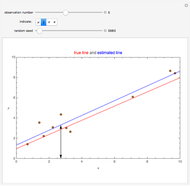

Estimating the Local Mean Function

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

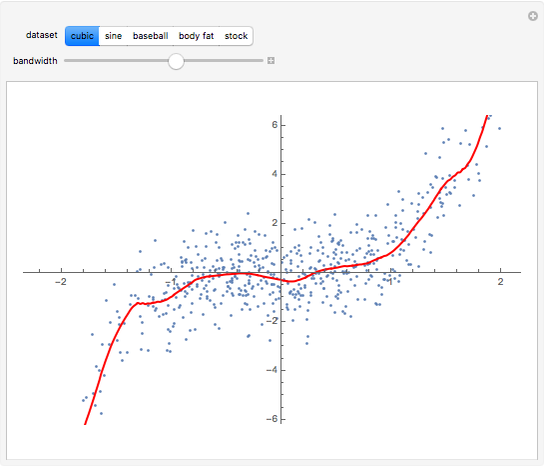

The linear regression model  relies on a number of crucial assumptions, the most important of which is a linear relationship between the covariate

relies on a number of crucial assumptions, the most important of which is a linear relationship between the covariate  and the dependent variable

and the dependent variable  . One way of generalizing the standard linear regression model is to extend it to the nonlinear form

. One way of generalizing the standard linear regression model is to extend it to the nonlinear form  , where

, where  and

and  are real-valued functions and

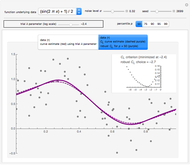

are real-valued functions and  is an independent, identically distributed sequence of standard normal random variables. We study five different sets of data (three "real" and two simulated) to illustrate how kernel-weighted least-squares regression can be used to estimate the local mean function

is an independent, identically distributed sequence of standard normal random variables. We study five different sets of data (three "real" and two simulated) to illustrate how kernel-weighted least-squares regression can be used to estimate the local mean function  .

.

Contributed by: Jeff Hamrick (December 2008)

Open content licensed under CC BY-NC-SA

Snapshots

Details

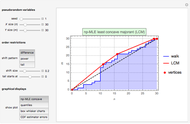

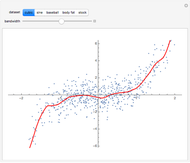

There is an extensive literature on nonlinear regression and nonparametric estimation techniques. We refer the reader to the notable book by Fan and Yao and extensive work by Bjerve and Doksum. Roughly speaking, the procedure to estimate  can be implemented in the following fashion. First, take a set of evenly spaced design points over an interior interval of the empirical support of the covariate . Then, at each design point, solve a kernel-weighted least squares problem to locally fit a polynomial of order

can be implemented in the following fashion. First, take a set of evenly spaced design points over an interior interval of the empirical support of the covariate . Then, at each design point, solve a kernel-weighted least squares problem to locally fit a polynomial of order  . (In this Demonstration, the local fit is parabolic.)

. (In this Demonstration, the local fit is parabolic.)

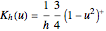

By "kernel-weighted", we mean that the data are weighted according to the Epanechnikov kernel  , where

, where  ,

,  is a design point, and

is a design point, and  is the "kernel bandwidth". The variable effectively controls the amount of nearby data that are permitted to influence the estimate of (and its derivatives) locally. There are a variety of techniques or heuristics available to choose . You can vary the size of the bandwidth. Smaller bandwidths reveal too many of the local features of the data, perhaps, and larger bandwidths oversmooth the data.

is the "kernel bandwidth". The variable effectively controls the amount of nearby data that are permitted to influence the estimate of (and its derivatives) locally. There are a variety of techniques or heuristics available to choose . You can vary the size of the bandwidth. Smaller bandwidths reveal too many of the local features of the data, perhaps, and larger bandwidths oversmooth the data.

By solving a kernel-weighted least squares regression at each design point, we obtain an estimate of the value of and its first two derivatives at each design point. We then have all the information we need to fit a spline.

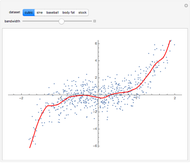

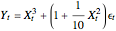

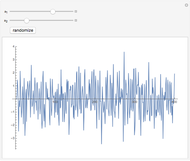

The "cubic" set of data is a simulated set formed by generating 600 realizations of with a standard normal distribution and then simulating  , where are independently simulated standard normal random variables.

, where are independently simulated standard normal random variables.

The "sine" set of data is another simulated set, formed by first generating 600 realizations of with a uniform distribution over the interval  . We then obtain simulations of according to the rule

. We then obtain simulations of according to the rule  , where are independently simulated standard normal random variables.

, where are independently simulated standard normal random variables.

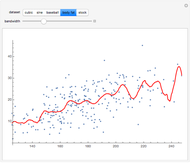

The "baseball" data consists of performance data for all regular major league baseball players during the 1999 baseball season. We compute the overall proportion of hits to at-bats, and the proportion of hits to at-bats when there is a teammate in scoring position. The two proportions are obviously positively correlated, but the nonlinear regression model offers a potentially more useful fit than the usual linear regression model. These data were taken from John Rasp's website.

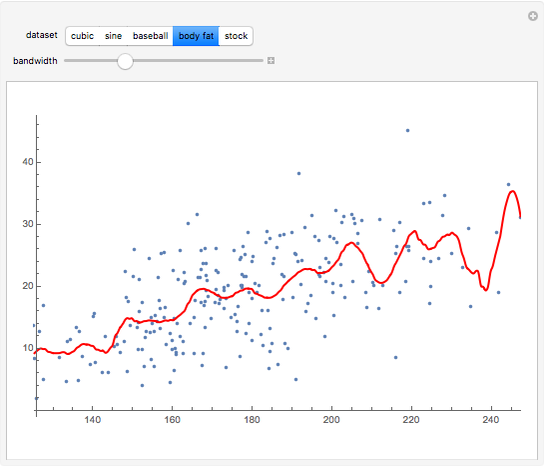

The "body fat" data were also taken from John Rasp's website. The data were taken from a sample of 252 men. The covariate  is the weight (in pounds) of the male subject, and the dependent variable

is the weight (in pounds) of the male subject, and the dependent variable  is the body fat percentage (obtained through an underwater weighing procedure).

is the body fat percentage (obtained through an underwater weighing procedure).

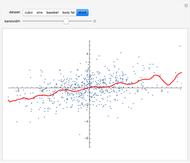

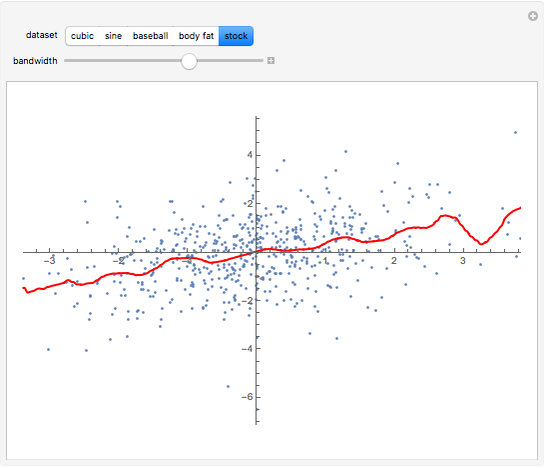

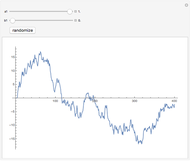

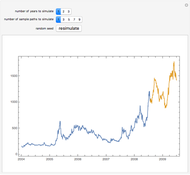

The "stock" data consists of U.S. equity returns ( variable) and French equity returns ( variable) for 1000 trading days in the late 1990s.

Permanent Citation

Kernel Density Estimation

Kernel Density Estimation

Jeff Hamrick Estimating a Centered Matérn (1) Process: Three Alternatives to Maximum Likelihood via Conjugate Gradient Linear Solvers

Estimating a Centered Matérn (1) Process: Three Alternatives to Maximum Likelihood via Conjugate Gradient Linear Solvers

Didier A. Girard How Loess Works

How Loess Works

Ian McLeod Nonparametric Curve Estimation by Smoothing Splines: Unbiased-Risk-Estimate Selector and its Robust Version via Randomized Choices

Nonparametric Curve Estimation by Smoothing Splines: Unbiased-Risk-Estimate Selector and its Robust Version via Randomized Choices

Didier A. Girard Auto-Regressive Simulation (Second-Order)

Auto-Regressive Simulation (Second-Order)

David von Seggern (University of Nevada) Autoregressive Moving-Average Simulation (First Order)

Autoregressive Moving-Average Simulation (First Order)

David von Seggern (University of Nevada) Estimating a Distribution Function Subject to a Stochastic Order Restriction

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Michail Bozoudis and Vasileios Papachatzis Mean, Fitted-Value, Error, and Residual in Simple Linear Regression

Mean, Fitted-Value, Error, and Residual in Simple Linear Regression

Ian McLeod Maximum Likelihood Estimation

Maximum Likelihood Estimation

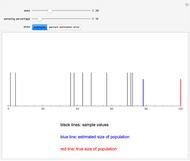

Marc Brodie (Wheeling Jesuit University) Estimating the Size of a Population

Estimating the Size of a Population

Heikki Ruskeepää

-

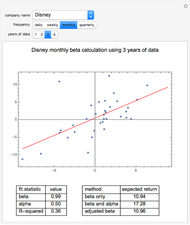

Expected Returns of the Dow Industrials, Beta Model

Expected Returns of the Dow Industrials, Beta Model

Jeff Hamrick -

Exploring Measures of Association

Exploring Measures of Association

Jeff Hamrick -

Bootstrapping Credit Default Swap Data

Bootstrapping Credit Default Swap Data

Jeff Hamrick -

Linear Dependence between Two Bernoulli Random Variables

Linear Dependence between Two Bernoulli Random Variables

Jeff Hamrick -

Estimating the Local Mean Function

Estimating the Local Mean Function

Jeff Hamrick -

Acceptance/Rejection Sampling

Acceptance/Rejection Sampling

Jeff Hamrick -

Simulating the 2008 U.S. Presidential Election

Simulating the 2008 U.S. Presidential Election

Jeff Hamrick -

The Method of Inverse Transforms

The Method of Inverse Transforms

Jeff Hamrick -

The Perturbed Rat

The Perturbed Rat

Jeff Hamrick -

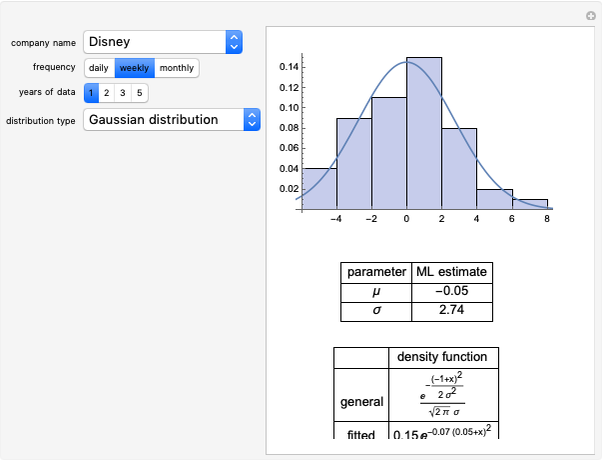

Modeling Return Distributions

Modeling Return Distributions

Jeff Hamrick -

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Jeff Hamrick -

The Method of Common Random Numbers: An Example

The Method of Common Random Numbers: An Example

Jeff Hamrick -

The Envelope Theorem: Numerical Examples

The Envelope Theorem: Numerical Examples

Jeff Hamrick -

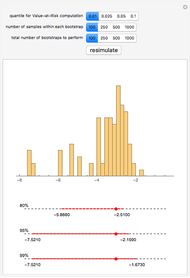

Bootstrapping to Compute Value-at-Risk Standard Errors

Bootstrapping to Compute Value-at-Risk Standard Errors

Jeff Hamrick -

Expected Returns of the Dow Industrials, Fama-French Model

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick -

Kernel Density Estimation

Jeff Hamrick -

Simulating Asset Prices with a GARCH(1,1) Model

Simulating Asset Prices with a GARCH(1,1) Model

Jeff Hamrick