Net Lease Economics

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

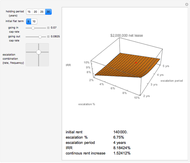

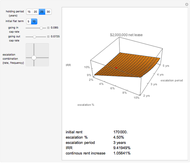

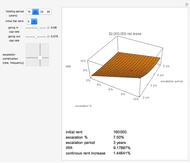

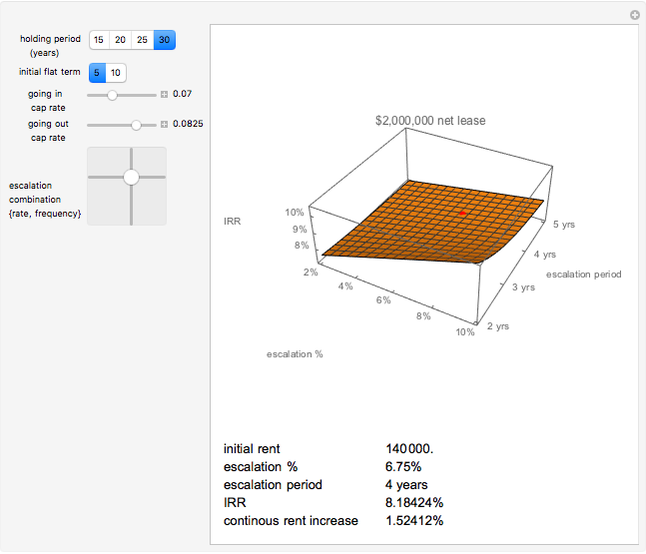

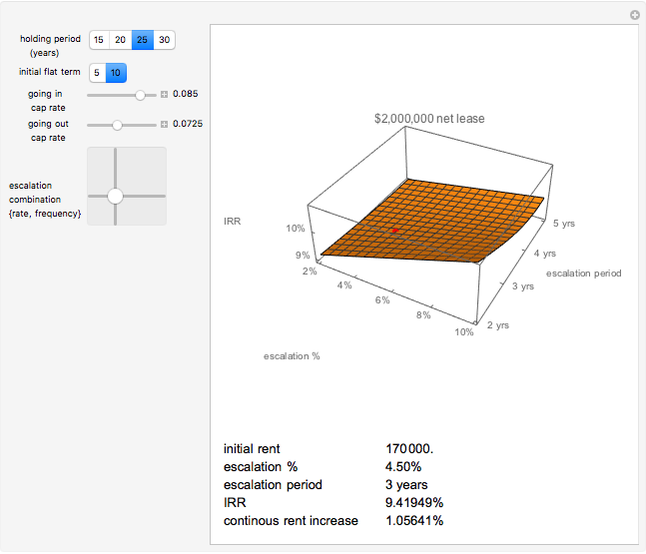

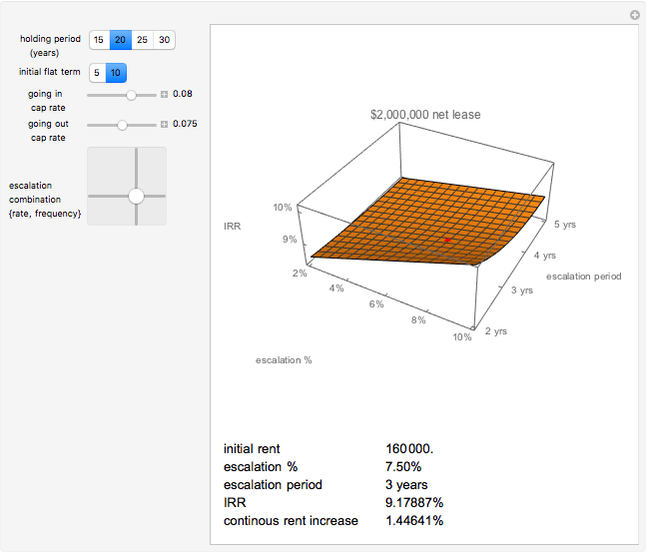

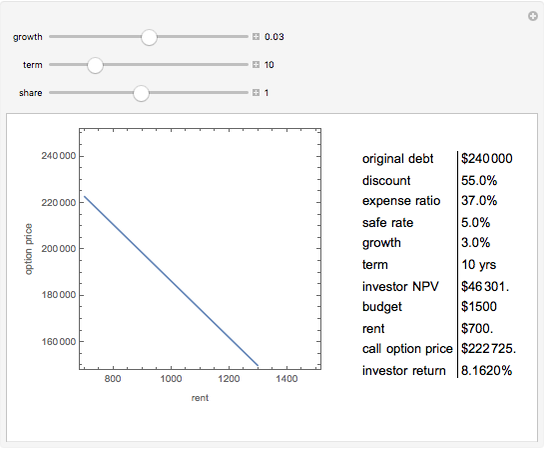

The proliferation of national chains, franchises, and the marketing concept of "branding" has produced a real estate investment commonly known as the "single tenant net lease investment". This vehicle essentially trades as real estate's equivalent of bonds with two important differences. First, the final payment of a standard bond is usually a fixed, known amount. In the net lease investment, the reversion of possession at lease expiration makes the residual value of the property the equivalent "final payment". Second, while bond interest rates are typically fixed for the term, net lease payments are rent, typically adjusted at regular intervals over time, based on a fixed escalation or cost-of-living increase.

[more]

Contributed by: Roger J. Brown (April 2008)

Reproduced by permission of Academic Press from Private Real Estate Investment ©2005

Open content licensed under CC BY-NC-SA

Snapshots

Details

The negotiation process between landlord and tenant becomes an important aspect of this analysis. The consequence of transferring possession of a well-located parcel of realty to a user for decades has a material effect on value. Both parties overwork their respective crystal balls as they balance the trade-off of initial rent, future escalations and terminal value at expiration.

The valuation of the reversion is the subject of much speculation, namely because it is so far into the future. There are also ramifications over time as local rental market conditions fluctuate. Over a 25-year period at different points in time, depending on the relationship between market rent and contract rent, there will either be a "bargain element" in the rent for the tenant when market rents exceed the lease rate (making the lease an asset in the tenant's hands and a liability in the landlord's hands); or for the landlord when the contract rent exceeds the local market rent (making the lease an asset to the landlord and a burden on the tenant).

A popular variation to the net lease concept is the net ground lease. Under this scenario the landlord leases only the ground and the tenant builds its own building on the land. Many new issues emerge in this scenario. The building may be viewed as a large "security deposit" assuring performance of the lease. The reversion of the land means the landlord receives the tenant's building (a variation on the notion that "you can't take it with you"). Typically this results in a longer net lease term (or a series of renewal options) that permits the tenant to amortize the building.

More information is available in Chapter Four of [1] and at mathestate.com.

Reference

[1] R. J. Brown, Private Real Estate Investment: Data Analysis and Decision Making, Burlington, MA: Elsevier Academic Press, 2005.

Permanent Citation

Net Present Value

Net Present Value

Fiona Maclachlan The Effect of Holding Period on Real Estate Investment Return

The Effect of Holding Period on Real Estate Investment Return

Roger J. Brown Explaining Real Estate Price Bubbles

Explaining Real Estate Price Bubbles

Roger J. Brown Value Added Growth Model

Value Added Growth Model

Roger J. Brown Risk, Ownership, and Control

Risk, Ownership, and Control

Roger J. Brown Land Use Regulation and Municipal Utility

Land Use Regulation and Municipal Utility

Roger J. Brown Property Coinsurance

Property Coinsurance

Seth J. Chandler Tax Rates and Tax Revenue

Tax Rates and Tax Revenue

Seth J. Chandler Constant Risk Aversion Utility Functions

Constant Risk Aversion Utility Functions

Seth J. Chandler Bilateral Accident Model

Bilateral Accident Model

Seth J. Chandler

-

Dissolving Partnerships

Dissolving Partnerships

Roger J. Brown -

Forming the Efficient Frontier When Returns Are Non-Normal

Forming the Efficient Frontier When Returns Are Non-Normal

Roger J. Brown -

Spectral Measures

Spectral Measures

Roger J. Brown -

Granger-Orr Running Variance Test

Granger-Orr Running Variance Test

Roger J. Brown -

Capitalization Rate Probability

Capitalization Rate Probability

Roger J. Brown -

Net Lease Economics

Net Lease Economics

Roger J. Brown -

The Refinance Decision

The Refinance Decision

Roger J. Brown -

True Cost of Variable Rate Mortgage Funds

True Cost of Variable Rate Mortgage Funds

Roger J. Brown -

Term Structure of Interest Rates

Term Structure of Interest Rates

Roger J. Brown -

Generalized Central Limit Theorem

Generalized Central Limit Theorem

Roger J. Brown -

Inflation-Adjusted Yield

Inflation-Adjusted Yield

Roger J. Brown -

Simulating the IRR

Simulating the IRR

Roger J. Brown -

Real Options

Real Options

Roger J. Brown -

The Price-Terms Tradeoff

The Price-Terms Tradeoff

Roger J. Brown -

Fitting an Elephant

Fitting an Elephant

Roger J. Brown -

Solving the Subprime Loan Problem

Solving the Subprime Loan Problem

Roger J. Brown -

Why Location Matters: The Bid Rent Curve

Why Location Matters: The Bid Rent Curve

Roger J. Brown -

Explaining Real Estate Price Bubbles

Roger J. Brown -

Value Added Growth Model

Roger J. Brown -

Connecting the CDF and the PDF

Connecting the CDF and the PDF

Roger J. Brown