Convergence of Binomial, Binomial Black-Scholes, and Trinomial Option Pricing Methods

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

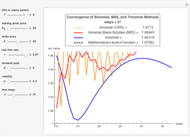

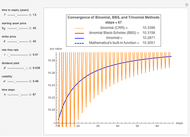

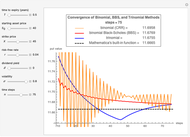

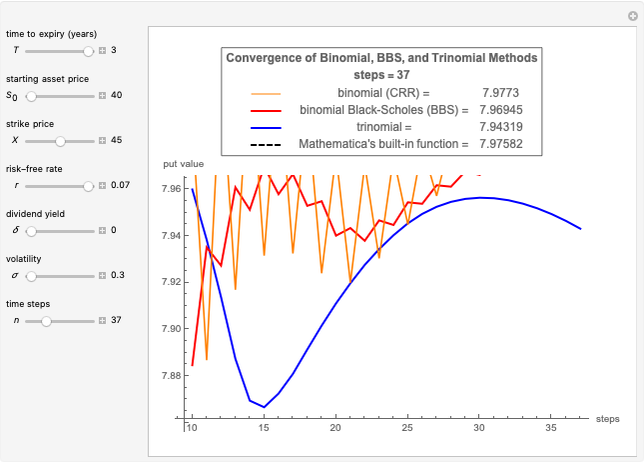

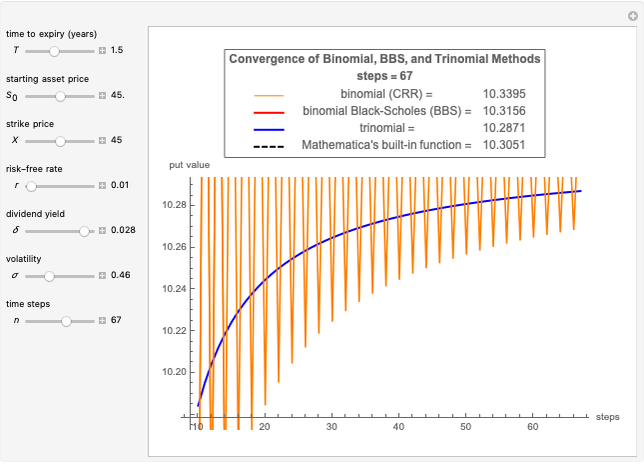

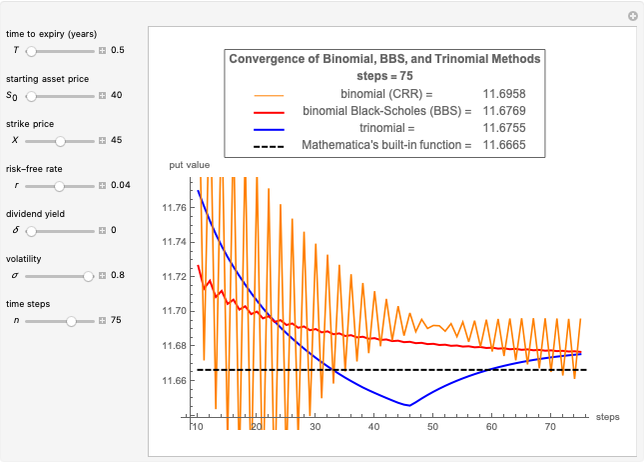

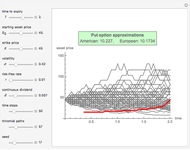

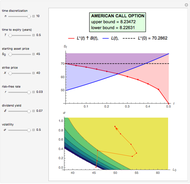

This Demonstration shows the convergence of the binomial [1], binomial Black–Scholes (BBS) [2], and trinomial [3] methods, depending on the American put option's maturity time discretization. Use the controls to set the option's parameters and time discretization (up to 100 uniform steps); the table shows the American put value approximations at the selected number of time steps. The horizontal black dashed line represents the option's value according to Mathematica's built-in function FinancialDerivative with a 1,000×10,000 grid size.

Contributed by: Michail Bozoudis (November 2014)

Suggested by: Michail Boutsikas

Open content licensed under CC BY-NC-SA

Snapshots

Details

Under the binomial method (CRR) [1], the underlying asset price is modeled as a recombining tree, where at each node the price can go up and down. These values are found by multiplying the value at the current node by the appropriate factor  or

or  :

:

,

,

,

,

with corresponding probabilities

,

,

,

,

where  is the asset-price volatility,

is the asset-price volatility,  is the continuous dividend yield,

is the continuous dividend yield,  is the risk-free rate, and

is the risk-free rate, and  is the length of each time step in the binomial tree (equal to the option's maturity divided by the number of time steps).

is the length of each time step in the binomial tree (equal to the option's maturity divided by the number of time steps).

To make sure that these probabilities are in the interval  , the condition

, the condition  should be satisfied.

should be satisfied.

Once the binomial lattice of all possible asset prices up to maturity has been calculated, the option value is found at each node by working backward from the final nodes to the present.

Under the binomial Black–Scholes (BBS) method [2], which is a variation of the binomial method, the Black–Scholes analytic formula is applied to estimate the values at those nodes one time step before expiration. Then, by working backward to the present, the process is similar to the binomial method. As seen in the graph, the BBS method converges more smoothly than the binomial method.

Under the trinomial method [3], the underlying asset price is modeled as a recombining tree, where at each node the price has three possible paths: up, down, or stable (middle). These values are found by multiplying the value at the current node by the appropriate factor  ,

,  , or

, or  :

:

,

,

,

,

,

,

with corresponding probabilities

,

,

,

,

.

.

To make sure that all probabilities are in the interval  , the condition

, the condition  should be satisfied.

should be satisfied.

Once the trinomial lattice of all possible asset prices up to maturity has been calculated, the option value is found at each node largely as for the binomial model, by working backward from the final nodes to the present. The difference between the trinomial and binomial models is that the option value at each non-final node is determined based on the three later nodes (as opposed to two) and their corresponding probabilities.

References

[1] J. Cox, S. Ross, and M. Rubinstein, "Option Pricing: A Simplified Approach," Journal of Financial Economics, 7(3), 1979 pp. 229–263. doi:10.1016/0304-405X(79)90015-1.

[2] M. Broadie and J. Detemple, "American Option Valuation: New Bounds, Approximations, and a Comparison of Existing Methods," The Review of Financial Studies, 9(4), 1996 pp. 1211–1250. doi:10.1093/rfs/9.4.1211.

[3] P. Boyle, "Option Valuation Using a Three Jump Process," International Options Journal, 3, 1986 pp. 7–12.

Permanent Citation

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Michail Bozoudis Pricing Put Options with the Binomial Method

Pricing Put Options with the Binomial Method

Michail Bozoudis Pricing Put Options with the Trinomial Method

Pricing Put Options with the Trinomial Method

Michail Bozoudis Pricing American Options with the Two- and Three-Point Maximum Methods

Pricing American Options with the Two- and Three-Point Maximum Methods

Michail Bozoudis Kim's Method for Pricing American Options

Kim's Method for Pricing American Options

Michail Bozoudis A Recursive Integration Method for Options Pricing

A Recursive Integration Method for Options Pricing

Michail Bozoudis Pricing Put Options with the Explicit Finite-Difference Method

Pricing Put Options with the Explicit Finite-Difference Method

Michail Bozoudis Kim's Method with Nonuniform Time Grid for Pricing American Options

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis Pricing Put Options with the Crank-Nicolson Method

Pricing Put Options with the Crank-Nicolson Method

Michail Bozoudis Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis

-

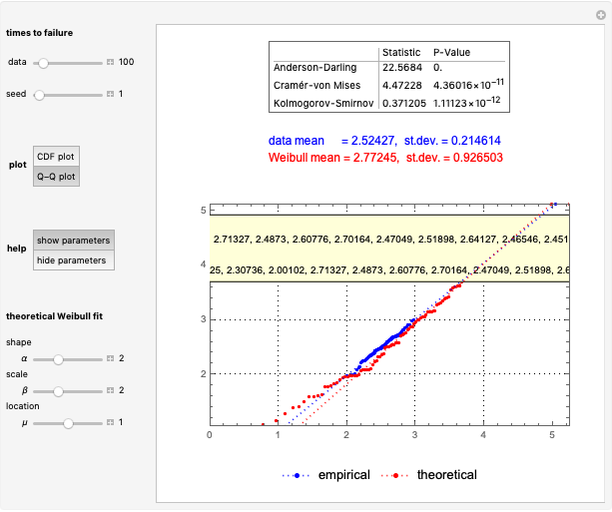

Fitting Times-to-Failure to a Weibull Distribution

Fitting Times-to-Failure to a Weibull Distribution

Michail Bozoudis -

A Canonical Optimal Stopping Problem for American Options

A Canonical Optimal Stopping Problem for American Options

Michail Bozoudis -

A Recursive Integration Method for Options Pricing

Michail Bozoudis -

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Michail Bozoudis -

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis -

Geometric Brownian Motion with Nonuniform Time Grid

Geometric Brownian Motion with Nonuniform Time Grid

Michail Bozoudis -

Kim's Method for Pricing American Options

Michail Bozoudis -

Simultaneous Confidence Interval for the Weibull Parameters

Simultaneous Confidence Interval for the Weibull Parameters

Michail Bozoudis -

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Michail Bozoudis -

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis -

American Options on Assets with Dividends Near Expiry

American Options on Assets with Dividends Near Expiry

Michail Bozoudis -

Hold-or-Exercise for an American Put Option

Hold-or-Exercise for an American Put Option

Michail Bozoudis -

American Capped Call Options with Exponential Cap

American Capped Call Options with Exponential Cap

Michail Bozoudis -

American Capped Call Options with Constant Cap

American Capped Call Options with Constant Cap

Michail Bozoudis -

Pricing Put Options with the Crank-Nicolson Method

Michail Bozoudis -

Pricing Put Options with the Implicit Finite-Difference Method

Pricing Put Options with the Implicit Finite-Difference Method

Michail Bozoudis -

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Michail Bozoudis -

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Michail Bozoudis -

Fitting Data to a Lognormal Distribution

Fitting Data to a Lognormal Distribution

Michail Bozoudis -

SARIMA Process Forecasting Model

SARIMA Process Forecasting Model

Michail Bozoudis