Modeling Return Distributions

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

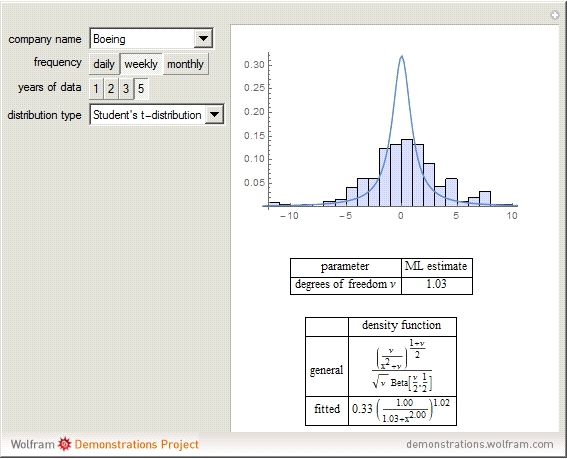

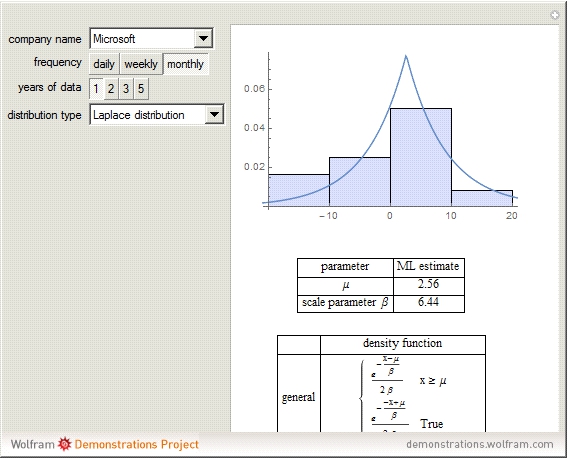

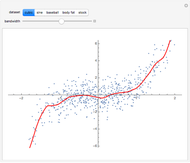

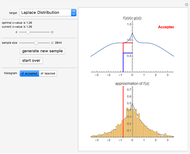

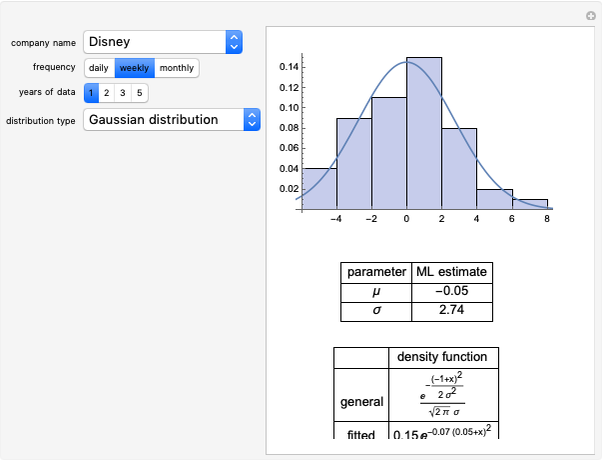

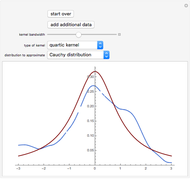

We use numerical maximum likelihood estimation to obtain the parameters governing probability distributions that might plausibly generate the daily, weekly, monthly, or quarterly return distributions of stocks from the Dow 30. The candidate distribution types should probably be continuous and supported on the whole real line. So, we choose to investigate the Gaussian distribution, Student's  -distribution, the Gumbel distribution, the Cauchy distribution, and the Laplace distribution. We show a histogram of the return data for a particular time horizon and frequency, as well as the density function with the fitted parameters.

-distribution, the Gumbel distribution, the Cauchy distribution, and the Laplace distribution. We show a histogram of the return data for a particular time horizon and frequency, as well as the density function with the fitted parameters.

Contributed by: Jeff Hamrick (March 2011)

Additional contributions by: Jason Cawley

Open content licensed under CC BY-NC-SA

Snapshots

Details

In this Demonstration, we define the returns of a stock  by

by  for

for  . Hence, the number

. Hence, the number  corresponds to a positive 5% return and

corresponds to a positive 5% return and  corresponds to a negative 9% return.

corresponds to a negative 9% return.

Permanent Citation

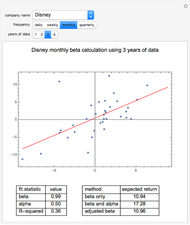

Expected Returns of the Dow Industrials, Beta Model

Expected Returns of the Dow Industrials, Beta Model

Jeff Hamrick and Jason Cawley Expected Returns of the Dow Industrials, Fama-French Model

Expected Returns of the Dow Industrials, Fama-French Model

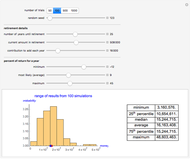

Jeff Hamrick and Jason Cawley Monte Carlo Simulation of Retirement Savings with Variable Annual Return

Monte Carlo Simulation of Retirement Savings with Variable Annual Return

Paul Savory (University of Nebraska-Lincoln) The Effect of Holding Period on Real Estate Investment Return

The Effect of Holding Period on Real Estate Investment Return

Roger J. Brown Stock Market Returns by Party

Stock Market Returns by Party

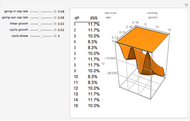

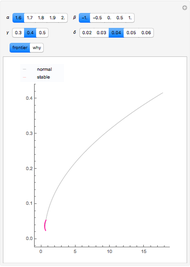

Theodore Gray Forming the Efficient Frontier When Returns Are Non-Normal

Forming the Efficient Frontier When Returns Are Non-Normal

Roger J. Brown Value Added Growth Model

Value Added Growth Model

Roger J. Brown Trader Dynamics in Minimal Models of Financial Complexity

Trader Dynamics in Minimal Models of Financial Complexity

Philip Maymin Exploring Minimal Models of the Complexity of Security Prices

Exploring Minimal Models of the Complexity of Security Prices

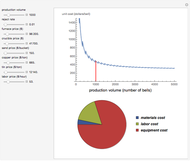

Philip Maymin Process-Based Cost Model for Sand-Casting Bronze Bells

Process-Based Cost Model for Sand-Casting Bronze Bells

Sam Shames

-

Expected Returns of the Dow Industrials, Beta Model

Jeff Hamrick -

Exploring Measures of Association

Exploring Measures of Association

Jeff Hamrick -

Bootstrapping Credit Default Swap Data

Bootstrapping Credit Default Swap Data

Jeff Hamrick -

Linear Dependence between Two Bernoulli Random Variables

Linear Dependence between Two Bernoulli Random Variables

Jeff Hamrick -

Estimating the Local Mean Function

Estimating the Local Mean Function

Jeff Hamrick -

Acceptance/Rejection Sampling

Acceptance/Rejection Sampling

Jeff Hamrick -

Simulating the 2008 U.S. Presidential Election

Simulating the 2008 U.S. Presidential Election

Jeff Hamrick -

The Method of Inverse Transforms

The Method of Inverse Transforms

Jeff Hamrick -

The Perturbed Rat

The Perturbed Rat

Jeff Hamrick -

Modeling Return Distributions

Modeling Return Distributions

Jeff Hamrick -

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Pricing a European-Style Arithmetic Asian Option: Comparing Bootstrapping and Simulation Approaches

Jeff Hamrick -

The Method of Common Random Numbers: An Example

The Method of Common Random Numbers: An Example

Jeff Hamrick -

The Envelope Theorem: Numerical Examples

The Envelope Theorem: Numerical Examples

Jeff Hamrick -

Bootstrapping to Compute Value-at-Risk Standard Errors

Bootstrapping to Compute Value-at-Risk Standard Errors

Jeff Hamrick -

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick -

Kernel Density Estimation

Kernel Density Estimation

Jeff Hamrick -

Simulating Asset Prices with a GARCH(1,1) Model

Simulating Asset Prices with a GARCH(1,1) Model

Jeff Hamrick