Endogeneity Bias

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

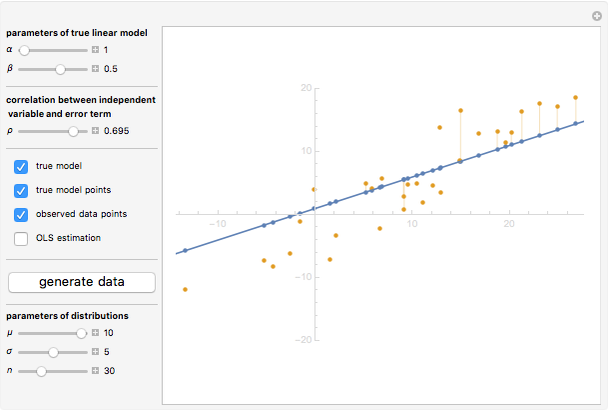

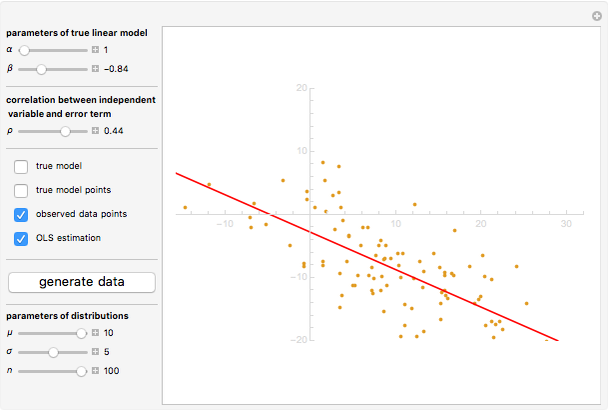

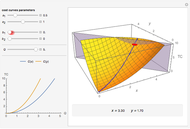

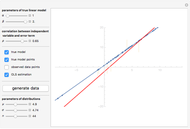

Endogeneity is one of the major concerns of contemporary empirical studies in economics and econometrics. This Demonstration aims to show the geometric sense of this phenomenon in the simplest setting, namely the model with one single explanatory variable (also known as the independent variable).

[more]

Contributed by: Timur Gareev (February 2016)

Open content licensed under CC BY-NC-SA

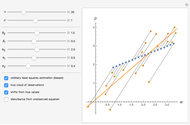

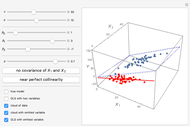

Snapshots

Details

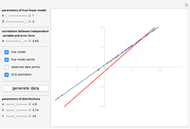

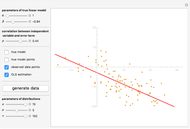

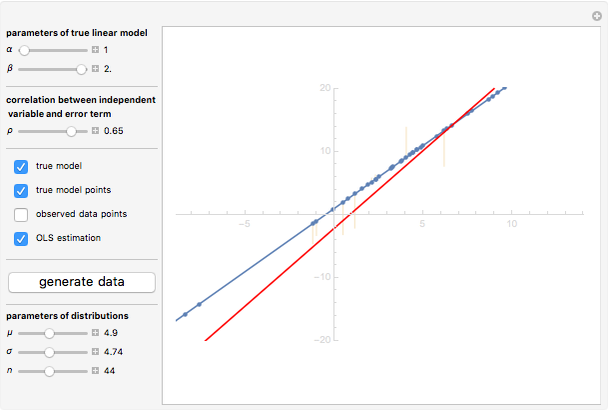

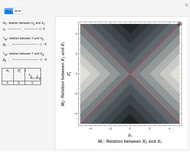

Endogeneity bias (in the narrow sense) is applicable to the model if  . Whenever

. Whenever  (meaning that the independent variable

(meaning that the independent variable  is not correlated with the error term

is not correlated with the error term  ), there is no endogeneity bias (in the narrow sense). In this case, the slope of the fitting curve (OLS regression line) converges to the slope of the true line

), there is no endogeneity bias (in the narrow sense). In this case, the slope of the fitting curve (OLS regression line) converges to the slope of the true line  with the growth of the number of observations

with the growth of the number of observations  , or

, or  .

.

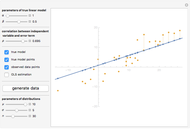

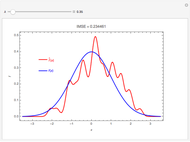

On the contrary, with endogeneity bias there is no such convergence and the fitting model gives inconsistent estimates of in terms of  . You can also see a geometric representation of endogeneity in that simple case when observations (points on the plot) lie systematically lower or higher than a given true line. That is what makes OLS fitting pointless in the presence of endogeneity bias. There are many reasons of endogeneity, namely, omitted variables, measurement errors, and simultaneity. Methods such as using a control function or instrumental variables (IV) can be applied to cure the endogeneity bias problem.

. You can also see a geometric representation of endogeneity in that simple case when observations (points on the plot) lie systematically lower or higher than a given true line. That is what makes OLS fitting pointless in the presence of endogeneity bias. There are many reasons of endogeneity, namely, omitted variables, measurement errors, and simultaneity. Methods such as using a control function or instrumental variables (IV) can be applied to cure the endogeneity bias problem.

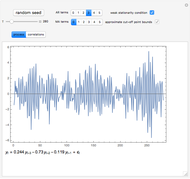

This Demonstration is designed to generate random data by clicking the "generate data" button. You can vary the parameters: is the number of observations,  is both (for simplicity of the model) the expectation and the standard error of the random variate

is both (for simplicity of the model) the expectation and the standard error of the random variate  , and

, and  is the standard error of the normally distributed error term

is the standard error of the normally distributed error term  with

with  expectation.

expectation.

Reference

[1] J. M. Wooldridge, Introductory Econometrics: A Modern Approach, Mason, OH: South-Western, Cengage Learning, 2009 p. 26.

Permanent Citation

Expected Returns of the Dow Industrials, Fama-French Model

Expected Returns of the Dow Industrials, Fama-French Model

Jeff Hamrick and Jason Cawley Mean-Reverting Random Walks

Mean-Reverting Random Walks

Jason Cawley Auto-Regressive Simulation (Second-Order)

Auto-Regressive Simulation (Second-Order)

David von Seggern (University of Nevada) Autoregressive Moving-Average Simulation (First Order)

Autoregressive Moving-Average Simulation (First Order)

David von Seggern (University of Nevada) The Envelope Theorem: Numerical Examples

The Envelope Theorem: Numerical Examples

Jeff Hamrick Simultaneity Bias

Simultaneity Bias

Timur Gareev Omitted Variable Bias in 3D

Omitted Variable Bias in 3D

Timur Gareev Omitted Variable Bias

Omitted Variable Bias

Alrik Thiem Variance-Bias Tradeoff

Variance-Bias Tradeoff

Ian McLeod Autoregressive Moving-Average Generator

Autoregressive Moving-Average Generator

Matus Baniar

-

Returns to Scale in One-Factor Production Functions

Returns to Scale in One-Factor Production Functions

Timur Gareev -

Omitted Variable Bias in 3D

Timur Gareev -

Revenue and Costs Curves Analysis

Revenue and Costs Curves Analysis

Timur Gareev -

Leontief Production Function

Leontief Production Function

Timur Gareev -

Simultaneity Bias

Timur Gareev -

Firm Costs Optimization Problem in Primal and Dual Form

Firm Costs Optimization Problem in Primal and Dual Form

Timur Gareev -

Comparative and Absolute Advantage

Comparative and Absolute Advantage

Timur Gareev -

Firm with Two Plants

Firm with Two Plants

Timur Gareev -

Elasticity Function

Elasticity Function

Timur Gareev -

Substitute and Complementary Goods

Substitute and Complementary Goods

Timur Gareev -

Monopoly with Two Plants

Monopoly with Two Plants

Timur Gareev -

Best Response in Static Two-Player Games

Best Response in Static Two-Player Games

Timur Gareev -

Hotelling Model of Product Quality Differentiation

Hotelling Model of Product Quality Differentiation

Timur Gareev -

Endogeneity Bias

Endogeneity Bias

Timur Gareev -

Discriminating Monopolist with Two Independent Markets

Discriminating Monopolist with Two Independent Markets

Timur Gareev -

Monopsony in the Labor Market

Monopsony in the Labor Market

Timur Gareev -

Nondiscriminating Monopolist with Two Independent Markets

Nondiscriminating Monopolist with Two Independent Markets

Timur Gareev -

Supply Curve from Piecewise Linear Cost Function

Supply Curve from Piecewise Linear Cost Function

Timur Gareev -

Duopoly Model in 3D

Duopoly Model in 3D

Timur Gareev -

Isocosts, Isoquants, Isocline Lines, and Scale Lines for Homogeneous (Cobb-Douglas) Functions

Isocosts, Isoquants, Isocline Lines, and Scale Lines for Homogeneous (Cobb-Douglas) Functions

Timur Gareev