Tail Conditional Expectations

Requires a Wolfram Notebook System

Interact on desktop, mobile and cloud with the free Wolfram Player or other Wolfram Language products.

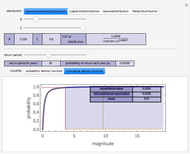

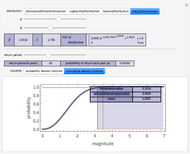

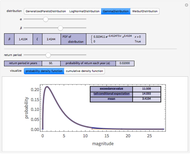

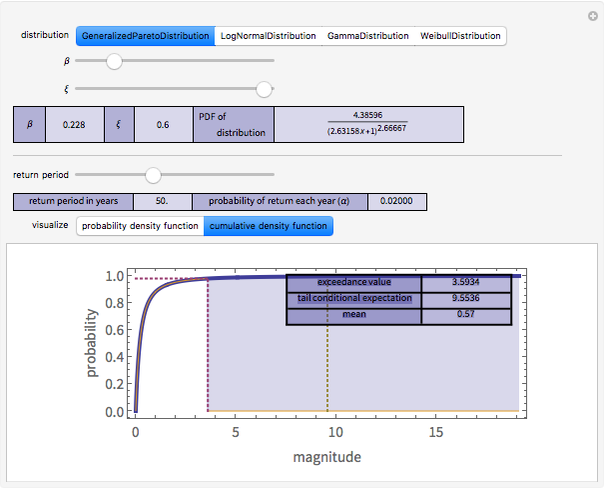

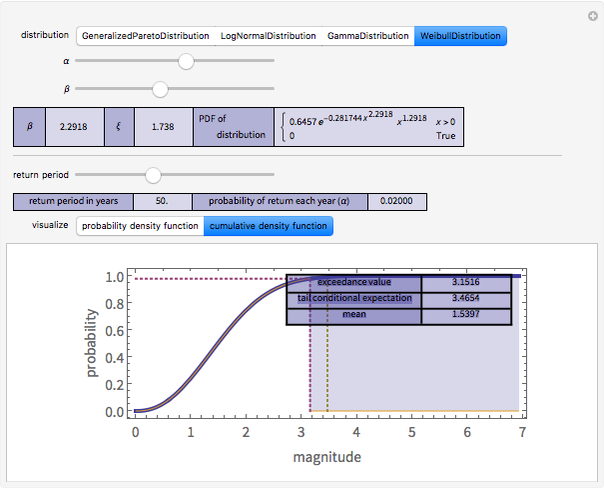

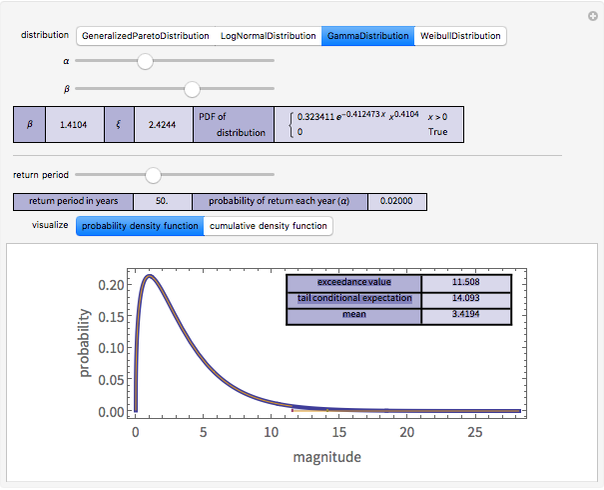

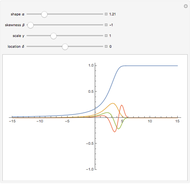

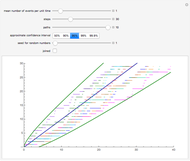

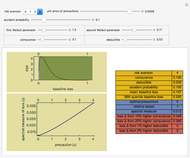

In modeling catastrophes, it is often useful to know how large a loss can be expected to be, given the assumption that the loss is greater than some amount. This value—the so-called "tail conditional expectation"—may be of great relevance to those who insure or reinsure against the highest levels of losses; it is sometimes what is meant by the actuarial term "probable maximum loss". In this Demonstration, you select a family of distributions and two parameters that instantiate a particular distribution from that family. The resulting distribution determines the probability that a loss from some catastrophe will exceed some amount. You can then set the magnitude of the catastrophe you wish to study. A "return period" of 50, for example, means that you wish to study catastrophes that are larger than all of those that will, on average, occur over a 50 year period. The Demonstration responds by drawing the distribution you have selected (you select whether you want to see the probability density function or the cumulative density function): the red dashed line shows the "exceedance value" and the blue line shows the tail conditional expectation, which is computed using numerical integration. An inset grid recapitulates the results.

Contributed by: Seth J. Chandler (March 2011)

Open content licensed under CC BY-NC-SA

Snapshots

Details

This Demonstration was influenced in part by Dr. Gordon Woo's article "Natural Catastrophe Probable Maximum Loss," British Actuarial Journal, 8(5), 2002 pp. 943–959.

Snapshot 1: If the "damage" random variable is drawn from certain generalized Pareto distributions, the tail conditional expectation can be three times larger than the exceedance value.

Snapshot 2: If the "damage" random variable is drawn from certain Weibull distributions, the tail conditional expectation is not much larger than the exceedance value.

Snapshot 3: A model in which damage is a random variable drawn from a gamma distribution. The tail conditional expectation, though of course larger than the exceedance value, does not hugely exceed the exceedance value.

It becomes apparent from the Demonstration that the tail conditional expectation is quite sensitive to the particular family of distributions from which the random variable is drawn. Since it is often difficult from data alone to decide which family of distributions should be used, beliefs about tail conditional expectations can vary greatly and can probably be refined only by an understanding of the physical processes behind the distributions. This sensitivity to assumptions can make it difficult to resolve debates about the appropriate premiums to compensate for the risks assumed by private or governmental excess insurers.

Permanent Citation

"Tail Conditional Expectations"

http://demonstrations.wolfram.com/TailConditionalExpectations/

Wolfram Demonstrations Project

Published: March 7 2011

Power Law Tails in Log Normal Data

Power Law Tails in Log Normal Data

Fiona Maclachlan Stock Price Probability with Stable Distributions

Stock Price Probability with Stable Distributions

Bob Rimmer Estimating Insurance Premiums Using Exceedance Data and the Method of Moments

Estimating Insurance Premiums Using Exceedance Data and the Method of Moments

Seth J. Chandler Estimating Loss Functions Using Exceedance Data and the Method of Moments

Estimating Loss Functions Using Exceedance Data and the Method of Moments

Seth J. Chandler Statistical Mechanics of Money

Statistical Mechanics of Money

Ian Wright Closed-Form Full Life Cycle Distribution

Closed-Form Full Life Cycle Distribution

Kelly S. Lowder Kernel Density Estimations: Condorcet's Jury Theorem, Part 5

Kernel Density Estimations: Condorcet's Jury Theorem, Part 5

Tetsuya Saito Stable Distribution Function

Stable Distribution Function

Bob Rimmer Simulating the Poisson Process

Simulating the Poisson Process

Heikki Ruskeepää Polynomial Fits of Random Walks

Polynomial Fits of Random Walks

Michael Schreiber

-

Post-Event Bonding

Post-Event Bonding

Seth J. Chandler -

Emulating Land Use Evolution with a Cellular Automaton

Emulating Land Use Evolution with a Cellular Automaton

Seth J. Chandler -

General Assembly Resolution Viewer

General Assembly Resolution Viewer

Seth J. Chandler -

Random Acyclic Networks

Random Acyclic Networks

Seth J. Chandler -

A Theory of Insurance Lapses

A Theory of Insurance Lapses

Seth J. Chandler -

Asylum in the United States

Asylum in the United States

Seth J. Chandler -

Property Coinsurance

Property Coinsurance

Seth J. Chandler -

The Persuasion Effect: A Traditional Two-Stage Jury Model

The Persuasion Effect: A Traditional Two-Stage Jury Model

Seth J. Chandler -

Cellular Automata with Global Control

Cellular Automata with Global Control

Seth J. Chandler -

Sports Seasons Based on Score Distributions

Sports Seasons Based on Score Distributions

Seth J. Chandler -

Evidentiary Uncertainty

Evidentiary Uncertainty

Seth J. Chandler -

Spectral Measures

Spectral Measures

Seth J. Chandler -

The Banzhaf Power Index of States for Presidential Candidates

The Banzhaf Power Index of States for Presidential Candidates

Seth J. Chandler -

Liability Insurance Desirability under Lognormal Loss Distributions

Liability Insurance Desirability under Lognormal Loss Distributions

Seth J. Chandler -

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

The Effects of Coinsurance and Deductibles on Optimal Precautions for Weibull-Distributed Loss

Seth J. Chandler -

Collocation by Chi Square

Collocation by Chi Square

Seth J. Chandler -

The Present Value of Future Gas Use

The Present Value of Future Gas Use

Seth J. Chandler -

Visualizing Legal Rules: A Homicide Case

Visualizing Legal Rules: A Homicide Case

Seth J. Chandler -

Communities of Nations Bridged by Language Similarity

Communities of Nations Bridged by Language Similarity

Seth J. Chandler