Richardson Extrapolation Applied Twice to Accelerate the Convergence of an Estimate

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

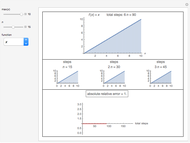

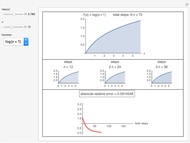

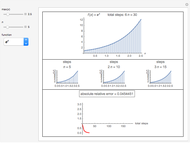

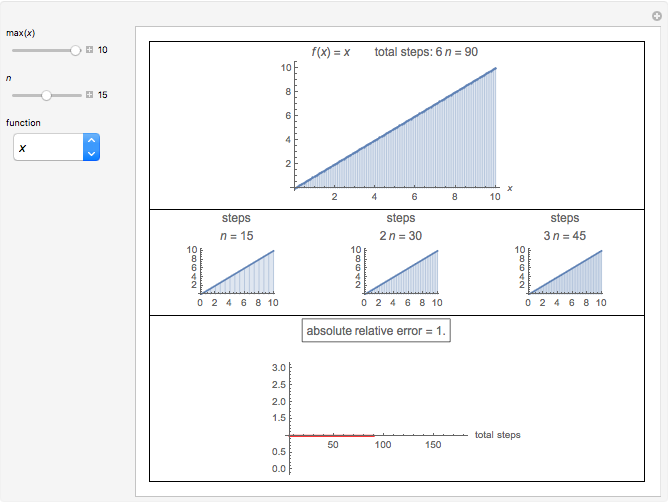

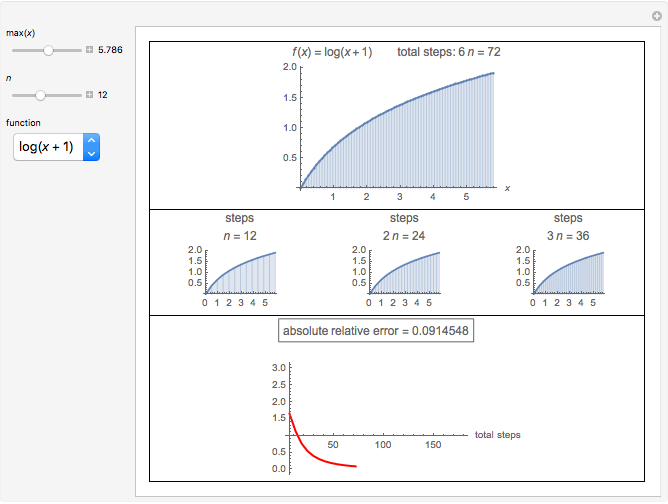

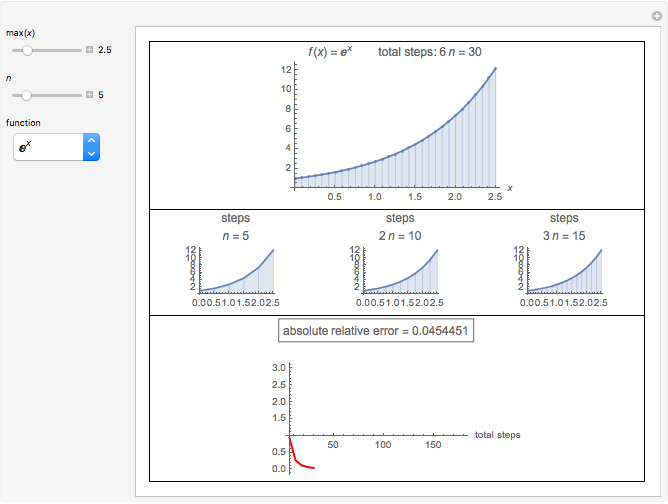

This Demonstration shows Richardson extrapolation applied twice to accelerate the convergence of an estimate.

[more]

Contributed by: Michail Bozoudis (July 2014)

Suggested by: Michail Boutsikas

Open content licensed under CC BY-NC-SA

Snapshots

Details

Let  be an approximation of the exact value

be an approximation of the exact value  of the integral of

of the integral of  that depends on a positive step size

that depends on a positive step size  with an error formula of the form

with an error formula of the form

,

,

where the  are known constants. For step sizes

are known constants. For step sizes  and

and  ,

,

To apply Richardson extrapolation twice, multiply the last two equations by  and

and  , respectively, and then, by adding all equations, the two error terms of the lowest order disappear:

, respectively, and then, by adding all equations, the two error terms of the lowest order disappear:

.

.

Notice that the approximations  and

and  require the same computational effort, yet the errors are

require the same computational effort, yet the errors are  and

and  , respectively.

, respectively.

Permanent Citation

Power Series Interval of Convergence

Power Series Interval of Convergence

Olivia M. Carducci (East Stroudsburg University) Convergence of a Recursive Sequence

Convergence of a Recursive Sequence

Soledad María Sáez Martínez and Félix Martínez de la Rosa Euler's Estimate of Pi

Euler's Estimate of Pi

Izidor Hafner Monte Carlo Methods to Estimate Area

Monte Carlo Methods to Estimate Area

Tomas Garza Convergence of Newton's Method for Approximating Square Roots

Convergence of Newton's Method for Approximating Square Roots

Andrzej Kozlowski Using Sampled Data to Estimate Derivatives, Integrals, and Interpolated Values

Using Sampled Data to Estimate Derivatives, Integrals, and Interpolated Values

Robert L. Brown Mixing Cell Model Applied to Transport in Porous Media

Mixing Cell Model Applied to Transport in Porous Media

Clay Gruesbeck Nonparametric Curve Estimation by Smoothing Splines: Unbiased-Risk-Estimate Selector and its Robust Version via Randomized Choices

Nonparametric Curve Estimation by Smoothing Splines: Unbiased-Risk-Estimate Selector and its Robust Version via Randomized Choices

Didier A. Girard Kernel Density Estimation

Kernel Density Estimation

Jeff Hamrick Estimating Planetary Perihelion Precession

Estimating Planetary Perihelion Precession

Brad Klee

-

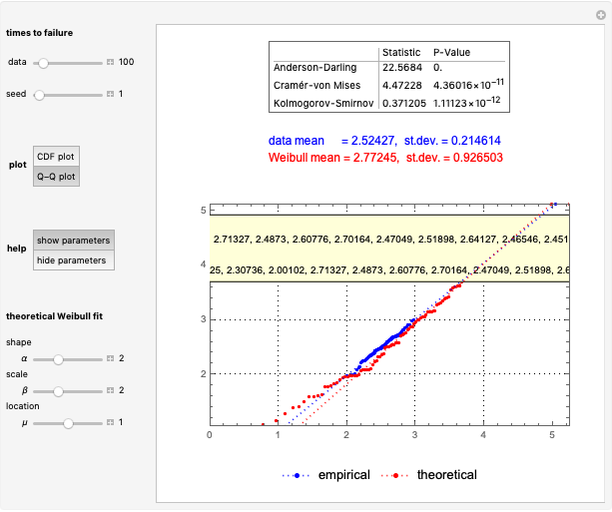

Fitting Times-to-Failure to a Weibull Distribution

Fitting Times-to-Failure to a Weibull Distribution

Michail Bozoudis -

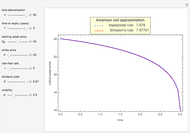

A Canonical Optimal Stopping Problem for American Options

A Canonical Optimal Stopping Problem for American Options

Michail Bozoudis -

A Recursive Integration Method for Options Pricing

A Recursive Integration Method for Options Pricing

Michail Bozoudis -

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Adaptive Mesh Relocation-Refinement (AMrR) on Kim's Method for Options Pricing

Michail Bozoudis -

Kim's Method with Nonuniform Time Grid for Pricing American Options

Kim's Method with Nonuniform Time Grid for Pricing American Options

Michail Bozoudis -

Geometric Brownian Motion with Nonuniform Time Grid

Geometric Brownian Motion with Nonuniform Time Grid

Michail Bozoudis -

Kim's Method for Pricing American Options

Kim's Method for Pricing American Options

Michail Bozoudis -

Simultaneous Confidence Interval for the Weibull Parameters

Simultaneous Confidence Interval for the Weibull Parameters

Michail Bozoudis -

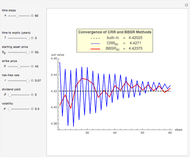

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Binomial Black-Scholes with Richardson Extrapolation (BBSR) Method

Michail Bozoudis -

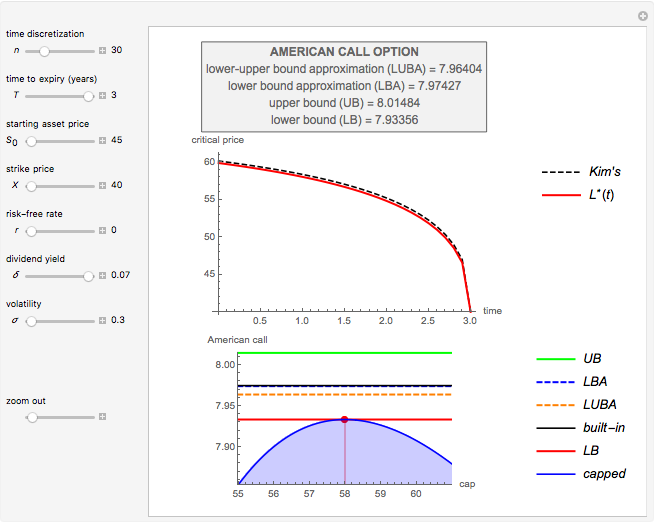

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Pricing American Options with the Lower-Upper Bound Approximation (LUBA) Method

Michail Bozoudis -

American Options on Assets with Dividends Near Expiry

American Options on Assets with Dividends Near Expiry

Michail Bozoudis -

Hold-or-Exercise for an American Put Option

Hold-or-Exercise for an American Put Option

Michail Bozoudis -

American Capped Call Options with Exponential Cap

American Capped Call Options with Exponential Cap

Michail Bozoudis -

American Capped Call Options with Constant Cap

American Capped Call Options with Constant Cap

Michail Bozoudis -

Pricing Put Options with the Crank-Nicolson Method

Pricing Put Options with the Crank-Nicolson Method

Michail Bozoudis -

Pricing Put Options with the Implicit Finite-Difference Method

Pricing Put Options with the Implicit Finite-Difference Method

Michail Bozoudis -

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Estimating a Distribution Function Subject to a Stochastic Order Restriction

Michail Bozoudis -

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Maximizing a Bermudan Put with a Single Early-Exercise Temporal Point

Michail Bozoudis -

Fitting Data to a Lognormal Distribution

Fitting Data to a Lognormal Distribution

Michail Bozoudis -

SARIMA Process Forecasting Model

SARIMA Process Forecasting Model

Michail Bozoudis