Pricing American Options with the Two- and Three-Point Maximum Methods

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

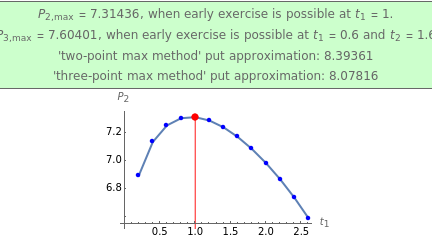

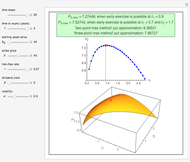

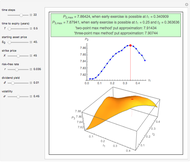

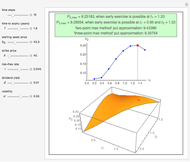

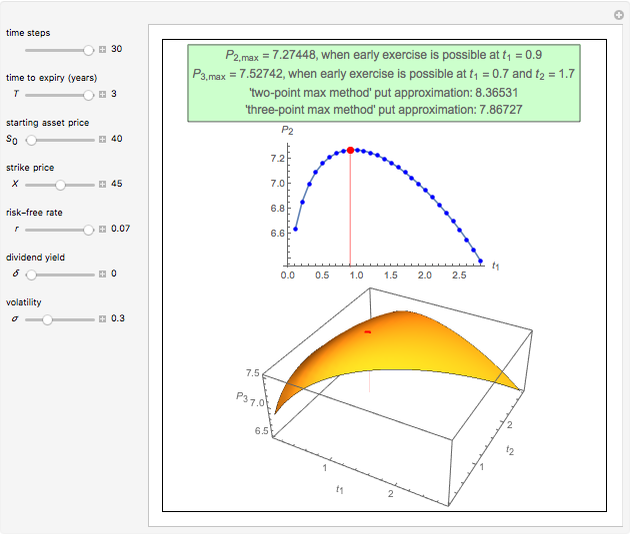

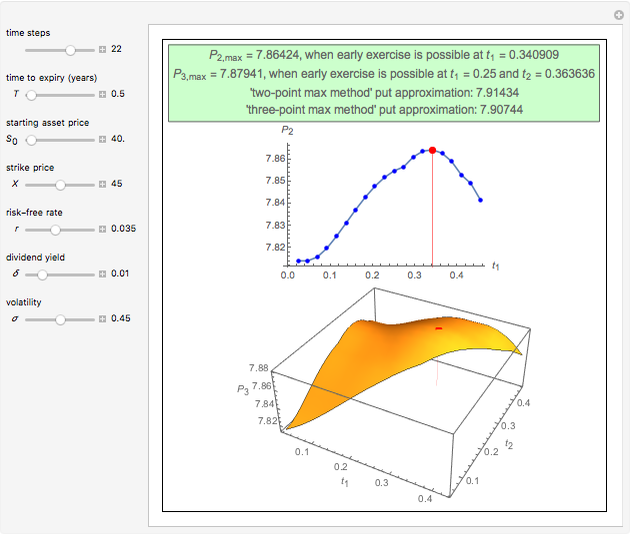

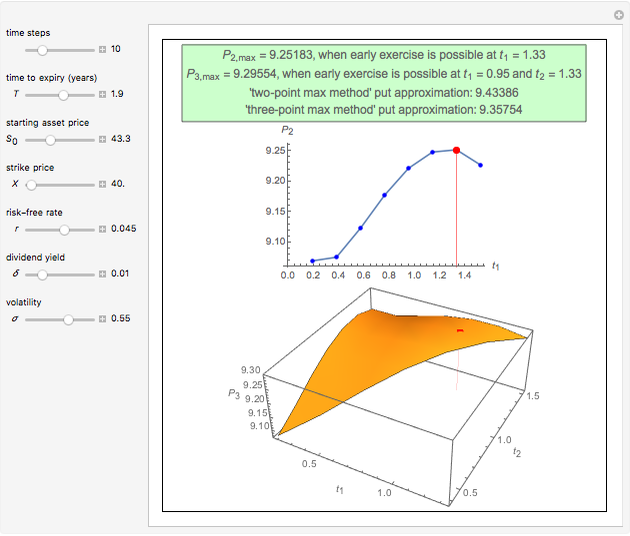

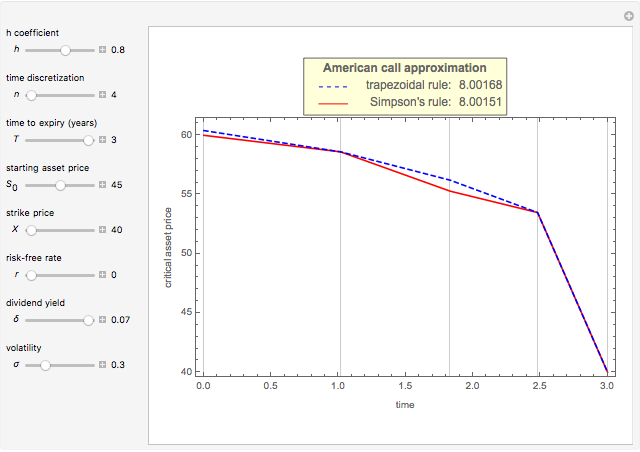

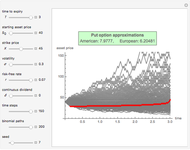

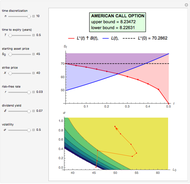

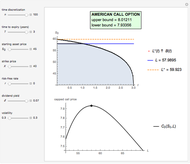

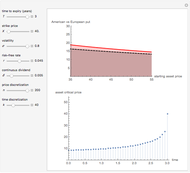

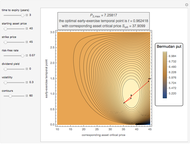

This Demonstration shows the application of the "two-point maximum" and "three-point maximum" methods [2] in order to approximate the value of an American put. The Demonstration uses the trinomial method [3] and the fact that Bermudan options approximate American options to locate the optimal early exercise temporal points and estimate the values  and

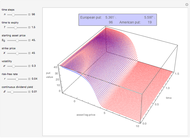

and  . Use the controllers to set the time discretization for the trinomial tree and the American option parameters.

. Use the controllers to set the time discretization for the trinomial tree and the American option parameters.

Contributed by: Michail Bozoudis (August 2014)

Suggested by: Michail Boutsikas

Open content licensed under CC BY-NC-SA

Snapshots

Details

The "two-point maximum" and "three-point maximum" methods [2] derive from the analytical method [1], which uses the values of

• a European put option  , which can only be exercised at its maturity

, which can only be exercised at its maturity  ,

,

• a Bermudan put option  , which can be exercised at

, which can be exercised at  or , and

or , and

• a Bermudan put option  , which can be exercised at

, which can be exercised at  ,

,  , or

, or .

.

Then, according to the method [1], Richardson extrapolation is applied twice to approximate the American put value  as

as  , with an error term of the form:

, with an error term of the form:  .

.

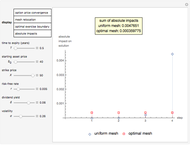

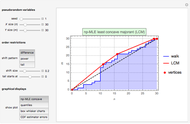

Instead, the modified "three-point maximum" method [2] uses optimally time-discretized Bermudan options with maximized values and , respectively. When Richardson extrapolation is applied twice, the American put approximation is  . The error term is again of the form , but in most cases its absolute value is smaller compared to the method [1]. The disadvantage of the modified method [2] compared to the method [1] is that it requires more computational time and effort. The "two-point maximum" method refers to the application of Richardson extrapolation once; the American put approximation is then

. The error term is again of the form , but in most cases its absolute value is smaller compared to the method [1]. The disadvantage of the modified method [2] compared to the method [1] is that it requires more computational time and effort. The "two-point maximum" method refers to the application of Richardson extrapolation once; the American put approximation is then  , with an error term of the form

, with an error term of the form  .

.

References

[1] R. Geske and H. Johnson, "The American Put Option Valued Analytically," The Journal of Finance, 39(5), 1984 pp. 1511–1524.

[2] D. Bunch and H. Johnson, "A Simple Numerically Efficient Valuation Method for American Puts Using a Modified Geske–Johnson Approach," The Journal of Finance, 47(2), 1992 pp. 809–816.

[3] P. Boyle, "Option Valuation Using a Three-Jump Process," International Options Journal, 3, 1986 pp. 7–12.

Permanent Citation

Kim's Method for Pricing American Options

Kim's Method for Pricing American Options

Michail Bozoudis Kim's Method with Nonuniform Time Grid for Pricing American Options

Kim's Method with Nonuniform Time Grid for Pricing American Options

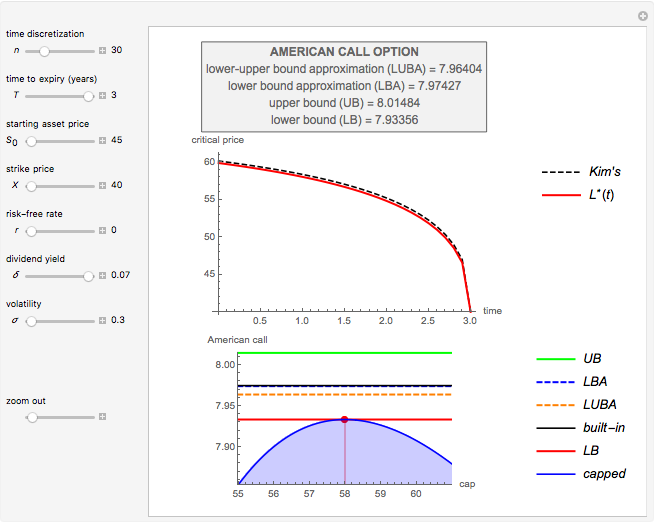

Michail Bozoudis Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis Pricing Put Options with the Trinomial Method

Pricing Put Options with the Trinomial Method

Michail Bozoudis A Recursive Integration Method for Options Pricing

A Recursive Integration Method for Options Pricing

Michail Bozoudis Pricing Put Options with the Binomial Method

Pricing Put Options with the Binomial Method

Michail Bozoudis Pricing Put Options with the Crank-Nicolson Method

Pricing Put Options with the Crank-Nicolson Method

Michail Bozoudis Pricing Put Options with the Explicit Finite-Difference Method

Pricing Put Options with the Explicit Finite-Difference Method

Michail Bozoudis Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

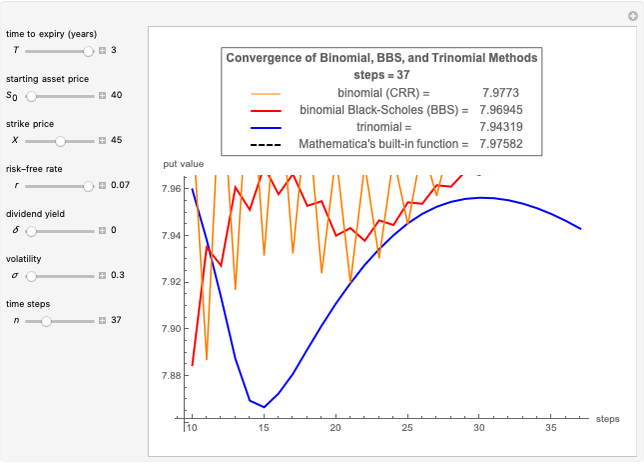

Michail Bozoudis Convergence of Binomial, Binomial Black-Scholes, and Trinomial Option Pricing Methods

Convergence of Binomial, Binomial Black-Scholes, and Trinomial Option Pricing Methods

Michail Bozoudis

-

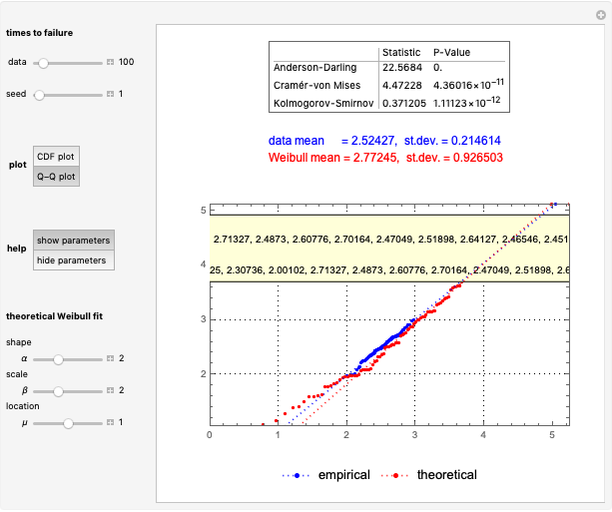

Fitting Times-to-Failure to a Weibull Distribution

Fitting Times-to-Failure to a Weibull Distribution

Michail Bozoudis -

A Canonical Optimal Stopping Problem for American Options

A Canonical Optimal Stopping Problem for American Options

Michail Bozoudis -

A Recursive Integration Method for Options Pricing

Michail Bozoudis -

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Michail Bozoudis -

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis -

Geometric Brownian Motion with Nonuniform Time Grid

Geometric Brownian Motion with Nonuniform Time Grid

Michail Bozoudis -

Kim's Method for Pricing American Options

Michail Bozoudis -

Simultaneous Confidence Interval for the Weibull Parameters

Simultaneous Confidence Interval for the Weibull Parameters

Michail Bozoudis -

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Michail Bozoudis -

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis -

American Options on Assets with Dividends Near Expiry

American Options on Assets with Dividends Near Expiry

Michail Bozoudis -

Hold-or-Exercise for an American Put Option

Hold-or-Exercise for an American Put Option

Michail Bozoudis -

American Capped Call Options with Exponential Cap

American Capped Call Options with Exponential Cap

Michail Bozoudis -

American Capped Call Options with Constant Cap

American Capped Call Options with Constant Cap

Michail Bozoudis -

Pricing Put Options with the Crank-Nicolson Method

Michail Bozoudis -

Pricing Put Options with the Implicit Finite-Difference Method

Pricing Put Options with the Implicit Finite-Difference Method

Michail Bozoudis -

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Michail Bozoudis -

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Michail Bozoudis -

Fitting Data to a Lognormal Distribution

Fitting Data to a Lognormal Distribution

Michail Bozoudis -

SARIMA Process Forecasting Model

SARIMA Process Forecasting Model

Michail Bozoudis