Option Prices under the Fractional Black-Scholes Model

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

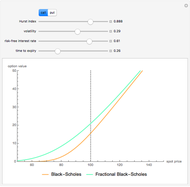

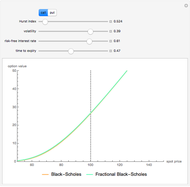

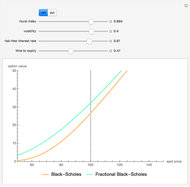

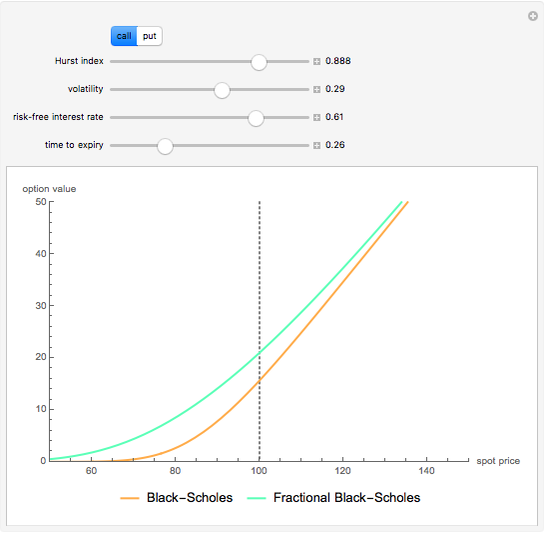

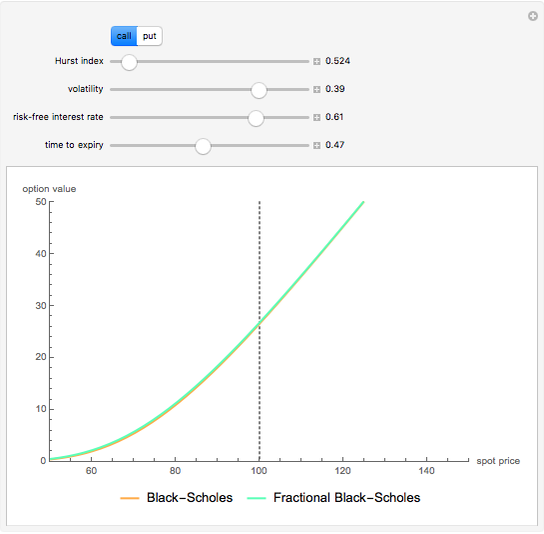

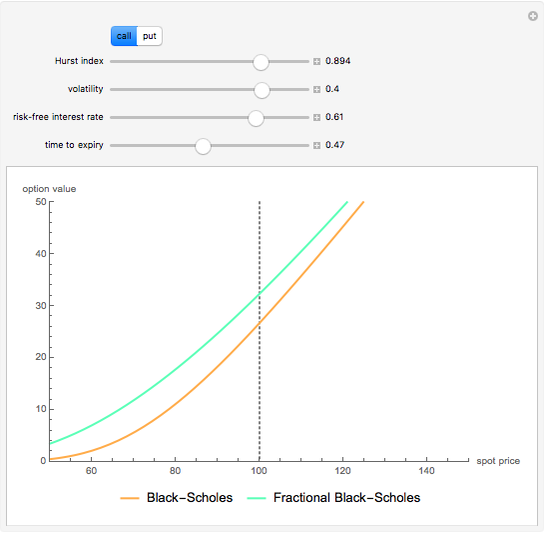

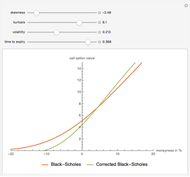

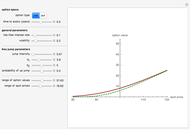

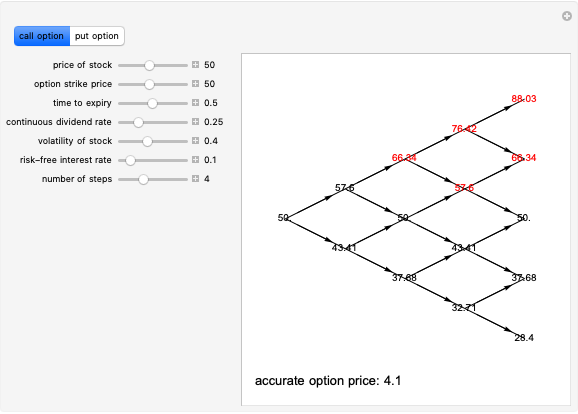

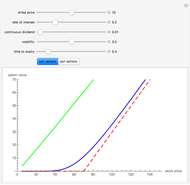

This Demonstration shows the values of vanilla European options in a model based on fractional Brownian motion and on ordinary geometric Brownian motion (the Black–Scholes model). The strike price is fixed at 100. Options values in this model generally overprice Black–Scholes values.

Contributed by: Andrzej Kozlowski (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

In spite of its having attractive properties as a model for the stock exchange, the suitability of fractional Brownian motion for option pricing is controversial.

There is some evidence that certain stock returns may exhibit the phenomenon of "long memory" (slowly decreasing covariance between returns at different times) [2], though this seems to be fairly weak. It is also generally accepted that stock returns display the phenomenon of "clustering". None of these phenomena appear in semi-martingale models, such as the Black–Scholes model. They do appear, however, if we consider the analogue of the Black–Scholes model based on fractional Brownian motion with Hurst index  , where

, where  .

.

Since fractional Brownian motion is not a semi-martingale, the Itô theory of stochastic integrals cannot be directly applied to it. One can try to replace the Itô integral by a version of the pathwise Riemann–Stieltjes integral, but then, as has been shown by Rogers [6], the resulting model of option values admits arbitrage. As this is contrary to empirical evidence, it has been generally thought that models based on fractional Brownian are not usable for option pricing. Hu and Øksendal [4] defined a new stochastic integral based on the Skorokhod integral and the Wick product and showed that a model based on this integral does not admit arbitrage. Unfortunately, it was shown in [1] that this model does not make economic sense. However, recently Guasoni [3] showed that as soon as one introduces proportional transaction costs in the fractional Black-Scholes model, arbitrage opportunities vanish.

In this Demonstration we adopt a different approach, based on the work of Norros, Valkeila, and Virtamo [3]. They have shown that one can define a centered Gaussian martingale (called "the fundamental martingale") that generates the same filtration as the fractional Brownian motion. Since it is the filtration rather than the stochastic process itself that represents information provided by the market, it seems reasonable to use this martingale for option pricing. It is then easy to obtain formulas analogous to the classical Black–Scholes formulas (and coinciding with them when the Hurst index is  ).

).

[1] T. Bjork and H. Hult, "A Note on Wick Products and the Fractional Black-Scholes Model," Finance Stoch., 9(2), 2005 pp. 197–209.

[2] N. J. Cutland, P. E. Kopp, and W. Willinger, "Stock Price Returns and the Joseph Effect: A Fractional Version of the Black-Scholes Model," in Proceedings of the Former Ascona Conferences on Stochastic Analysis, Random Fields and Applications, Progress in Probability, Vol. 36, Basel: Birkhauser, 1995 pp. 327–351.

[3] P. Guasoni, "No Arbitrage under Transaction Costs, with Fractional Brownian Motion and Beyond," Math. Finance, 16(3), 2006 pp. 569–582.

[4] Y. Hu and B. Øksendal, "Fractional White Noise Calculus and Applications to Finance," Inf. Dim. Anal. Quantum Probab. Rel. Top., 6(1), 2003 pp. 1–32.

[5] I. Norros, E. Valkeila, and J. Virtamo, "A Girsanov-Type Formula for the Fractional Brownian Motion," in Proceedings of the First Nordic-Russian Symposium on Stochastics, Helsinki, Finland, 1996.

[6] L. C. G. Rogers, "Arbitrage with Fractional Brownian Motion," Math. Finance, 7(1), 1997 pp. 95–105.

Permanent Citation

The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

The Difference between European Option Prices in the Black-Scholes and NIG Models Computed with the DFT

Andrzej Kozlowski Hedging the Black-Scholes Call Option

Hedging the Black-Scholes Call Option

Andrzej Kozlowski The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski Option Prices in the Kou Jump Diffusion Model

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski Exploring the Black-Scholes Formula

Exploring the Black-Scholes Formula

Andrzej Kozlowski The Price of a Call Option on Electrical Power

The Price of a Call Option on Electrical Power

Andrzej Kozlowski Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

Pricing a Bermudan Option with the Longstaff-Schwartz Monte Carlo Method

Andrzej Kozlowski The Russian Option: Reduced Regret

The Russian Option: Reduced Regret

Andrzej Kozlowski Hedging the European Put Option

Hedging the European Put Option

Andrzej Kozlowski American Call and Put Option

American Call and Put Option

Andrzej Kozlowski

-

The Black-Scholes European Call Option Formula Corrected Using the Gram-Charlier Expansion

Andrzej Kozlowski -

Option Prices in the Kou Jump Diffusion Model

Andrzej Kozlowski -

The Polar and Bipolar of a Convex Polytope

The Polar and Bipolar of a Convex Polytope

Andrzej Kozlowski -

Two Jump Diffusion Processes

Two Jump Diffusion Processes

Andrzej Kozlowski -

The Vieta Mapping for the Coxeter Group A_2

The Vieta Mapping for the Coxeter Group A_2

Andrzej Kozlowski -

The Bifurcation Set of the Space of Smooth Real Functions

The Bifurcation Set of the Space of Smooth Real Functions

Andrzej Kozlowski -

The Swallowtail Singularity

The Swallowtail Singularity

Andrzej Kozlowski -

Singularities of an Ellipsoidal Wave Front

Singularities of an Ellipsoidal Wave Front

Andrzej Kozlowski -

Nonuniqueness of Option Pricing Under the Meixner Model

Nonuniqueness of Option Pricing Under the Meixner Model

Andrzej Kozlowski -

Coin Machine

Coin Machine

Andrzej Kozlowski -

A Mean-Reverting Jump Diffusion Process

A Mean-Reverting Jump Diffusion Process

Andrzej Kozlowski -

Standard American and European Options

Standard American and European Options

Andrzej Kozlowski -

Density of the Kou Jump Diffusion Process

Density of the Kou Jump Diffusion Process

Andrzej Kozlowski -

The Meixner Process

The Meixner Process

Andrzej Kozlowski -

Fitting the Meixner Distribution to S&P 500 Returns

Fitting the Meixner Distribution to S&P 500 Returns

Andrzej Kozlowski -

Simple Graphs and Their Binomial Edge Ideals

Simple Graphs and Their Binomial Edge Ideals

Andrzej Kozlowski -

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

The Eneström-Kakeya Bounds for Roots of a Polynomial with Positive Coefficients

Andrzej Kozlowski -

Newton Polygon and Branching of Algebraic Curves

Newton Polygon and Branching of Algebraic Curves

Andrzej Kozlowski -

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Counting the Number of Roots of Transcendental Functions in Bounded Regions Using Winding Numbers

Andrzej Kozlowski -

The Space of Inner Products

The Space of Inner Products

Andrzej Kozlowski