Hold-or-Exercise for an American Put Option

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

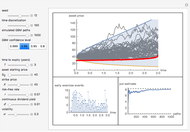

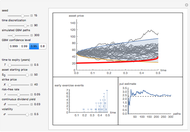

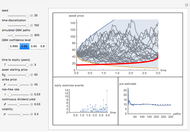

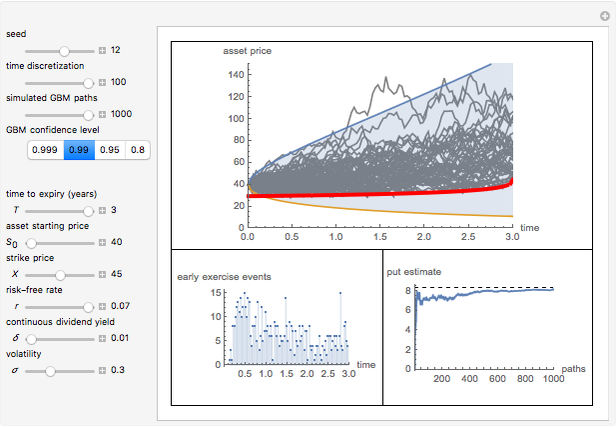

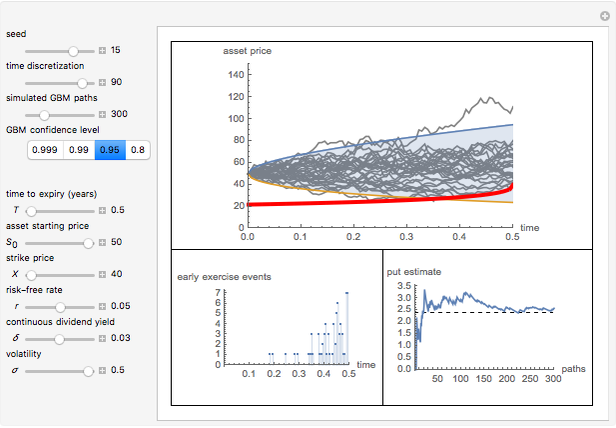

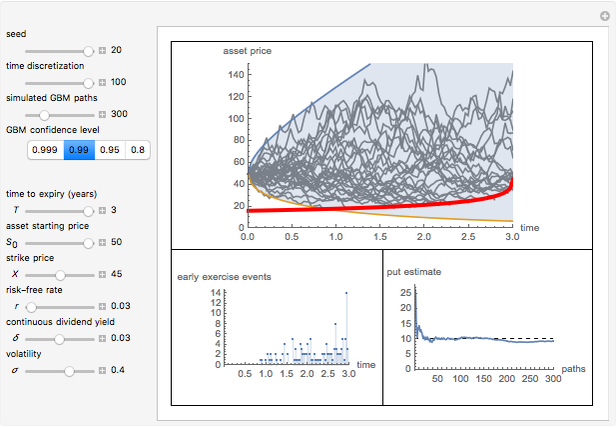

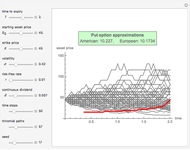

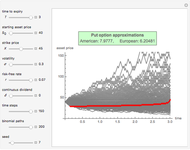

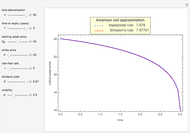

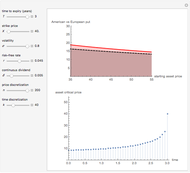

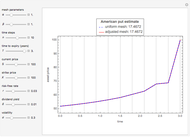

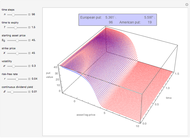

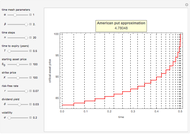

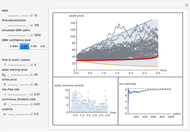

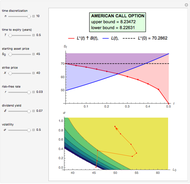

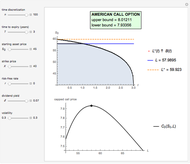

This Demonstration shows the "hold-or-exercise" process during the life of an American put option. The early exercise boundary is constructed according to the quadratic approximation analytical method [1]. Pseudorandom geometric Brownian motion (GBM) paths simulate the asset price through time; whenever a path touches the boundary (dashed red line in the upper graph), the option is instantly exercised. For each path, the intrinsic value of the option at the time of exercise is discounted, and Monte Carlo integration helps to estimate the American put at  . Use the controls to set the parameters of the option and observe the impact of time discretization and number of GBM paths on the convergence. The more GBM paths, the better the approximation.

. Use the controls to set the parameters of the option and observe the impact of time discretization and number of GBM paths on the convergence. The more GBM paths, the better the approximation.

Contributed by: Michail Bozoudis (June 2014)

Suggested by: Michail Boutsikas

Open content licensed under CC BY-NC-SA

Snapshots

Details

In the upper graph, the dashed red line represents the approximation of the early exercise boundary. It is constructed according to the quadratic approximation analytical method [1]. The light blue area shows where the asset price is expected to be in the future according to the GBM model, at the selected "GBM confidence level". Only one for every 10 GBM paths is shown in the graph.

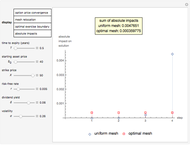

The left lower graph shows the events of early exercise per time step (before the expiry of the option) as you increase the number of GBM paths.

The right lower graph shows the American put convergence as you increase the number of GBM paths. The horizontal dashed black line represents the estimate of the American put at , according to the quadratic approximation analytical method [1].

Reference

[1] G. Barone–Adesi and R. Whaley, "Efficient Analytic Approximation of American Option Values," Journal of Finance, 42(2), 1987 pp. 301–320.

Permanent Citation

Maximizing a Bermudan Put with Two Early-Exercise Temporal Points

Maximizing a Bermudan Put with Two Early-Exercise Temporal Points

Michail Bozoudis Pricing Put Options with the Trinomial Method

Pricing Put Options with the Trinomial Method

Michail Bozoudis Pricing Put Options with the Binomial Method

Pricing Put Options with the Binomial Method

Michail Bozoudis Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Michail Bozoudis Kim's Method for Pricing American Options

Kim's Method for Pricing American Options

Michail Bozoudis Pricing Put Options with the Implicit Finite-Difference Method

Pricing Put Options with the Implicit Finite-Difference Method

Michail Bozoudis Pricing Put Options with the Crank-Nicolson Method

Pricing Put Options with the Crank-Nicolson Method

Michail Bozoudis A Canonical Optimal Stopping Problem for American Options

A Canonical Optimal Stopping Problem for American Options

Michail Bozoudis Pricing Put Options with the Explicit Finite-Difference Method

Pricing Put Options with the Explicit Finite-Difference Method

Michail Bozoudis Kim's Method with Nonuniform Time Grid for Pricing American Options

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis

-

Fitting Times-to-Failure to a Weibull Distribution

Fitting Times-to-Failure to a Weibull Distribution

Michail Bozoudis -

A Canonical Optimal Stopping Problem for American Options

Michail Bozoudis -

A Recursive Integration Method for Options Pricing

A Recursive Integration Method for Options Pricing

Michail Bozoudis -

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Michail Bozoudis -

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis -

Geometric Brownian Motion with Nonuniform Time Grid

Geometric Brownian Motion with Nonuniform Time Grid

Michail Bozoudis -

Kim's Method for Pricing American Options

Michail Bozoudis -

Simultaneous Confidence Interval for the Weibull Parameters

Simultaneous Confidence Interval for the Weibull Parameters

Michail Bozoudis -

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Michail Bozoudis -

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis -

American Options on Assets with Dividends Near Expiry

American Options on Assets with Dividends Near Expiry

Michail Bozoudis -

Hold-or-Exercise for an American Put Option

Hold-or-Exercise for an American Put Option

Michail Bozoudis -

American Capped Call Options with Exponential Cap

American Capped Call Options with Exponential Cap

Michail Bozoudis -

American Capped Call Options with Constant Cap

American Capped Call Options with Constant Cap

Michail Bozoudis -

Pricing Put Options with the Crank-Nicolson Method

Michail Bozoudis -

Pricing Put Options with the Implicit Finite-Difference Method

Michail Bozoudis -

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Michail Bozoudis -

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Michail Bozoudis -

Fitting Data to a Lognormal Distribution

Fitting Data to a Lognormal Distribution

Michail Bozoudis -

SARIMA Process Forecasting Model

SARIMA Process Forecasting Model

Michail Bozoudis