Loading Plot of a Principal Component Analysis (PCA)

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

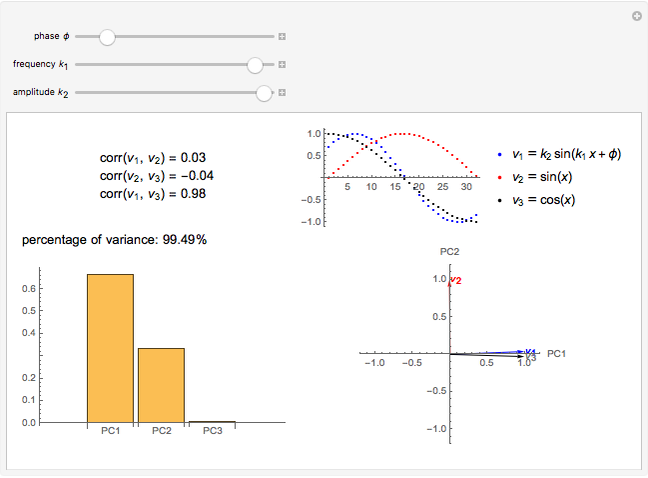

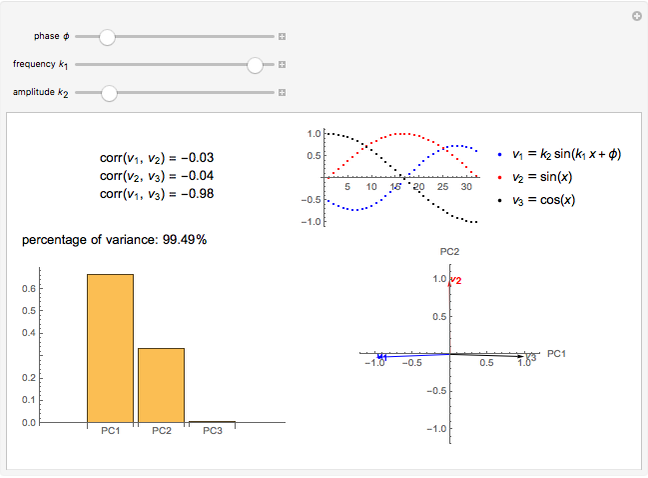

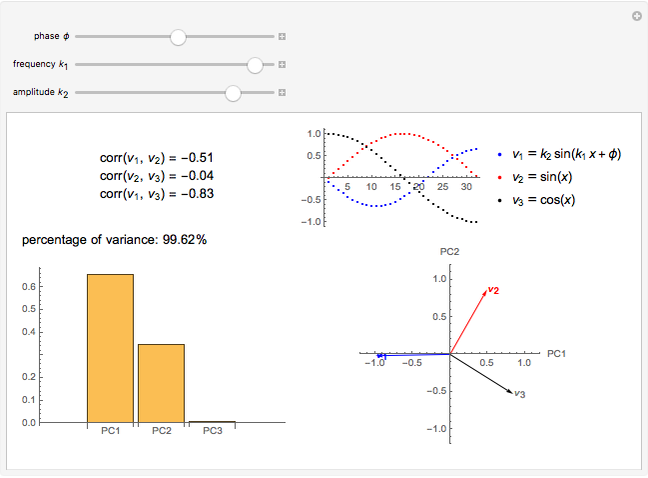

Principal component analysis (PCA) is a statistical procedure that converts data with possibly correlated variables into a set of linearly uncorrelated variables, analogous to a principal-axis transformation in mechanics.

[more]

Contributed by: D. Meliga and S. Z. Lavagnino (May 2016)

With additional contributions by: A. Chiavassaand M. Aria

Open content licensed under CC BY-NC-SA

Snapshots

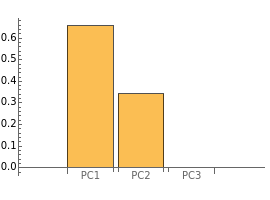

Details

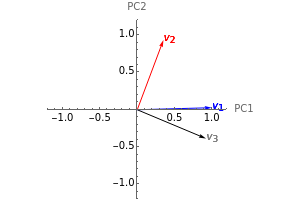

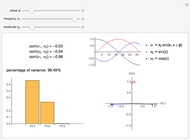

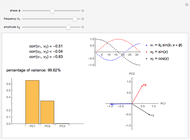

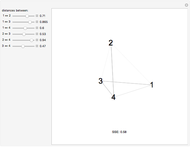

In the loading plot, the high correlation between two variables leads to two vectors that are very close to each other, the non-correlation leads to two vectors out of phase by  , while the anti-correlation leads to two vectors that are out of phase by

, while the anti-correlation leads to two vectors that are out of phase by  [2].

[2].

Snapshot 1: a strong correlation between  and

and

, non-correlation in the remaining cases

, non-correlation in the remaining cases  . From a graphical point of view, we can see two vectors that are very close, while the others are out of phase with each other by about .

. From a graphical point of view, we can see two vectors that are very close, while the others are out of phase with each other by about .

Snapshot 2: a strong correlation between and

, non-correlation in the remaining cases . From a graphical point of view, we can see two opposite vectors, while the others are out of phase to each other by about .

, non-correlation in the remaining cases . From a graphical point of view, we can see two opposite vectors, while the others are out of phase to each other by about .

References

[1] S. J. Press, Applied Multivariate Analysis: Using Bayesian and Frequentist Methods of Inference, Mineola, NY: Dover Publications, 2005.

[2] M. Aria. "L'analisi in Componenti Principali." (May 25, 2016) www.federica.unina.it/economia/analisi-statistica-sociologica/analisi-componenti-principali.

Permanent Citation

Aliasing in Time Series Analysis

Aliasing in Time Series Analysis

Ian McLeod 1, 2, 3-Parameter Logistic Rasch and Birnbaum Models and Item Analysis

1, 2, 3-Parameter Logistic Rasch and Birnbaum Models and Item Analysis

Olexandr Eugene Prokopchenko Exploring Skewness in Box Plots

Exploring Skewness in Box Plots

Ian McLeod Nonparametric Regression and Kernel Smoothing: Confidence Regions for the L2-Optimal Curve Estimate

Nonparametric Regression and Kernel Smoothing: Confidence Regions for the L2-Optimal Curve Estimate

Didier A. Girard Estimating a Centered Ornstein-Uhlenbeck Process under Measurement Errors

Estimating a Centered Ornstein-Uhlenbeck Process under Measurement Errors

Didier A. Girard Principal Components

Principal Components

Ian McLeod Fisher Discriminant Analysis

Fisher Discriminant Analysis

Ian McLeod Cluster Analysis for 2D Points

Cluster Analysis for 2D Points

Stephen Wolfram Edgeworth Expansion for Near-Normal Data

Edgeworth Expansion for Near-Normal Data

Housam Binous, Mamdouh Al-Harthi, and Brian G. Higgins Multidimensional Scaling

Multidimensional Scaling

Yaroslav Bulatov

-

Single-Step Reaction Kinetics Using Collision Theory

Single-Step Reaction Kinetics Using Collision Theory

S. Z. Lavagnino -

Crystal Field Theory for Coordination Complexes

Crystal Field Theory for Coordination Complexes

S. Z. Lavagnino -

Central Limit Theorem Illustrated with Four Probability Distributions

Central Limit Theorem Illustrated with Four Probability Distributions

S. Z. Lavagnino -

Kinetic and Thermodynamic Control of Electrophilic Addition Reactions

Kinetic and Thermodynamic Control of Electrophilic Addition Reactions

S. Z. Lavagnino -

Electrophilic Aromatic Substitution Reactions of Benzene

Electrophilic Aromatic Substitution Reactions of Benzene

S. Z. Lavagnino -

Electrophilic Addition to Alkenes with Formation of Optical Isomers

Electrophilic Addition to Alkenes with Formation of Optical Isomers

S. Z. Lavagnino -

Zeros of a Polynomial or Rational Function and Its Derivative

Zeros of a Polynomial or Rational Function and Its Derivative

S. Z. Lavagnino -

How to Catch a Standing Wave

How to Catch a Standing Wave

S. Z. Lavagnino -

Comparing the Cook-Torrance BRDF Model with Diffuse Reflection Simulation

Comparing the Cook-Torrance BRDF Model with Diffuse Reflection Simulation

S. Z. Lavagnino -

Stoichiometry: With Excess or Limiting Reagents

Stoichiometry: With Excess or Limiting Reagents

S. Z. Lavagnino -

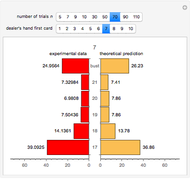

Dealer's Odds in Blackjack

Dealer's Odds in Blackjack

S. Z. Lavagnino -

Rotating Crystal Method for 2D Lattices Using Ewald's Circle

Rotating Crystal Method for 2D Lattices Using Ewald's Circle

S. Z. Lavagnino -

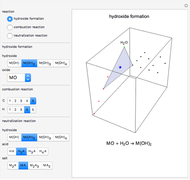

Chemical Reactions Represented via a 3D Simplex

Chemical Reactions Represented via a 3D Simplex

S. Z. Lavagnino -

Chemical Reactions Represented on a 2D Simplex

Chemical Reactions Represented on a 2D Simplex

S. Z. Lavagnino -

Laue's Method for 2D Lattices Using Ewald's Circle

Laue's Method for 2D Lattices Using Ewald's Circle

S. Z. Lavagnino -

Successive Dissociations of Polyprotic Acid H_4A as Regulated by pH

Successive Dissociations of Polyprotic Acid H_4A as Regulated by pH

S. Z. Lavagnino -

Detailed Analysis of Rutherford Scattering of Alpha Particles

Detailed Analysis of Rutherford Scattering of Alpha Particles

S. Z. Lavagnino -

Bertrand's Box Paradox

Bertrand's Box Paradox

S. Z. Lavagnino -

Classical Qualitative Inorganic Analysis

Classical Qualitative Inorganic Analysis

S. Z. Lavagnino -

Blood Donation Protocols

Blood Donation Protocols

S. Z. Lavagnino