Omitted Variable Bias in 3D

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

This Demonstration develops geometric intuition behind the concept of omitted variable bias. In econometrics modeling, there is a persistent risk of omitting an important variable (i.e. due to not understanding the true model structure or due to a lack of relevant data). As a result, endogeneity [1] spoils the model, resulting in inconsistent and therefore misleading estimations of model coefficients. Usually the effect of the omitted variable is explained analytically or via numerical examples, but visualization may bring more insight to the issue.

[more]

Contributed by: Timur Gareev (May 2018)

Open content licensed under CC BY-NC-SA

Snapshots

Details

If we try to estimate a true model of the form

with an incorrect model of the form

,

,

the estimation of  , which is signed

, which is signed  , is most likely biased. Indeed, we have by definition:

, is most likely biased. Indeed, we have by definition:

.

.

Here we have

;

;

and

.

.

The element  is an error term vector, where each observation term is independent (from each other) and normally distributed with mean 0 and variance

is an error term vector, where each observation term is independent (from each other) and normally distributed with mean 0 and variance  .

.

The key term in the preceding expression is  , which we can simulate with the

, which we can simulate with the  control. If it equals zero, no problems arise—estimations are unbiased,

control. If it equals zero, no problems arise—estimations are unbiased,  . However, in practice the important feature of the model of the form

. However, in practice the important feature of the model of the form

is that  , and so omitting

, and so omitting  from the evaluation causes bias. It is always a source of confusion, but should not be too high, otherwise results even without omitted variables will be misleading (as we approach the other "trap" in the form of multicollinearity).

from the evaluation causes bias. It is always a source of confusion, but should not be too high, otherwise results even without omitted variables will be misleading (as we approach the other "trap" in the form of multicollinearity).

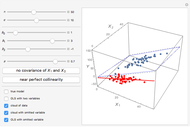

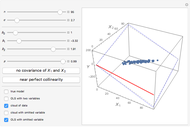

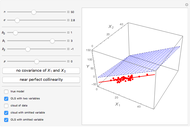

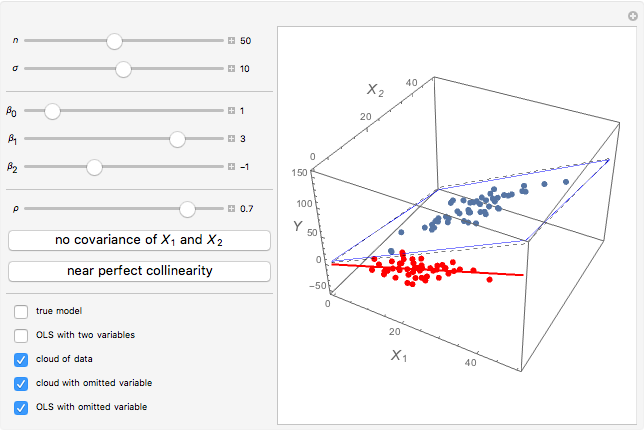

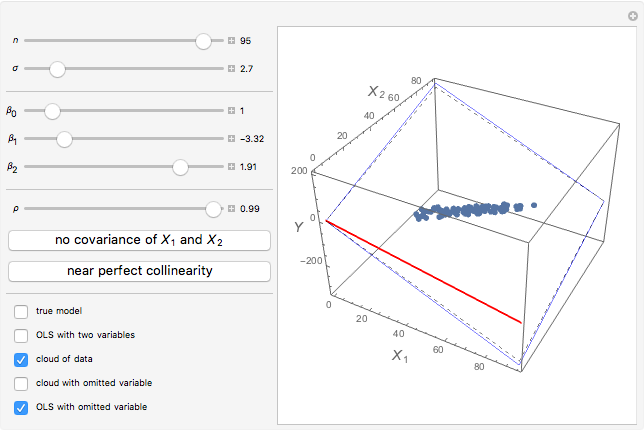

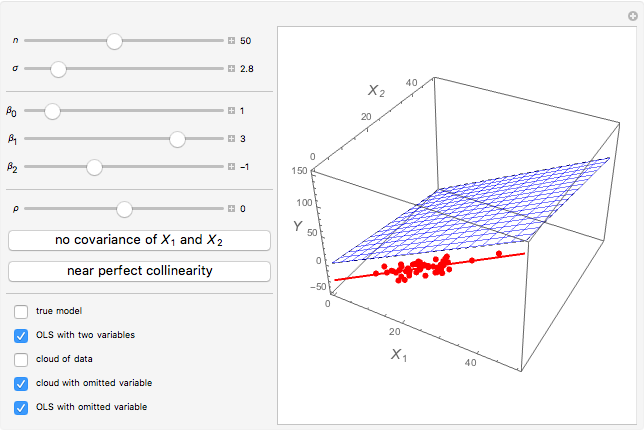

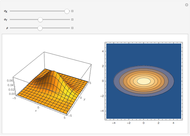

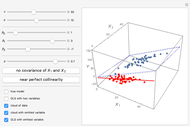

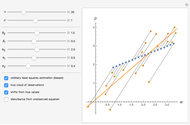

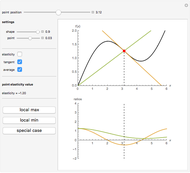

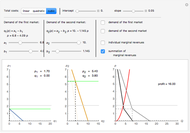

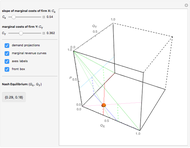

We demonstrate it as follows. The blue cloud is the observations cloud, and each point stands for one observation (the number of observations may be changed with  ). The black lattice shows the true model. The blue lattice reflects the correct estimation with both variables

). The black lattice shows the true model. The blue lattice reflects the correct estimation with both variables  and included. The red line is the regression with the omitted variable. (The red cloud is the projection of the observations cloud from true 3D space to 2D.) Use the checkboxes to switch the appearance of elements on and off. When you use the checkboxes, the cloud does not change. Be warned, though, that each time parameters change, the cloud of observation changes as well.

and included. The red line is the regression with the omitted variable. (The red cloud is the projection of the observations cloud from true 3D space to 2D.) Use the checkboxes to switch the appearance of elements on and off. When you use the checkboxes, the cloud does not change. Be warned, though, that each time parameters change, the cloud of observation changes as well.

Most important are the slopes of black and blue planes and the red line. When the slopes are relatively equal, there is no bias.

Increasing and reducing  may considerably reduce bias. Use the buttons to study special cases with

may considerably reduce bias. Use the buttons to study special cases with  or

or  (

( corresponds to perfect multicollinearity, so we cannot study this case). It is also recommended to check

corresponds to perfect multicollinearity, so we cannot study this case). It is also recommended to check  visually.

visually.

Reference

[1] Wikipedia. "Endogeneity (Econometrics)." (May 7, 2018) en.wikipedia.org/wiki/Endogeneity_(econometrics).

Permanent Citation

Omitted Variable Bias

Omitted Variable Bias

Alrik Thiem Endogeneity Bias

Endogeneity Bias

Timur Gareev Variance-Bias Tradeoff

Variance-Bias Tradeoff

Ian McLeod Symmetrizing Positive Random Variables

Symmetrizing Positive Random Variables

Ian McLeod Entropy of a Message Using Random Variables

Entropy of a Message Using Random Variables

Daniel de Souza Carvalho Joint Density of Trivariate Gaussian Random Variables

Joint Density of Trivariate Gaussian Random Variables

John M. Shea Joint Density of Bivariate Gaussian Random Variables

Joint Density of Bivariate Gaussian Random Variables

John M. Shea Distribution of the Sample Range of Continuous Random Variables

Distribution of the Sample Range of Continuous Random Variables

Heikki Ruskeepää Distribution of the Sample Range of Discrete Random Variables

Distribution of the Sample Range of Discrete Random Variables

Heikki Ruskeepää Illustrating the Central Limit Theorem with Sums of Uniform and Exponential Random Variables

Illustrating the Central Limit Theorem with Sums of Uniform and Exponential Random Variables

Ian McLeod

-

Krugman's Model of Increasing Returns and Monopolistic Competition

Krugman's Model of Increasing Returns and Monopolistic Competition

Timur Gareev -

Returns to Scale in One-Factor Production Functions

Returns to Scale in One-Factor Production Functions

Timur Gareev -

Omitted Variable Bias in 3D

Omitted Variable Bias in 3D

Timur Gareev -

Revenue and Costs Curves Analysis

Revenue and Costs Curves Analysis

Timur Gareev -

Leontief Production Function

Leontief Production Function

Timur Gareev -

Simultaneity Bias

Simultaneity Bias

Timur Gareev -

Firm Costs Optimization Problem in Primal and Dual Form

Firm Costs Optimization Problem in Primal and Dual Form

Timur Gareev -

Comparative and Absolute Advantage

Comparative and Absolute Advantage

Timur Gareev -

Firm with Two Plants

Firm with Two Plants

Timur Gareev -

Elasticity Function

Elasticity Function

Timur Gareev -

Substitute and Complementary Goods

Substitute and Complementary Goods

Timur Gareev -

Monopoly with Two Plants

Monopoly with Two Plants

Timur Gareev -

Best Response in Static Two-Player Games

Best Response in Static Two-Player Games

Timur Gareev -

Hotelling Model of Product Quality Differentiation

Hotelling Model of Product Quality Differentiation

Timur Gareev -

Endogeneity Bias

Timur Gareev -

Discriminating Monopolist with Two Independent Markets

Discriminating Monopolist with Two Independent Markets

Timur Gareev -

Monopsony in the Labor Market

Monopsony in the Labor Market

Timur Gareev -

Nondiscriminating Monopolist with Two Independent Markets

Nondiscriminating Monopolist with Two Independent Markets

Timur Gareev -

Supply Curve from Piecewise Linear Cost Function

Supply Curve from Piecewise Linear Cost Function

Timur Gareev -

Duopoly Model in 3D

Duopoly Model in 3D

Timur Gareev