Tax Rates and Tax Revenue

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

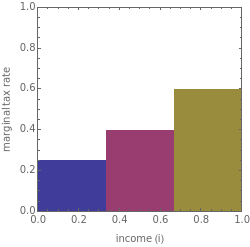

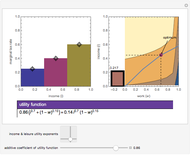

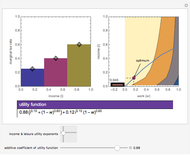

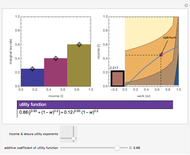

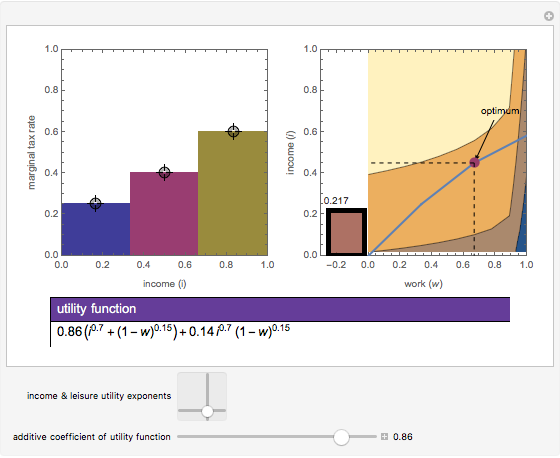

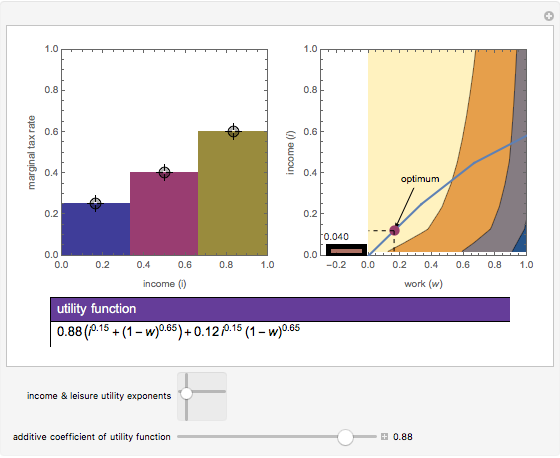

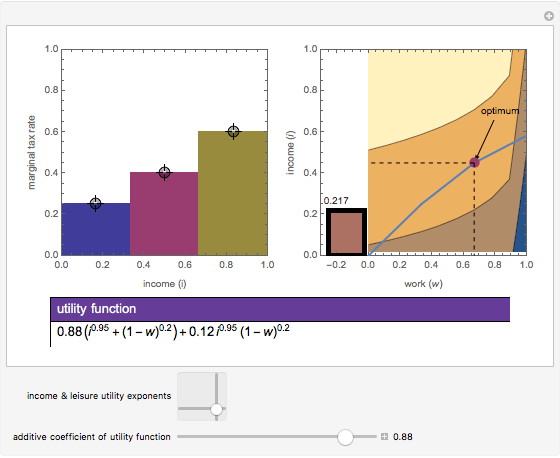

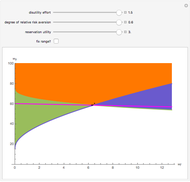

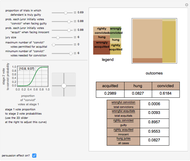

A significant debate in tax policy is the extent to which increasing marginal rates of taxation will increase tax revenues. This Demonstration lets you explore this issue by letting you set marginal rates for different levels of income and parameters of the taxpayers' utility as a function of the amount they work and the amount of net income they receive. The graphic on the top left lets you set tax rates for three different income brackets. The graphic on the top right shows the utility of the taxpayer for different levels of work and income, the feasible trade-offs between the two given the tax structure. The copper rectangle at the left of the top right graphic shows the amount of tax revenue the government receives. The top panel shows the utility function to be optimized. This model examines the effects of changing tax rates on a single hypothetical taxpayer. With multiple taxpayers involved, as would be the case in the real world, the effect of changing tax rates is considerably more complex.

Contributed by: Seth J. Chandler (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

The utility function employed here is a linear combination of: (1) a multiplicative utility function in which the utility derived from leisure ( is multiplied by the utility derived from net income; and (2) an additive utility function in which the utility derived from leisure is added to the utility derived from net income. This parameterization of utility allows an indeterminacy in the effect of changes in tax rates on tax revenues.

is multiplied by the utility derived from net income; and (2) an additive utility function in which the utility derived from leisure is added to the utility derived from net income. This parameterization of utility allows an indeterminacy in the effect of changes in tax rates on tax revenues.

Permanent Citation

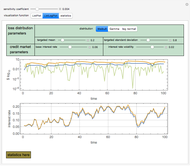

Moral Hazard

Moral Hazard

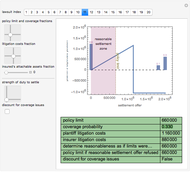

Seth J. Chandler Efficient Single Limit Liability Insurance

Efficient Single Limit Liability Insurance

Seth J. Chandler Certainty Equivalent Wealth

Certainty Equivalent Wealth

Seth J. Chandler Insurance Disclosures

Insurance Disclosures

Seth J. Chandler The Efficient Dual-Limit Liability Insurance Contract

The Efficient Dual-Limit Liability Insurance Contract

Seth J. Chandler Property Coinsurance

Property Coinsurance

Seth J. Chandler Bilateral Accident Model

Bilateral Accident Model

Seth J. Chandler Moral Hazard and Least-Cost Contracts: Impact of Changes in Conditional Probabilities

Moral Hazard and Least-Cost Contracts: Impact of Changes in Conditional Probabilities

Randy Silvers (Deakin University) Moral Hazard and Least-Cost Contracts: Impact of Changes in Agent Preferences

Moral Hazard and Least-Cost Contracts: Impact of Changes in Agent Preferences

Randy Silvers (Deakin University) The Duty to Settle

The Duty to Settle

Seth J. Chandler

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

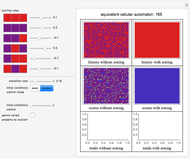

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler