Saving for Retirement

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

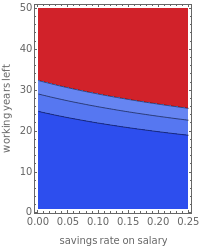

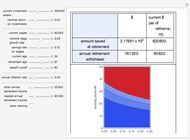

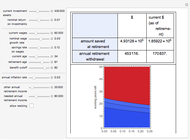

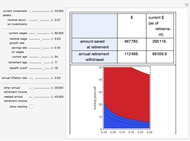

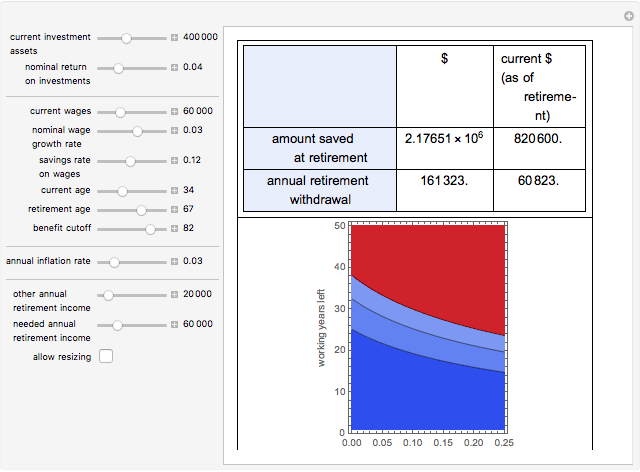

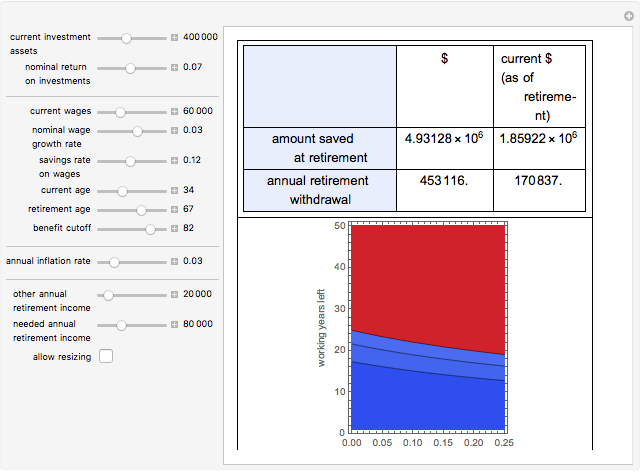

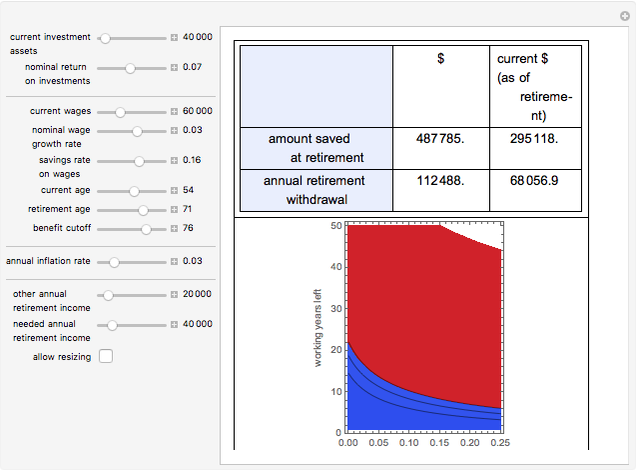

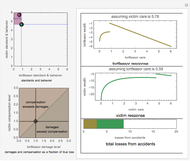

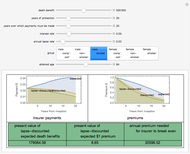

This Demonstration explores the tradeoff between the savings rate during periods of employment and the length of time people need to work in order to achieve desired levels of retirement income. First, set your current investment assets and the rate of return you anticipate making on investments over your lifetime. Next, set your current wages, your expected level of wage growth over your working lifetime, and the fraction of wage income you expect to be able to invest each year. Specify your current age, the age at which you wish to retire, and the age at which you are likely no longer to need retirement benefits. You also need to make a guess as to the rate of future inflation. Then, identify any non-investment income you expect to have during your retirement, such as Social Security benefits in the United States or, perhaps, part-time labor income. Finally, specify the needed or desired level of income you want during your retirement. The Demonstration shows how much money you will have available at retirement and the amount of money you can annually withdraw from that accumulation such that nothing is left at the end of the benefit period you specified. The graphic shows how you might achieve the same level of retirement income by either saving more during your working years or by working for a longer period of time.

Contributed by: Seth J. Chandler (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

Snapshot 1: A low rate of return on investments significantly limits realistic retirement income.

Snapshot 2: A high rate of return on investments creates better choices among savings rates and retirement age.

Snapshot 3: The person who defers saving until later in life has a very difficult time creating desired levels of retirement income.

This Demonstration does not take taxation into account.

The amount of money accumulated at retirement can generally be annuitized by transferring the risk of longevity to an insurer. The precise amount paid on the annuity depends on a number of factors, including the health of the annuitant. You can obtain a decent approximation to the amount paid by an annuity by setting the benefit cutoff age to your expected age of death or, to decrease risk, to a slightly higher value.

Permanent Citation

"Saving for Retirement"

http://demonstrations.wolfram.com/SavingForRetirement/

Wolfram Demonstrations Project

Published: March 7 2011

Property Coinsurance

Property Coinsurance

Seth J. Chandler Occurrence versus Claims-Made Insurance Policies

Occurrence versus Claims-Made Insurance Policies

Seth J. Chandler Stock Price Envelopes

Stock Price Envelopes

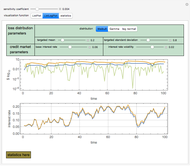

Seth J. Chandler Estimating Insurance Premiums Using Exceedance Data and the Method of Moments

Estimating Insurance Premiums Using Exceedance Data and the Method of Moments

Seth J. Chandler Estimating Loss Functions Using Exceedance Data and the Method of Moments

Estimating Loss Functions Using Exceedance Data and the Method of Moments

Seth J. Chandler Insurance Disclosures

Insurance Disclosures

Seth J. Chandler Tail Conditional Expectations

Tail Conditional Expectations

Seth J. Chandler Pay the Points?

Pay the Points?

Seth J. Chandler Bilateral Accident Model

Bilateral Accident Model

Seth J. Chandler Life Insurance Pricing

Life Insurance Pricing

Seth J. Chandler

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler