Price Bubbles

Roger J. Brown -

Value Added Growth Model

Value Added Growth Model

Roger J. Brown -

Connecting the CDF and the PDF

Connecting the CDF and the PDF

Roger J. Brown