The Duty to Settle

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

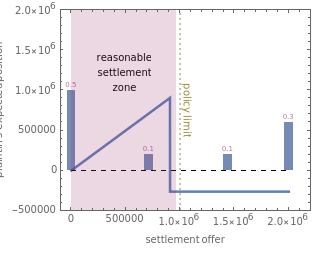

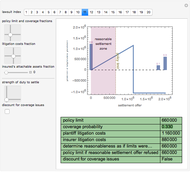

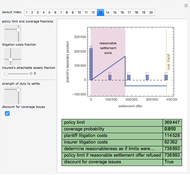

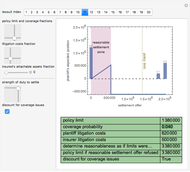

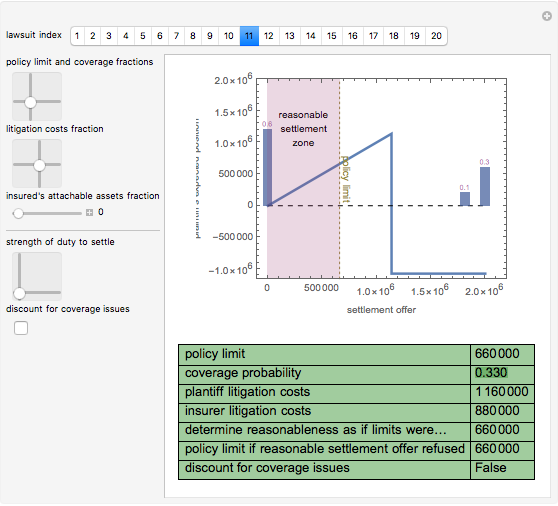

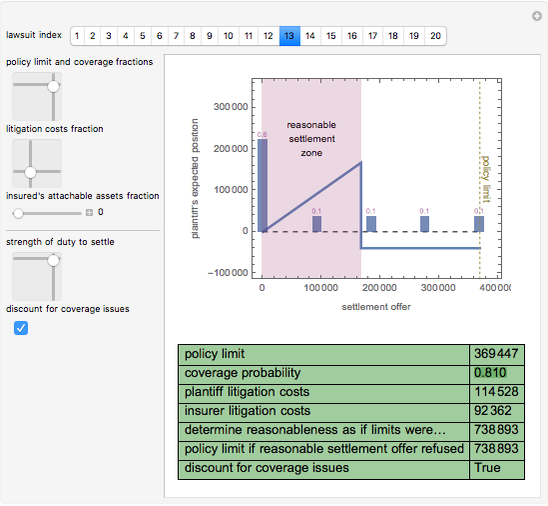

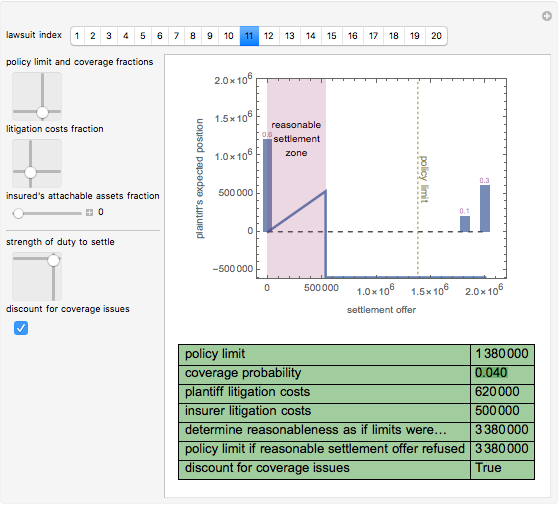

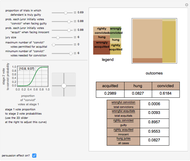

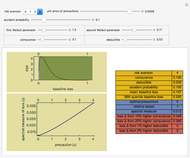

Courts imply a "duty to settle" on the part of the insurer into almost all American liability insurance contracts. This Demonstration creates a rich model in which to explore the effects of this on the likely outcomes of lawsuits. For each of the 20 sample lawsuits, you may specify the policy limit, coverage probability, litigation costs, and attachable assets of the insured as well as factors related to the strength of the duty to settle: (a) the size of the "as-if" policy the insurer must pretend it has in determining whether a settlement offer is reasonable, (b) the size of the "as-if" policy the insurer will be deemed to have written if it rejects a "reasonable" settlement offer, and (c) whether the insurer may discount for coverage issues the size of the "as-if" policy the insurer must pretend it has. The top panel of the Demonstration outputs a graph showing the plaintiff's expected position for each settlement offer it makes and superimposes on that graph information relating to the distribution of judgments in the underlying lawsuit, the policy limit and the zone of settlement offers that a court will deem reasonable. The parameters you set are shown in a table at the bottom of the Demonstration.

Contributed by: Seth J. Chandler (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

The two‐dimensional slider labeled "policy limit and coverage fractions" works as follows. The  axis determines the per occurrence limit of the liability insurance policy rescaled to run from 0 to the size of the largest possible judgment against the insured. The

axis determines the per occurrence limit of the liability insurance policy rescaled to run from 0 to the size of the largest possible judgment against the insured. The  axis determines the probability [0,1] that a court will ultimately determine that "coverage" exists, that is, that the insurer has a duty to pay on behalf of the insured all sums for which the insured is liable, subject to applicable limits of liability.

axis determines the probability [0,1] that a court will ultimately determine that "coverage" exists, that is, that the insurer has a duty to pay on behalf of the insured all sums for which the insured is liable, subject to applicable limits of liability.

The two-dimensional slider labeled "litigation costs fraction" works as follows. The axis determines the litigation costs the plaintiff will bear. The axis determines the litigation costs the insurer will bear. Both values are rescaled to run from 0 to the size of the largest possible judgment against the insured.

The slider labeled "insured's attachable assets fraction" determines the amount of assets the plaintiff could collect from the insured defendant in the event a court rendered a judgment in excess of the per occurrence limit. The value is rescaled to run from 0 to the size of the largest possible judgment against the insured.

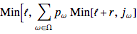

The two-dimensional slider labeled "strength of duty to settle" works as follows. The axis determines the extra amount in addition to policy limits that will be taken into account in determining whether a settlement offer is reasonable or not. A settlement is reasonable if it is less than  ] where ω is a possible outcome of the lawsuit (all possible outcomes are

] where ω is a possible outcome of the lawsuit (all possible outcomes are  ),

),  is the probability of that outcome,

is the probability of that outcome,  is the policy limit,

is the policy limit,  is the extra amount set by this slider, and

is the extra amount set by this slider, and  is the size of the judgment corresponding to outcome ω. This slider thus helps determine the size of the "reasonable settlement zone" marked on the top panel. Both the and values are rescaled to run from 0 to the size of the largest possible judgment against the insured.

is the size of the judgment corresponding to outcome ω. This slider thus helps determine the size of the "reasonable settlement zone" marked on the top panel. Both the and values are rescaled to run from 0 to the size of the largest possible judgment against the insured.

The checkbox "discount for coverage issues" allows simulation of settings in which a court permits the insurer to discount the amount of any possible judgment by the probability that it would not be covered. It thus affects the size of the reasonable settlement zone.

Permanent Citation

Adverse Selection

Adverse Selection

Seth J. Chandler Life Insurance Pricing

Life Insurance Pricing

Seth J. Chandler Efficient Single Limit Liability Insurance

Efficient Single Limit Liability Insurance

Seth J. Chandler Property Coinsurance

Property Coinsurance

Seth J. Chandler Insurance Disclosures

Insurance Disclosures

Seth J. Chandler The Efficient Dual-Limit Liability Insurance Contract

The Efficient Dual-Limit Liability Insurance Contract

Seth J. Chandler Moral Hazard

Moral Hazard

Seth J. Chandler Certainty Equivalent Wealth

Certainty Equivalent Wealth

Seth J. Chandler Bilateral Accident Model

Bilateral Accident Model

Seth J. Chandler A Conceptual Model of Lapse Financed Life Insurance

A Conceptual Model of Lapse Financed Life Insurance

Seth J. Chandler

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

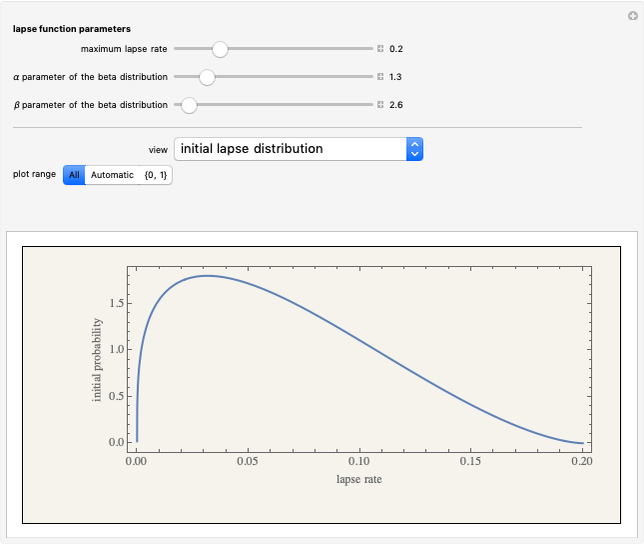

A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler